THE PRESIDENT’S FRAMEWORK FOR

BUSINESS TAX REFORM:

AN UPDATE

A Joint Report by

The White House and the Department of the Treasury

April 2016

1

The President’s Framework for Business

Tax Reform: An Update

Contents

Introduction .................................................................................................................................................. 2

I. The Need for Reform ............................................................................................................................ 4

Distortions in the Form of Investment by Industry and Asset ...................................................................... 6

Distortions in the Financing of Investment ................................................................................................... 8

Distortions in the Organizational Form of Businesses .................................................................................. 9

Distortions in the Location of Production and Allocation of Profits ........................................................... 11

Positive and Negative Externalities of Business Behavior .......................................................................... 16

II. The President’s Framework for Business Tax Reform ...................................................................... 17

Eliminate Loopholes and Subsidies, Broaden the Base, and Cut the Corporate Tax Rate ......................... 17

Strengthen American Innovation, Clean Energy, and Manufacturing ........................................................ 21

Strengthen the International Tax System to Encourage Domestic Investment ......................................... 23

Simplify and Cut Taxes for America’s Small Businesses .............................................................................. 26

Restore Fiscal Responsibility ....................................................................................................................... 27

Conclusion .................................................................................................................................................. 29

2

Introduction

America’s system of business taxation is in need of reform. The United States has a relatively narrow

corporate tax base compared to other countries—a tax base reduced by loopholes, tax expenditures, and

tax planning. The resulting system distorts choices, such as where to produce, what to invest in, how to

finance a business, and what business form to use. And it does too little to encourage job creation and

investment in the United States while allowing firms to benefit from incentives to locate production and

shift profits overseas. The system is also too complicated—especially for America’s small businesses.

In 2012, the White House and the Treasury Department released The President’s Framework for Business

Tax Reform, outlining the need for reform of the business tax system and presenting the five elements of

reform as envisioned by the President: eliminating loopholes and subsidies to broaden the base and lower

the rate, strengthening American manufacturing and innovation, strengthening the international tax

system, simplifying and cutting taxes for America’s small businesses, and restoring fiscal responsibility

without adding to the deficit. Since then, Members of Congress from both parties have put forward

thoughtful tax reform proposals, including former House Ways and Means Committee Chairman Dave

Camp and former Senate Finance Committee Chairman Max Baucus. Last year, a number of Senate

Finance Committee working groups continued the reform effort, releasing a set of reports on different

topics in tax reform. While the Administration does not agree with every component of these proposals,

all of these efforts have underscored the need for and the urgency of business tax reform and advanced

the discussion in meaningful ways.

The urgency of closing loopholes and reforming the tax system more broadly has grown since the

Framework was released in 2012. Particularly notable is the recent wave of corporate inversions,

transactions in which a U.S. corporation shifts its legal residence abroad to be deemed a foreign company

for U.S. tax purposes, even as it frequently keeps management and business operations here. The

Congressional Research Service identified 23 inversions since 2012, compared to only three in total in

2010 and 2011. In September 2014, the Treasury took action to limit companies’ ability to undertake these

transactions and reduce the economic benefits of inversions, a step that observers have credited with

slowing the pace of inversions, and followed up with further steps in November 2015 and April 2016.

However, a complete solution to the problem requires Congressional action. The President’s Budget has

proposed to stop corporate inversions and shut down a key strategy inverted firms use to shift taxable

income outside the United States, but Congress has failed to act on these proposals. As a result, inversions

continue to erode the U.S. tax base unnecessarily.

While inversions are a particularly prominent symptom of a broken tax system, and one that should be

addressed immediately even absent broader business tax reform, the issues run much deeper. Even

without changing the address on their tax returns, corporations can shift profits to low-tax countries in

order to reduce their worldwide tax liability. Academic research suggests that the cost of profit shifting

has increased substantially in recent years and may now cost the United States more than $100 billion per

year in foregone tax revenue. The global importance of this issue is highlighted by the successful

development of comprehensive recommendations to address base erosion and profit shifting (BEPS) by

the OECD BEPS Project, which were approved by the G-20 nations in November.

In the face of these challenges, inaction is not an option. The combination of the relatively high U.S.

corporate rate and our complicated system for taxing multinational businesses has encouraged and

3

facilitated the erosion of the tax base. It also has made America a less attractive place to start and grow

an international business, and complicated and distorted business decisions. Unwarranted tax

preferences continue to narrow the tax base, requiring higher tax rates than would otherwise be

necessary and encouraging investments in less-productive activities. Our high corporate tax rate,

combined with other structural features of the tax code, penalizes traditional “C corporations” relative to

other business forms and results in a significant tax advantage for financing investments using debt rather

than equity, which, in turn, imposes broader economic costs from bankruptcy and financial fragility. Tax

expenditures that benefit one industry over another, or one type of investment over another, encourage

firms to seek out investments that receive preferential tax treatment but do not necessarily result in

higher economic or social returns.

