European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

74

Financial Performance Analysis of Adidas AG

Anupa Jayawardhana

Department of Sport Science and Physical Education, Faculty of Social Sciences, University of Kelaniya,

Dalugama, 11600, Sri Lanka

Abstract

The financial statement of Adidas has been selected and analysed. The financial statement indicates the balance

sheet, income statement and the cash flow statement. Financial performance has been studied using horizontal

analysis, vertical analysis, trend analysis and mainly ratio analysis to suggest improvements to increase finance

flow, improve dividend and reduce liabilities. Main analysis is based on 2014 and 2013 financial years which are

ending on 31st of December in every year. The latest performance being compared with company’s statements

over the last five years starting 2010 for showing trends. Finally, recommendations and suggestions have been

made to ensure the revenue of the company and reduce the liabilities while improving the stability of the

company.

Keywords: financial ratio, Adidas, Financial analysis

1. Introduction

1.1 Purpose of the report

The purpose of this report is to analyse the financial performance, and propose recommendations for financial

management that will improve the future financial effectiveness, ensure growth and consolidate the market

position of the Adidas organisation. During the discussion, key ratios have been compared and analysed from

previous year and with the main competitors which will help to envisage actual finance performance of the

organisation. It will help to suggest appropriate recommendations which will improve the liquidity and

profitability of the company through implementation.

1.2 Back ground of the organisation

Adidas is a German multinational corporation that designs and manufactures sports shoes, clothing and

accessories founded in 1949 by Adolf Dassler. The Adidas group consists of Reebok sportswear company,

TaylorMade Golf Company, FC Bayern Munich and Runtastic that headquarter based in Olympiaring,

Herzogenaurach, Germany.

German national football team victory in 1954 world cup brought Adidas name on football pitches

everywhere as they made the lightweight football boots for national team. According to Forbes (2015) Adidas

brand value is more than $17.1 billion. Today Adidas has 1746 concept stores, 779 factory outlets and 316

concession corners and other around the world (Statista, 2015). The Adidas Group's net sales amounted to about

€14.53 billion in 2014 and have more than 53731 employees from around the world (Adidas, 2014). The

mission of adidas Group, strives to be the global leader in the sporting goods industry with brands built on a

passion for sports and a sporting lifestyle.

2. Financial performance

2.1 Finance

The financial statement is the basic document which provides information and recommendation about the

financial position, performance and changes in financial position in an organisation (Atrill & McLaney, 2002).

Various people are interested about the financial statement such as shareholders, external capital providers,

existing and potential investors, lenders, other creditors, government departments, employees, client, suppliers,

competitors and stockbrokers (Du Toit, Erasmus, Kotze, Ngwenya, Thomas, & Viviers, 2014). Financial

performance refers to the act of performing financial activity and indicates whether financial objectives are being

or have been accomplished (Knott, 2004). Measuring financial performance is based on a given period of time

and similar firms across the same industry or used to compare industries or sectors in aggregation (Atrill &

McLaney, 2002).

Measuring financial performance is required to maintain organisation’s liquidity in day-to-day

operation to ensure its smooth running and to meet its obligation (Eljelly, 2004). The analysis indicates firm’s

liquidity, profitability and makes a platform for comparison with other competitors indicating that the business is

conducted in a rational and normal way; ensuring enough returns to the shareholders to maintain at least its

market value (Altman, 1968). Decisions which are based on finance performance analysis help the maximization

of shareholders or owners wealth (Panwala, 2009).

This report has analysed Adidas group financial reports which are ending December 31st 2014. The

analysis is based on balance sheet, the income statement and cash flow statement which have been attached in

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

75

the Appendices. The income statement set out the summary of the trading events that will affect the capital of

the business and shows whether the company is selling its product or service, for less or more than its cost of

deliver them to its customers (McLaney, 2006). Balance sheet is a snapshot of the company’s assets, liabilities

and equity at the end of the fiscal year (Brigham & Ehrhardt, 2013). The statement of cash flow indicates the

summary of organisation’s ability to generate cash (Du Toit et al.,2014).

2.2 Horizontal Analysis

Horizontal analysis is used to identify the changes in the amounts of corresponding financial statement items

over a period of time (Gibson, 2010). The analysis is based on two periods of accounts and earliest period is

usually used as the base period then all later period are compared with items on the statements of the base period

(Bernstein & Wild, 1993). The based period amount is calculated as 100% then each following period is

expressed as a percentage of the amount in the based year.

The horizontal analysis is useful to see the impact of operational results on a company's financial

condition over the review period. But the common problem is that aggregation of information in the financial

statements could change over time, due to ongoing changes on the accounts (Fridson & Alvarez, 2011).

Table; 1. Horizontal Analysis

Item 2014 2013 Change

(€ in million) (€ in million) %

Net Sales 14,534 14,203 2.3

Cost of Sales 7,610 7,202 5.7

Gross Profit 6,924 7,001 -1.1

Operating Expenses 6,203 6,013 3.2

Operating Profit 883 1,181 -25.2

Income before Taxes 835 1,113 -24.9

Net Income 496 790 -37.2

Finger; 1. Horizontal Analysis

Horizontal analysis has been done for income statement in financial year 2013 and 2014 above.

Comparing with 2013, Net income was declined 37.2% even though the net sales were increased by 2.3%. These

charts illustrate increasing cost of sales by 5.7% and operating expenses by 3.2% directly affected on declining

net income. Therefore Adidas should concern about reducing cost of sales and operating expenses to maximise

the net income in next years. Effective and low cost communication medium utilised to reduce the cost of sales

and reduction of additional employees would be another option to minimise the operation cost as salaries and

wages are the highest part of the operation cost (Eljelly, 2004).