Reform should not only eliminate undesirable incentives; it should also provide incentives to support

economic activities that benefit the broader economy. For this reason, policies to strengthen innovation,

clean energy, and manufacturing, in addition to supporting America’s small businesses, are important

components of the President’s approach to business tax reform. This agenda includes an expanded and

simplified tax credit for research activities, enhanced provisions allowing small firms to write off more of

the cost of new investments, and tax credits to support investments in clean energy. In December 2015,

Congress enacted several important pieces of this agenda, including making permanent the Research and

Experimentation (R&E) tax credit for the first time since its initial enactment in the early 1980s, enhancing

incentives for small business investment, and extending tax credits for renewable energy production and

investments in clean energy technology. However, while these steps reflect significant improvements in

the law, the hard work of tax reform remains to be done. Moreover, in enacting these policies Congress

did not offset their cost as it should have, increasing the importance of restoring fiscal responsibility to

the tax reform effort. Consistent with the President’s long-standing principle that business tax reform

must be revenue neutral in the long run, reform should be fully paid for, including paying for those

provisions that have already been enacted.

This update reviews the need for reform of the U.S. business tax system and the key elements of the

President’s Framework. In addition, it details the specific proposals the President has put forward,

including a comprehensive approach to reforming the international tax system.

4

I. The Need for Reform

The U.S. corporate income tax combines the highest statutory rate among advanced economies with a

base narrowed by loopholes, tax expenditures, and tax planning strategies. In addition to the corporate

income tax, the United States operates a second, parallel system of business taxation for pass-through

entities—businesses whose earnings are taxed on the owners’ income tax returns rather than a separate

entity-level return. The U.S. business tax system allows some companies to avoid significant tax liability,

while others pay tax at a high rate. It distorts important economic decisions about where to produce, how

to finance investments, and what industries and assets to invest in. The system also is too complicated,

and that complexity hurts America’s small businesses and allows large corporations to reduce their tax

liability by shifting profits around the globe.

The current business tax system reduces productivity, output, and wages through its impact on the

location of production and allocation of profits, the means of financing new investments, and the

P

RESIDENT

O

BAMA

’

S

F

IVE

E

LEMENTS

O

F

B

USINESS

T

AX

R

EFORM

I. Eliminate dozens of tax loopholes and subsidies, broaden the base, and cut the corporate

tax rate to spur growth in America: The Framework would eliminate dozens of different tax

expenditures and fundamentally reform the business tax base to reduce distortions that hurt

productivity and growth. It would reinvest these savings to lower the corporate tax rate to

28 percent, putting the United States in line with major competitor countries and

encouraging greater investment in America.

II. Strengthen American innovation, clean energy, and manufacturing: The Framework would

expand incentives for research and development and clean energy while also refocusing the

manufacturing deduction.

III. Strengthen the international tax system, including establishing a new minimum tax on

foreign earnings to encourage domestic investment: Our tax system should not give

companies an incentive to locate production overseas or engage in accounting games to

shift profits abroad, eroding the U.S. tax base. Introducing a 19 percent minimum tax on

foreign earnings would help address profit shifting and discourage a global race to the

bottom in tax rates.

IV. Simplify and cut taxes for America’s small businesses: Tax reform should make tax filing

simpler for small businesses and entrepreneurs so that they can focus on growing their

businesses rather than filling out tax returns.

V. Restore fiscal responsibility and not add a dime to the deficit: Business tax reform should

be fully paid for, which includes paying for provisions Congress has already enacted without

offsets.

5

allocation of investment across assets and industries.

1

The high statutory rate and complicated rules for

taxing income in different countries can discourage firms from locating highly profitable investments in

the United States. Reduced investment in turn reduces U.S. productivity and output. Loopholes that allow

multinational firms to shift profits to low-tax jurisdictions abroad require higher taxes on domestic

businesses and families to make up for the lost revenue. The significant tax preference for debt

encourages excessive borrowing, which in turn increases bankruptcy costs and financial fragility, and thus

reduces macroeconomic stability. Tax expenditures that privilege certain industries and assets encourage

investment in low-return, lightly-taxed projects while high-return, but more heavily-taxed, projects are

ignored.

The distortions caused by the U.S. corporate tax system are magnified by the relatively high statutory tax

rate. The higher the tax rate, the more a firm benefits by claiming a special deduction, reducing its taxable

income by increasing borrowing, or using aggressive strategies to shift profits offshore. Income shifting

has also grown worse as the wedge between the U.S. statutory rate and rates in other countries has

widened, and the absence of reform has left strategies used to shift income untouched.