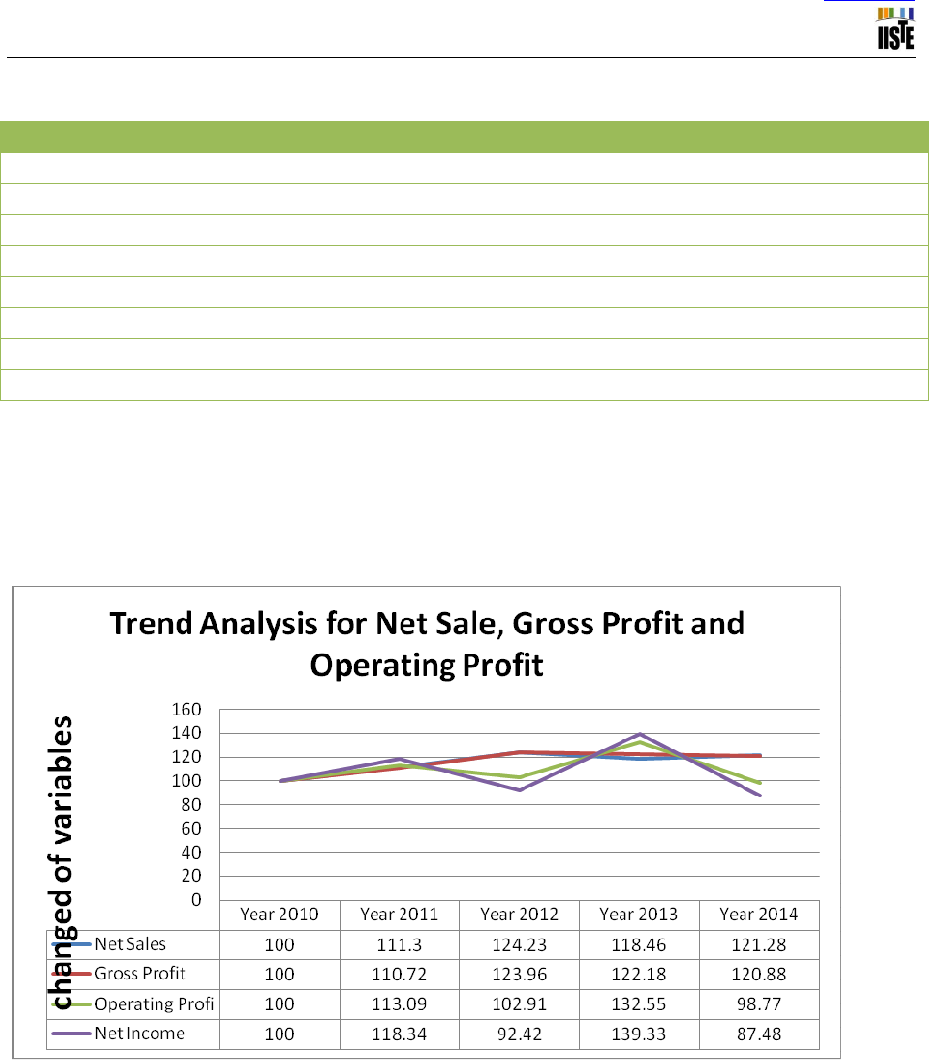

2.3 Trend Analysis

This analysis is similar to horizontal analysis, but evaluates an organization’s financial information more over

two period of time (Fridson & Alvarez, 2011).Therefore this analysis helps to grasp the changes in the selected

variables more easily. Evaluating several years’ data will help to forecast future financial trends accurately in an

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

76

organisation (Bernstein & Wild, 1993).

Table; 2. Trend Analysis

Column1 2010 2011 2012 2013 2014

Net Sales 11,990 13,344 14,883 14,203 14,534

100 111.3 124.23 118.46 121.28

Gross Profit 5,730 6,344 7,103 7,001 6,924

100 110.72 123.96 122.18 120.88

Operating Profit 894 1,011 920 1,181 883

100 113.09 102.91 132.55 98.77

Net Income 567 671 524 790 496

100 118.34 92.42 139.33 87.48

This trend of income statement illustrates the analysis on the different period of net sales, gross profit

and operating profit assuming 2010 as base. While comparing the value to 2006, the absolute value of net sales

and gross profit are in increasing trend. The absolute value of operation profits has changed on year to year and

at 2014 value of operating profit is low in compared to 2010. It mean, Adidas had more operating cost in 2012

and it affected on reducing the net income. The net income is mainly depending on operating expenses. When

the operating cost went down in 2013 net income increased parallel with the operating profit. But when

operating profit went down (operating expenses increased) by 98.77%, net income also went down by 87.48%.

Finger; 2 Trend Analysis

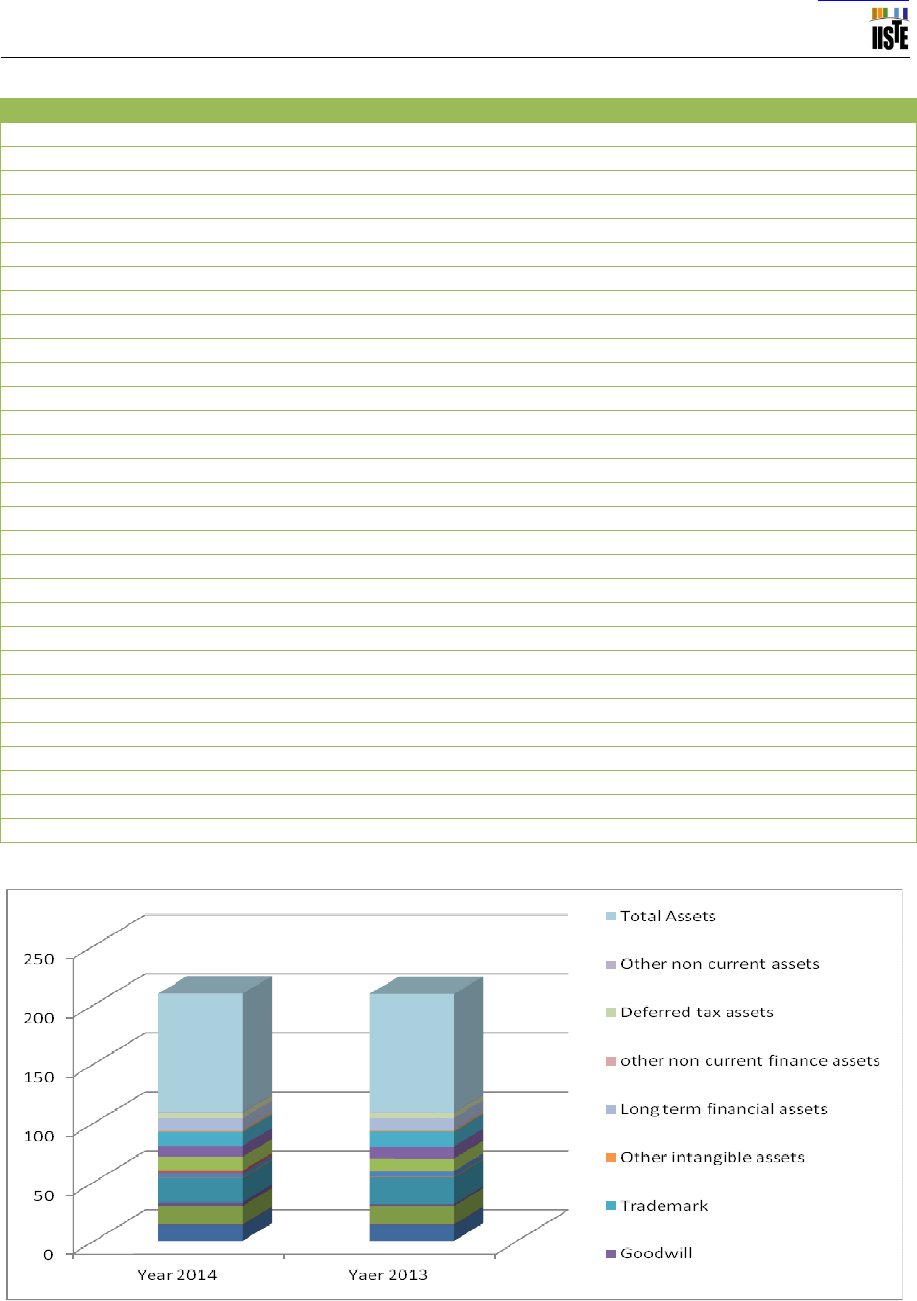

2.4 Vertical Analysis

This is a comparative analysis of a financial statement where each line item on accounts is listed as a percentage

of another item (Shaoul, 1998). For example, when analysing the vertical amounts on the balance sheet every

amount on the balance sheet is restated to be a percentage of total assets. One of the main advantages of this

analysis is that the balance sheet can be easily compared to any size of organisation and it will help to understand

relative annual changes within one business (Fridson & Alvarez, 2011).