Focusing exclusively on the U.S. statutory corporate tax rate, however, does not give a complete picture

of how the tax code affects decision-making and the competitiveness of the U.S. economy and U.S. firms

in world markets. Other indicators tell a more complete story. For example, the effective marginal tax rate

on corporate investment in the United States—the expected tax rate on a hypothetical new investment—

is slightly below the average for the G-7 (see Table 1).

2

1

For more discussion of the economic case for business tax reform, see: Council of Economic Advisers. “Economic

Report of the President.” 2015. Chapter 5.

https://www.whitehouse.gov/sites/default/files/docs/cea_2015_erp_complete.pdf

2

The effective marginal tax rates (EMTRs) reported in Table 1 take into account temporary incentives in place in

2015, including 50 percent bonus depreciation in the United States. EMTRs reported elsewhere in this update do

not take these temporary incentives into account.

Statutory Corporate Tax Rate Effective Marginal Tax Rate

Country

(including subnational taxes) (including subnational taxes)

a

Canada 26.3 12.5

France 34.4 24.0

Germany 30.2 21.2

Italy

b

31.3

5.2

Japan 32.1 24.5

United Kingdom 20.0 19.0

United States 39.0

18.1

G-7 Average Excluding the U.S.

c

29.6 19.4

Table 1: G-7 Statutory Corporate Tax Rates (in Percent), 2015

a.

EMTRs reported in this table include temporary incentives for investment, including 50% bonus depreciation in the United States.

b.

The statutory rate for Italy includes the 3.9 percent IRAP regional production tax not in the reported OECD rate.

c.

The G-7 average is calculated using 2014 gross domestic product (in current US dollars) as weights.

Source:

OECD and U.S. Department of the Treasury, Office of Tax Analysis.

6

Business tax reform must consider and balance different measures. The fact that U.S. firms face a

relatively high statutory rate but do not pay similarly high rates on marginal investments suggests the

need for a reform of the corporate tax system that lowers the statutory rate while broadening the tax

base to maintain at least the same level of revenue. A broader tax base with fewer unjustified loopholes

and subsidies would level the effective marginal tax rates, regardless of the type and location of

investments. As a result, decisions would more likely be made for business reasons and not for tax

reasons, thus improving the overall quality of investment.

Reducing the number of tax expenditures and loopholes would reduce the complexity of the tax system

and lessen the tax compliance burden for large corporations and small businesses alike. The proliferation

of tax preferences has created the need for additional rules and regulations to ensure that incentives are

limited to their intended beneficiaries. Small business owners have to spend time and money learning

about tax incentives and often rely on third parties to help them navigate the thicket of complex tax

rules, while large corporations employ lawyers and accountants to structure transactions to minimize

taxes. The IRS has to spend resources monitoring and enforcing the rules. Disputes invariably arise

between the IRS and taxpayers, and society expends resources adjudicating these disputes.

In sum, the tax expenditures and loopholes in the U.S. tax system, together with the structure of the

corporate tax system, produce significant distortions that can result in a less efficient allocation of capital,

reducing the productive capacity of the economy and U.S. living standards. The distortions created by the

tax system are explored further below.

Distortions in the Form of Investment by Industry and Asset

Tax expenditures vary dramatically by industry. These differences manifest themselves in disparate

average tax rates across industries. Table 2 shows effective actual federal corporate tax rates by industry

for the period 2007-2010. The overall average federal tax rate for U.S. corporations was 23 percent—well

below the federal statutory rate of 35 percent. Within that average, there was considerable variation by

industry—from a low of a 14.5 percent average tax rate for utilities to a 30.3 percent average tax rate for

construction. Tax preferences also lead to different effective marginal tax rates across types of assets, as

Figure 1 illustrates.

7

Industry

Effective Actual Corporate Tax Rate

Utilities 14.5

Leasing 17.7

Transport and Warehouse 18.6

Mining 21.6

Agriculture, Forestry, Fishing 22.0

Real Estate 22.4

Manufacturing 22.4

Insurance 23.1

Finance 23.1

Information 24.2

Wholesale-Retail 27.9

All Services 29.4

Construction 30.3

Average Effective Actual Tax Rate 23.3

Source: U.S. Department of the Treasury, Office of Tax Analysis.

Table 2: Effective Actual Federal Corporate Tax Rates by Industry, 2007-2010

8

The result is a tax system that distorts investment decisions. By allocating capital inefficiently, this system

lowers living standards now

and also could impede technological innovation.

3

The pace of innovation is a

key determinant of economic growth, and innovation tends to be directly related to those areas in which

we make capital investments. Firms do not reap the benefits of technological advances until new capital

is brought into production. Given this interplay between innovation and capital accumulation, the

distortions created by the current corporate income tax may slow economic growth over the long term.

These challenges are particularly notable because subsidies in the current tax code contribute to low

effective tax rates on fossil fuel and other extractive industries, even as we face long-term challenges

requiring us to create a sustainable energy future. Income from an investment in structures for oil

petroleum and natural gas faced an effective total marginal tax rate (including corporate and investor

level taxes) in 2014 of about 19 percent as compared to a 36 percent rate for manufacturing buildings.

4

Distortions in the Financing of Investment

The current corporate tax code encourages corporations to finance themselves with debt rather than

with equity. Specifically, under the current tax code, corporate dividends are not deductible in computing

corporate taxable income, but interest payments are. This disparity creates a sizable wedge in the

effective tax rates applied to returns from investments financed with equity versus debt. Profits

generated by an equity-financed investment will be taxed at the 35 percent corporate rate, leaving 65

percent of the profits for dividend payments to shareholders. In contrast, profits from the same

investment funded by debt will only be taxed to the extent they exceed the associated interest payments.

Once the deductibility of interest is combined with accelerated depreciation, the cost of investments

financed by debt capital declines even further. In fact, on average, debt-financed investments are

subsidized (i.e., their effective marginal tax rate is negative), as income generated by such investments is

more than offset by deductions for interest and accelerated depreciation.

For example, the effective corporate marginal tax rate on new equity-financed investment in equipment

is 27 percent in the United States. At the same time, the effective marginal tax rate on the same

investment made with debt financing is negative 39 percent. Accounting for both corporate and

individual income taxes, the rates are 36 percent for equity-financed investment and close to zero percent

for debt-financed investment (see Figure 2).

3

See, e.g., Alan J. Auerbach and Kevin Hassett. “Tax Policy and Business Fixed Investment in the United States.”

1992. 47 J. Pub. Econ. 141; Dale W. Jorgenson and Kun-Young Yun, “Tax Policy and Capital Allocation.” 1986. 88

Scandinavian J. Econ. 355.

4

Congressional Budget Office. “Taxing Capital Income: Effective Marginal Tax Rates Under 2014 Law and Selected

Policy Options.” 2014.

https://www.cbo.gov/sites/default/files/113th-congress-2013-2014/reports/49817-

Taxing_Capital_Income_0.pdf

9

This tax preference for debt financing has important macroeconomic consequences. First and foremost,

outsized reliance on debt financing can increase the risk of financial distress and thus raise the likelihood

of bankruptcy. Unlike equity financing, which can flexibly absorb losses, debt requires fixed payments of

interest and principal and allows creditors to force a firm into bankruptcy. A solvent firm with limited

liquidity that is struggling to make its debt payments may experience losses of customers, suppliers, and

employees. It may engage in destructive asset “fire sales” and forgo economically profitable investments.

In an attempt to avoid bankruptcy, levered firms faced with financial distress may resort to high-risk

investments. In the broader context, a large bias towards debt financing in the tax code may lead to

greater aggregate leverage, making the broader economy less resilient and more susceptible to severe

downturns.

5

Distortions in the Organizational Form of Businesses

Businesses may be organized under a variety of different forms, including C-corporations, S-corporations,

partnerships, and sole-proprietorships. These organizational forms offer varying legal, regulatory, and tax

treatments. The primary difference in tax treatment lies between C-corporations, on the one hand, and

S-corporations, partnerships, and sole-proprietorships, on the other. C-corporations are subject to the

corporate tax, while pass-through entities are not. (These businesses are known as “pass-through”

entities because profits pass through to owners and owners pay tax on their individual tax returns.)

The combined effect of the differences in tax treatment is a lower effective tax rate for pass-through

entities relative to C-corporations. As shown in Figure 3, the effective marginal tax rate on new

5

See, e.g., Ruud A. De Mooij. “Tax Biases to Debt Finance: Assessing the Problem, Finding Solutions.” 2011. 33

Fiscal Studies 489.

10

investment by C-corporations is now 30 percent, while the effective marginal tax rate on new investment

by pass-through businesses is 25 percent.

6

As a result, companies are increasingly choosing to organize themselves as pass-through businesses in

order to avoid corporate tax liability. Pass-through businesses represented less than one quarter of net

business income in 1980 but about 60 percent of net business income in 2012, the most recent year with

data available (see Figure 4).

7

While nearly all pass-through income in 1980 accrued to sole

proprietorships, the share of income attributable to these entities has decreased over the last three

decades. In their place, partnerships and S corporations have grown from a negligible share of business

income to roughly half.

6

Calculations of the Treasury Office of Tax Analysis.

7

Internal Revenue Service (IRS). “Statistics of Income.” www.irs.gov/taxstats.