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

77

Table; 3. Vertical Analysis

Assets 2014

%

2013

%

cash and cash equivalents 1,683 13.55 1,587 13.68

Short-term financial assets 5 0.4 41 0.35

Account receivable 1,946 15.67 1,809 15.6

Other current finance assets 398 3.2 183 1.58

inventories 2,526 20.34 2,634 22.7

Income tax receivable 92 0.74 86 0.74

other current assets 425 3.42 506 4.38

Assets classified held for sale 272 2.19 11 0.09

Total current assets 7,347 59.17 6,857 59.11

Property, Plant and Equipment 1,454 11.7 1,238 10.67

Goodwill 1,169 9.41 1,204 10.38

Trademark 1,432 11.53 1,419 12.23

Other intangible assets 162 1.3 164 1.41

Long term financial assets 129 10.03 120 1.03

Other non curent finance assets 42 0.34 30 0.26

Deferred tax assets 577 4.65 486 4.19

Other non-current assets 105 0.86 81 0.69

Total non-current assets 5,070 40.83 4,742 40.88

Total assets 12,417 100 11,599 100

Liabilities and Equity

Short-term borrowing 288 2.32 681 5.87

Account Payable 288 2.32 681 5.87

Income taxes 294 2.37 240 2.07

Total current liabilities 4,378 35.25 4,732 40.78

Total non-current liabilities 2,422 19.51 1,386 11.95

Reserves 581 4.68 321 2.77

Shareholder equity 5,624 45.24 5,489 47.32

Total equity 5,618 45.25 5,481 47.25

Total liabilities and equity 12,417 100 11,599 100

Finger;3. Vertical Analysis

One of main issues when using vertical analysis for balance sheet is what to use as the benchmark in the

percentage calculation (Atrill & McLaney, 2002). The usual benchmarks are total asset or total liabilities when

calculating assets and liability line item percentages, and the total of all equity accounts when calculating all

equity line item percentages.

The analysis shows that the total assets of the company increased from 2013 to 2014 and there is a

slight increase in total current assets. Adidas has 59.17% higher the proportion of current assets in case to cover

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

78

all current and non-current liabilities which is total 54.76%. The company also has 13.55% of cash and cash

equivalents which can cover short-term borrowing (2.32%) account payable (2.32%) income taxes (2.37%) total

amount of 7.01%. The analysis shows that, Adidas strong working capital position and its ability to meet its

near-term obligations.

2.5 Financial Ratios

A sustainable organisation requires effective planning and financial management (Lewellen, 2004). Ratio

analysis provides key indicators of organisational performance which will help to understand the organisation

financial results and trends over time (Barnes, 1987). The ratio analysis reveals valuable information about

organisation’s financial attributes and it helps to compare organisation’s ratio with prior periods, competitor or

industry average, that will benefit to understand the current business position of the organisation (Schoenebeck

& Holtzman, 2013). Whittington (2007) has recognised that two principal uses of financial ratios; normative use

ratio for organisation’s ratio compared with a standard and positive use in identifying empirical relationships

such as predictive purposes.

Summarising quite complex accounting details into a relatively small number of key indicators is one of

main reasons to calculate ratio (McLaney, 2006). However, deferent users have different interests in financial

information which will determine the ratios they need to use (Atrill & McLaney, 2002). For example, investors

are interested more in profitability ratios, liquidity ratios and solvency ratios. Therefore it is important to identify

the objective of the finance report before calculating the ratios for generates useful data (Walsh, 2008).

2.6 Key Ratios

The ratios to be analysed are credit payment period, return capital employed, current ratio, net profit margin and

earnings per share. These ratios influence on financial health of the company and important for managers,

stakeholders, investors, lenders and suppliers. These ratios are a part of ratios such as liquidity ratios, productive

ratios, profitability ratios investment ratios and overall performance ratios (appendix, I).

Table; 4 Key Ratios Analysis

Item 2014 year 2013 year Change %

Creditor payment period 79.2 days 92.5 days -14.38

Return capital employed € 0.1 (10%) € 0.16 (16%) -37.5

Current Ratio 1.7 : 1 1.4 : 1 21.42

Interest cover 13.50 15.20 -11.84

Earnings per share € 2.43 € 3.78 -35.71

Finger; 4 Percentage of Key Ratios Change (based on 2013)

Creditor payment period is a liquidity ratio that indicates an organisation’s capacity to pay off its

account payable (Bernstein & Wild, 1993). This ratio is a useful calculation to assess the liquidity position of a

business (Australian shareholders’ association, 2010). It shows how many times an organisation can pay off their

average accounts payable balance during the one financial year.

In 2013, Adidas took more than 92 days to pay their traders. In general organisations that need to

maximise their cash flow have to take as long as possible to pay its bills (Brigham & Houston, 2004). But 92

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

79

days is a far long time, it can be seen when compared with Nike which took just 24 days to pay off their bills in

2013 financial year (Appendix.2). There is several risk associated with taking more time than their agreement

with the supplier such as loss of supplier goodwill and potential for late-payment charge and threat of legal

actions (Bernstein & Wild, 1993 ). However, in 2014 Adidas was able to reduce the payment days for 79 day it

was 14.38% reduction when it compare to 2013. This could be good news for suppliers and lenders of the Adidas

Company.

Return on capital employed (ROCE) is a profitability ratio which indicates how efficiently an

organisation can generate profits from its capital employed by comparing profit before interest and tax to capital

employed (Keown et al., 2008). This ratio calculation illustrates how much profit each Euros of employed capital

generate; a higher number of ratio mean more Euros of profits generated by each Euros of capital employed.

Adidas generated € 0.16 for € 1 investment in 2013 and was reduced to € 0.10 by 37.5% in 2014. These

numbers indicate that company assets’ performance is struggling and the company long term financial problem.

In 2013 and 2014 Nike had € 0.24 ($.026) and €0.22 ($0.22) ratio amounts respectively (appendix.2). According

to the return on capital employed calculation, Adidas is below in long term financial performance than Nike by

33.33% in 2013 and 54.54% in 2014. This mean Adidas’ amounts of assets are hindering them to achieve a high

return. Adidas Company is declining the money return on every euro invested in the business and burns up more

capital to generate profits. Decline in ROCE could signal the loss of competitive advantage and bad news for

stakeholders and investor.

The current ratio is a liquidity ratio which shows the proportion of current assets of a company in

relation to its current liabilities (Bernstein & Wild, 1993). The calculation shows a company’s ability to repay

short-term liabilities. The ratio of 2:1 consider as the benchmark, however it could vary across industries (Atrill

& McLaney, 2002).

In 2013, Adidas 1.4:1 ratio which indicate the sufficient money to meet current liabilities. However,

that amount is far below to the benchmark. It indicates the risk of unable to pay off its obligations. End of 2014

Adidas came to good financial health which indicates 1.7:1 amount in current ratio. This ratio reflects using the

current ratio in different ways as high current ratio may suggest company is not managing its working capital

well (Keown et al., 2008). But it could not be easily liquidated all current assets in a company as current ratio

assumed; this is one of error in using this ratio (Australian shareholders’ association, 2010).

The interest cover ratio is calculated as the ability of a company to pay the interest on its outstanding

debt (Bernstein & Wild, 1993). It helps to calculate how many times a company could pay its current interest

payment with its available earnings. A company’s capacity to meet its interest obligations is an aspect of a

company’s solvency as it is an important factor in the return for stakeholders (Brigham & Houston, 2004).

Therefore, the ratio is used to determine the risk of lending funds to a company by creditors, lenders, and

investors (Bernstein & Wild, 1993 ).

Adidas had 15.20 and 13.50 interest cover ratios in 2013 and 2014 respectively. In general, interest

cover ratio warning sign margin is 2.5, that the company should be careful about their future financial situation

(Keown et al., 2008). In this situation, Adidas is in good financial health with confidence to pay their interest for

lenders. But they have to consider about 11.84% reduction of their ability in 2014.

The earning per share ratio indicates the amount of company’s profit allocated each outstanding share

of common stock (Australian shareholders’ association, 2010). Indicating high amount of earning per share ratio

signals potential of generating a significant dividend for investors (Bernstein & Wild, 1993). Adidas had € 3.78

earnings per share in 2013 and it reduced to € 2.43 in 2014. Reduced net income in 2014 directly effected on this

sudden decline. Somehow, Adidas shareholders can satisfy the earning per share in Adidas when compared to

Nike as they generated € 3.09 ($3.35) per share in 2014.

In summary, Adidas had some financial difficulties in 2014 when compared to 2013 financial year.

Especially company has trouble on capital efficiency as employed capital is not generating sufficient income.