11

The ability of pass-through entities to take advantage of preferential tax treatment has placed businesses

organizing as C-corporations at a disadvantage. By allowing pass-through entities preferential treatment,

the tax code distorts choices of organizational form, which can lead to losses in economic efficiency.

8

Distortions in the Location of Production and Allocation of Profits

The U.S. system for taxing multinational corporations rewards U.S. companies that shift their reported

profits abroad to lower-tax jurisdictions and encourages inversions—transactions in which U.S.-based

corporations relocate their tax residence to low-tax countries by merging with a foreign corporation.

These incentives to manipulate tax rules in order to shift profits actually earned in the United States to

low-tax jurisdictions erode the corporate tax base, requiring higher rates elsewhere to achieve the same

revenue. They also impose significant costs on the U.S. economy by creating economic distortions that

sometimes encourage firms to invest and grow business activities abroad rather than at home and by

causing firms to devote resources to tax planning instead of productive investment. At the same time, the

current tax system can impose a relatively heavy tax burden on the income from some investments that

companies must make overseas and that compete with foreign-owned operations which can be taxed at

lower rates, limiting the opportunities of U.S.-based firms and workers.

Several of these problems arise because the current U.S. tax system taxes foreign subsidiaries of U.S.-

based multinationals on their overseas income (net of a tax credit for foreign taxes paid), but only when

that income is repatriated to the United States, a rule called deferral (since it defers taxation of the

8

See, e.g., Austan Goolsbee. “The Impact of the Corporate Income Tax: Evidence from State Organizational Form

Data.” 2004. 88 J. Pub. Econ. 2283; Jeffrey K. Mackie-Mason and Roger H. Gordon. “How Much Do Taxes

Discourage Incorporation?” 1997. 52 J. Fin. 477; Roger H. Gordon and Jeffrey K. Mackie-Mason. “Tax Distortions to

the Choice of Organizational Form.” 1994. 55 J. Pub. Econ. 279.

12

income). Because that income may be retained abroad indefinitely, the result is that firms may never face

U.S. taxes on much of their foreign income, making the system much more like a territorial system—a

system in which taxes are never paid on foreign income—for many companies. Because of deferral, U.S.

corporations have a significant opportunity to reduce overall taxes paid by shifting profits to low-tax

jurisdictions, either by moving their operations and jobs there or by relying on accounting tools and

current transfer pricing practices to shift profits there.

Indeed, because of deferral and other complex rules for the taxation of U.S. multinationals, the U.S. tax

system can create greater incentives to manipulate the location of foreign income than would arise under

either a pure territorial system or a pure worldwide tax system in which all foreign income was taxed

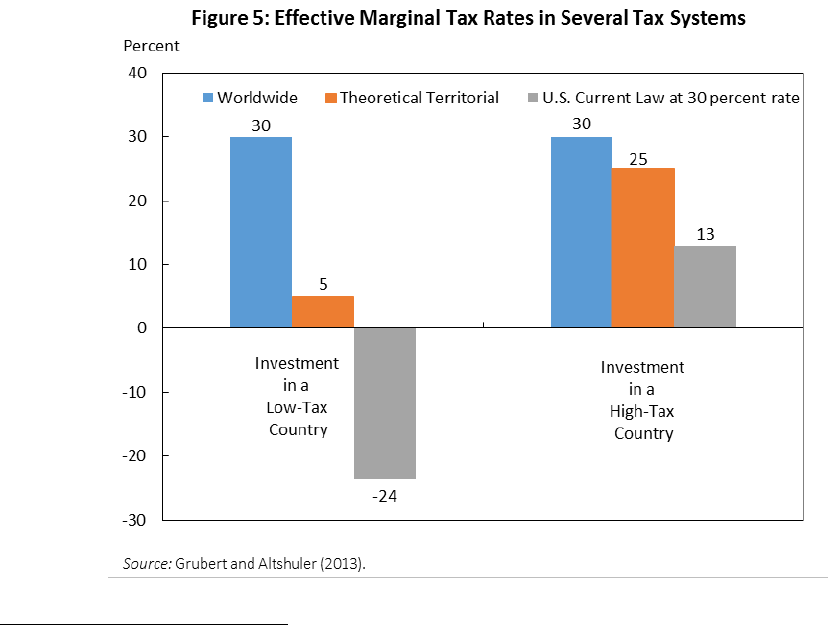

when earned. In particular, simulations by Rosanne Altshuler and Harry Grubert, which assume a statutory

corporate rate of 30 percent but otherwise match the features of current U.S. law, show that the effective

marginal tax rate on investments by a hypothetical U.S. multinational in a low-tax country is -24 percent

after accounting for shifting of intangibles, and the effective marginal tax rate on investments in a high-

tax country is 13 percent after accounting for earnings stripping (Figure 5).

9

These simulations suggest

that, though the United States ostensibly imposes a worldwide tax, the difference in effective marginal

tax rates between high-and low-tax jurisdictions abroad can look more like a territorial system. Moreover,

the tax rates in both high-and low-tax countries can be well below the rates that would apply under either

a true worldwide system or even a theoretically ideal territorial system unaffected by base erosion or

profit shifting.

9

Harry Grubert and Rosanne Altshuler. "Fixing the system: an analysis of alternative proposals for the reform of

international tax.” 2012. 66 Nat. Tax J. 671. For these computations, the low-tax country is assumed to have a

statutory rate of 5 percent and the high-tax country a rate of 25 percent. The activities in each country and the

associated tax planning strategies correspond to common behavior of U.S. companies in such countries.

13

Evidence shows that U.S. multinationals’ decisions about where to invest are sensitive to effective tax

rates in foreign jurisdictions.

10

There also is strong evidence that corporations use accounting mechanisms

to shift profits from where they are actually earned to tax havens and other low-tax jurisdictions. Table 3

shows profits of U.S. corporations reported in select, small countries with very low tax rates. In a number

of cases, the amount of profits far exceeds the country’s actual output, suggesting the degree to which

companies use these countries to shelter profits that were quite obviously earned elsewhere. In 2010, for

example, subsidiaries of U.S. companies (“controlled foreign corporations”) reported profits in the

Cayman Islands totaling more than 20 times that country’s entire economic output. Even in the

Netherlands, which has a much larger economy, U.S. controlled foreign corporation profits amounted to

17 percent of GDP. It is implausible that the high concentration of U.S. profits for the countries shown in

Table 3 reflects the actual business activity of these firms rather than tax planning.

The U.S. tax system also provides incentives and opportunities for corporations to reduce their tax

burdens by relocating their tax residence to a lower-tax country through a corporate inversion. A

corporate inversion is a transaction in which a U.S.-based multinational firm merges with a foreign

corporation and the U.S. parent of the group is replaced by the foreign corporation, typically located in a

low-tax country. These transactions can substantially reduce the U.S. tax liability of the multinational

group with only minimal changes to its operation. There is nothing illegal about corporate inversions, but

these transactions point to a basic unfairness where corporations take advantage of the many benefits of

operating in the United States—including reliable rule of law, intellectual property protection,

government support for basic research, an educated workforce, and publicly-provided infrastructure—

and then avoid paying their fair share of taxes.

One reason corporations pursue inversions is to remove the earnings of their foreign subsidiaries from

the U.S. tax base. But another key incentive for inverting is to allow the corporation to reduce the taxes it

pays on its domestic (U.S. source) income through base erosion (or income shifting) techniques such as

earnings stripping and aggressive transfer pricing. For example, one common way for an inverted (or

foreign-parented) corporation to move, or “strip” earnings from the U.S. corporate tax base to a low- tax

10

See, e.g., Rosanne Altshuler and Harry Grubert. “Taxpayer Responses to Competitive Tax Policies and Tax Policy

Responses to Competitive Taxpayers: Recent Evidence.” 2004. Tax Notes Int’l: Special Reports; Harry Grubert and

John Mutti. “Taxes, Tariffs and Transfer Pricing in Multinational Corporation Decision Making.” 1991. 73 Rev. Econ.

And Stats. 285.

Country

Profits of U.S. Controlled Foreign

Corporations as a Share of GDP

Bahamas 71%

Bermuda 1,614%

British Virgin Islands 1,804%

Cayman Islands 2,066%

Cyprus 14%

Ireland 42%

Luxembourg 127%

Netherlands 17%

Source: Jane G. Gravelle, Cong. Res. Service, Tax Havens International Tax Avoidance and Evasion (2015).

Table 3: U.S. Controlled Foreign Company Profits Relative to GDP, 2010

14

jurisdiction, is for the company to borrow from a related foreign company in the low-tax jurisdiction, and

pay interest that is tax deductible in the United States. Earnings stripping not only reduces corporate tax

revenues, it also imposes competitive disadvantages on purely domestic U.S. firms and multinational firms

that have maintained their U.S. residence.

In the last major tax reform in 1986, the United States cut its corporate rate to well below average for

the advanced economies that comprise the Organization for Economic Cooperation and Development

(OECD). Other countries followed suit by reducing their statutory corporate rates to the point where the

U.S. statutory rate is now 11.5 percentage points above the OECD average (see Figure 6). The reduction

in tax rates abroad has increased the incentive to shift income offshore. At the same time, the United

States has failed to adequately protect its tax base by curbing income shifting and inversions directly.