However, identifying a company’s financial situation is more difficult and it is important not to rely on few

financial measurements (Brigham & Houston, 2004).

3. Conclusion

The company is performing well and it will continue to make profit and revenues for next financial years.

However Adidas could be affected with considerable risks according to high operating expenses which hinder

the overall performance and net income. The company had € 0.1 ROCE that means less efficiency in capital

employed in the company. Therefore capital should be invested on a productive manner and unproductivity

assets such as vacation properties and personal use vehicles should be sold as soon as possible. Capital should

invest on most productive assets which will help to increase the revenue such as equipment for factory, vehicles

for sales and showrooms. Adidas had €14,534 net sales in 2014 while their main competitor Nike had €25531

($27799). Next financial year, Sale of the products should be increased along with their prices in order to acquire

more working capital which will help to fund further competitors. Increasing operating cost is the main reason of

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

80

the decline of the net profit in Adidas Company. The earning per share declined to € 2.43 in 2014 due to this

reason. Therefore, the company should establish cost cutting goals, maximise employees task efficiency and

consider about outsourcing. The company should implement quality assurance practice and procedures

throughout the entire business for increase sales.

References

Adidas (2014). Adidas group profile

Available at: http://www.adidas-group.com/en/group/profile/ (Accessed 15th December 2015).

Atrill, P., & McLaney, E. J. (2002). Financial accounting for non-specialists. Financial Times Prentice Hall.

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The

journal of finance, 23(4), 589-609.

Available at: http://onlinelibrary.wiley.com/doi/10.1111/j.1540-6261.1968.tb00843.x/pdf

Australian shareholders’ association. (2010). The top 15 financial ratio. Available at: Available at:

http://members.lincolnindicators.com.au/content/filestore/research/top-15-financial-ratios.pdf

Barnes, P. (1987). The analysis and use of financial ratios: A review article.Journal of Business Finance &

Accounting, 14(4), 449-461.

Available at: http://onlinelibrary.wiley.com/doi/10.1111/j.1468-5957.1987.tb00106.x/abstract

Bernstein, L. A., & Wild, J. J. (1993). Analysis of financial statements. Business One Irwin.

Brigham, E, F. & Houston, J, F. (2004). Fundamentals of financial management. Mason, ohio: Thomson/South-

Western.

Brigham, E., & Ehrhardt, M. (2013). Financial management: theory & practice. Cengage Learning.

Du Toit, E., Erasmus, P., Kotze, L., Ngwenya, S., Thomas, K., & Viviers, S. (2014). Corporate Finance: A South

African Perspective. OUP Catalogue.

Eljelly, A. M. (2004). Liquidity-profitability tradeoff: an empirical investigation in an emerging

market. International Journal of Commerce and Management,14(2), 48-61.

Available at: http://www.emeraldinsight.com/doi/abs/10.1108/10569210480000179

Forbes (2015). The world most valuable brands

Available at: http://www.forbes.com/companies/adidas/

Fridson, M. S., & Alvarez, F. (2011). Financial statement analysis: a practitioner's guide (Vol. 597). John Wiley

& Sons.

Gibson, C. (2010). Financial reporting and analysis: Using financial accounting information. Cengage Learning.

Keown, A. J., Martin, J. D. & William, P. J. (2008). Foundation of Finance. 6th ed. Person Prentice Hall : New

Jersey .

Knott, G. (2004). Financial Management. 4th ed. London: Palgrve Macmillan.

Lewellen, J. (2004). Predicting returns with financial ratios. Journal of Financial Economics, 74(2), 209-235.

Available at: http://www.sciencedirect.com/science/article/pii/S0304405X04000686

McLaney, E. J. (2006). Business finance: theory and practice. Pearson Education.

Mott, G. (2012). Accounting for non-accountants: a manual for managers and students. Kogan Page Publishers.

Schoenebeck, K. P., & Holtzman, M. P. (2013). Interpreting and analyzing financial statements. Pearson Higher

Ed.