The empirical evidence suggests that income-shifting behavior by multinational corporations is a

significant and growing concern that should be addressed through tax reform.

11

The pre-tax profitability

of controlled foreign corporations is negatively correlated with local country statutory tax rates, taking

into account real economic factors such as financial structure, capital employed, and other non-transfer

pricing operational aspects of multinational groups.

12

In addition to the evidence that companies

generally shift income from high-tax foreign countries to low-tax foreign countries, there also is evidence

11

See, e.g., Eric J. Bartelsman and Roel M.W.J. Beetsma. “Why Pay More? Corporate Tax Avoidance Through

Transfer Pricing in OECD Countries.” 2003. 87 J. Pub. Econ. 2225; Edward D. Kleinbard. “Stateless Income.” 2011.

65 Tax Law Rev. 99.

12

See, e.g., review of the literature, Department of the Treasury. “Ch. III: Study of Transfer Pricing.” November

2007. Report to the Congress on Earnings Stripping, Transfer Pricing and U.S. Income Tax Treaties.

https://www.treasury.gov/resource-center/tax-policy/Documents/ajca2007.pdf

; Jane Gravelle. “Tax Havens:

International Tax Avoidance and Evasion” 2009. 62 Nat’l Tax J. 727.

15

of income shifting specifically from the United States to other countries.

13

Income shifting from the

United States to other countries significantly erodes the U.S. tax base and leads to lower corporate tax

receipts, draining as much as $100 billion in corporate revenue from the United States every year,

according to one analysis.

14

Evidence suggests that high statutory tax rates also may affect a company’s

willingness to locate in the United States following mergers and acquisitions.

15

13

Harry Grubert. “Foreign Taxes and the Growing Share of Multinational Company Income Abroad: Profits, Not

Sales, Are Being Globalized.” 2012. 65 Nat’l Tax J. 247.

14

Kimberly A. Clausing. “The Effect of Profit Shifting on the Corporate Tax Base in the United States and Beyond.”

2016. Tax Notes. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2685442

15

Harry P. Huizinga and Johannes Voget. “International Taxation and the Direction and Volume of Cross Border

M&A.” 2009. 64 J. Fin. 1217.

C

ORPORATE

I

NVERSIONS

An extreme way for a U.S.-based multinational to shift profits out of the U.S. tax base is for the

company to change its tax residence from the United States to another country by merging with a

foreign firm in a transaction called an inversion. Over the past several years, a dramatic increase in

actual and announced inversions has raised concerns about their effects on the U.S. tax base and on

domestic business activity. While current law subjects inversions that appear to be based primarily on

tax considerations to certain adverse tax consequences, it has become clear from the growing pace of

these transactions that for many corporations, these consequences are acceptable in light of the

potential tax and financial reporting benefits.

Expatriating or inverting to a low-tax country offers two primary tax benefits for a U.S. multinational.

First, the corporation can reduce or eliminate any residual U.S. tax on foreign earnings—both taxes

owed on foreign earnings that are unrepatriated at the time of the merger and future foreign earnings.

Second, the transaction allows the inverted company to reduce its taxes on U.S. earnings by stripping

taxable income out of the United States. Inverted firms can strip earnings by claiming deductions in

the United States for interest paid to the new foreign parent. Inverted firms often increase their

reported book earnings because their computed worldwide effective tax rate is reduced by the

transaction.

Genuine cross-border mergers can make the U.S. economy stronger by enabling U.S. companies to

invest overseas and encouraging foreign investment to flow into the United States. But these

transactions should be driven by genuine business strategies and economic efficiencies, not simply by

a desire to avoid U.S. taxes.

There is nothing illegal about corporate inversions. However, the ability of a multinational corporation

to take advantage of the many benefits of locating in the United States and then refuse to pay its fair

share of taxes points to a basic unfairness in the tax system. That is why the President has called on

Congress to stop corporate inversions and proposed two major anti-inversion measures. The first

proposal limits the ability of U.S. firms to invert by providing that if a U.S. firm combines with a smaller

foreign firm, the merged entity will be treated as a U.S. entity for tax purposes. The second proposal

limits the ability of foreign-controlled companies to strip the U.S. corporate tax base using interest

and reinsurance payments, addressing a major financial incentive for U.S. firms to seek inversions

under current law.

16

Positive and Negative Externalities of Business Behavior

Business activity sometimes generates spillovers that benefit or harm other firms and the general public.

For example, one firm’s investment in basic research may lead to new discoveries that benefit not just

that firm but allow other businesses to develop new or better products as well. The beneficial effect of

one firm’s activities on another is an example of a positive externality. The private market may

underprovide research with spillover benefits because the firm paying for the research does not

incorporate the potential benefits to other firms when deciding how much research to invest in.