Shaoul, J. (1998). Critical financial analysis and accounting for stakeholders.Critical Perspectives on

Accounting, 9(2), 235-249.

Available at: http://www.sciencedirect.com/science/article/pii/S1045235497901726

Walsh, C. (2008). Key management ratios: The 100+ ratios every manager needs to know. Pearson Education.

Whittington, G. (2007). Some basic properties of accounting ratios.Profitability, Accounting Theory and

Methodology: The Selected Essays of Geoffrey Whittington, 7(2), 123.

Panwala, M. (2009). Dimensions of liquidity management-A case study of the surat textile traders co-operative

bank ltd., Surat. National Journal of System and Information Technology, 2(1), 117.

Statista (2015). Number of retail stores of the adidas Group worldwide from 2008 to 2014, by store type

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

81

Appendices

Appendix I. Calculation for ratios

Current Ratio Calculation Ratios

2014 7,347/4,378 1.7 : 1

2013 6857/4732 1.4 : 1

Quick Assets Ratio

2014 (7,347-2,526)/4,378 0.9

2013 (6,857/2,634)/4732 0.9

Cash Ratio

2014 1,683/4,378 0.4

2013 1,587/4,732 0.3

Stock Turnover

2014 7,610/{2/(2,526+2,634)} 3

2013 7,202/(2,634+2,486)} 2.8

Average time in stock

2014 (2,526/7,610)365 121.2 days

2013 (2,634/7,202)365 133.5 days

Turnover per Employee

2014 14,534/49,808 0.27

2013 14,203/53,731 0.29

Asset Turnover

2014 14,534/(12,417-4,378) 1.8

2013 14,203/(11,599-4,732) 2.1

Fixed Asset Turnover

2014 14,534/5,070 2.9

2013 14,203/4,742 3

Working capital turnover

2014 14,534/(7,347-4,378) 4.9

2013 14,203/(6,857-4,732) 6.7

Return capital employed

2014 835/(12,417-4,378) 0.1

1,113/(11,599-4,732) 0.16

Average turnover per Employee

2014 14,534/{2/ (46,306+49,808)} 0.28

2013 14,203/{2/ (49,808+53,731)} 0.29

Gross profit margin

2014 (6,924/14,534)100 47.60%

2013 (7,001/14,203)100 49.30%

Net profit margin

2014 (496/14,534)100 3.40%

2013 (790/14,203)100 5.60%

Earning per share

2014 (496,000,000/204,327,044) € 2.43

2013 (790,000,000/209,216,186) € 3.78

Earning yield

2014 (2.43/57.62) € 0.04

2013 (3.78/92.64) € 0.04

Dividend cover

2014 (496/314) 1.6

2013 (790/282) 2.8

Dividend yield

2014 (314,000,000/204,327,044)/ 57.62 € 0.03

2013 (282,000,000/209,216,186)/92.64 € 0.01

Interest cover

2014 835/62 € 13.50

2013 1,181/73 € 15.20

Return on capital employed

2014 835/(12,417-4,378) 0.1

2013 1,113/(11,599-4,732) 0.16

Return on shareholder's funds

2014 (568/5,624)100 10.10%

2013 (839/5,481)100 15.30%

Debt collection period

2014 (1,946/14,534)365 48.9 days

2013 ((1,809/14,203)365 46.5 days

Creditor payment period

2014 (1,652/7,610)365 79.2 days

2013 (1,825/7,202)365 92.5 days

European Journal of Business and Management www.iiste.org

ISSN 2222-1905 (Paper) ISSN 2222-2839 (Online)

Vol.8, No.11, 2016

82

Appendix II. Nike ratios Calculation

Creditor payment period (Nike) Calculation Ratios

2014 (1,930/27,799)365 25.3

2013 (1,669/25,313)365 24

Return capital emplyeed(Nike)

2014 3,544/(18,594-5,027) 0.24

2013 3,256/(17,545-5,027) 0.26

Earning per share Nike

2014 2,693/883.4 $3.35