In fact, numerous studies find that the total returns to research and development are significantly larger

Though Congress has thus far failed to act, Treasury has used its existing authority under the tax

laws to reduce the tax benefits of—and when possible, stop—corporate tax inversions. Treasury’s

actions significantly diminish the ability of inverted companies to escape U.S. taxation. For some

companies considering mergers, inversions may no longer make economic sense.

To date, Treasury has taken action to:

• Prevent inverted companies from accessing a foreign subsidiary’s earnings while deferring

U.S. tax through the use of creative loans, which are known as “hopscotch” loans, and from

restructuring a foreign subsidiary in order to access the subsidiary’s earnings tax-free.

• Close a loophole to prevent inverted companies from transferring cash or property from a

foreign subsidiary to the new parent to completely avoid U.S. tax.

• Make it more difficult for U.S. entities to invert by strengthening the requirement that the

former owners of the U.S. entity own less than 80 percent of the new combined entity.

• Block a particularly blatant form of inversion known as a “third country” inversion, where

a U.S. firm merges with a firm based in one foreign country, but then locates its tax

residence in a third country—essentially cherry-picking the tax rules under which they

operate.

• Address “serial inverters” by ensuring that firms cannot avoid the existing anti-inversion

rules by acquiring foreign-owned corporate groups that themselves have grown larger

through inversions or acquisitions of U.S. firms.

• Limit the ability of firms to strip earnings out of the United States by treating certain

payments between related parties as non-deductible dividends instead of deductible

interest payments and otherwise strengthening the rules characterizing financial

instruments as debt or equity for tax purposes.

While these actions have helped slow the pace and reduce the tax benefits of inversions, only

Congress can put a stop to inversions. It can and should take action immediately. Ultimately, the

best way to address the more fundamental problems in our tax system that are highlighted by

inversions is through business tax reform that includes specific anti-inversion provisions. These

provisions will need to be in place even after business tax reform is enacted because there will

always be countries offering advantageous tax treatment where corporations can establish

residence for tax purposes if rules allow.

17

than the private returns earned by the investors who fund it.

16

This evidence suggests that the social

returns range from one to two times the private returns, a disparity which leads to private-sector

underinvestment in the absence of policies such as the Research and Experimentation (R&E) tax credit.

Studies that directly evaluate the R&E credit find that each dollar of foregone tax revenue through the

credit generally causes firms to invest at least one additional dollar in research and development.

17

Not all spillovers are positive, however. Pollution, such as carbon pollution and particulate pollution from

burning fossil fuels, imposes costs on society from climate change and impairments to health. Because

firms do not bear the consequences of those costs, they may rely too heavily on pollution-intensive

activities. Greenhouse gas emissions impose significant environmental costs, which will only continue to

grow for future generations.

18

Other pollutants, such as particulate matter and ozone, impose large

immediate social costs in the form of increased rates of mortality and morbidity, and reduced quality of

life.

19

Many social costs of pollution are not borne by the firms making the decisions to invest in polluting

activities, so firms may overinvest in those activities.

Well-designed tax policies can encourage greater investments in activities with positive spillovers, like

research, and reduce reliance on pollution-intensive fuel sources.

II. The President’s Framework for Business Tax Reform

The President’s approach to business tax reform is intended to reduce the tax-induced distortions across

industries, assets, means of financing, and different forms of business, and to address problems in our

international tax system. These reforms are intended to encourage domestic investment and increase the

productivity of those investments, to simplify the tax code for America’s small businesses, to encourage

certain business activities with clear external benefits, like clean energy and research, and to rationalize

the tax treatment of multinational corporations—all in a way that is fiscally responsible over the short and

long run.

Eliminate Loopholes and Subsidies, Broaden the Base, and Cut the Corporate

Tax Rate

The President’s Framework would eliminate dozens of different tax expenditures and fundamentally

reform the business tax base to reduce distortions that hurt productivity and growth. It would reinvest

16

Bronwyn H. Hall, Jacques Mairesse, and Pierre Mohnen. “Measuring the Returns to R&D.” 2010. Handbook of

the Economics of Innovation 2.; Laura Tyson and Greg Linden. “The Corporate R&D Tax Credit and U.S. Innovation

and Competitiveness: Gauging the Economic and Fiscal Effectiveness of the Credit.” 2012. Center for American

Progress.

17

Bronwyn H. Hall. “Effectiveness of Research and Experimentation Tax Credits: Critical Literature Review and

Research Design.” 1995. Report for the Office of Technology Assessment, Congress of the United States.; Bronwyn

H. Hall and John Van Reenen. “How Effective are Fiscal Incentives for R&D? A Review of the Evidence.” 2000. 29

Research Policy.

18

U.S. Environmental Protection Agency (EPA). “Summary of Key Findings.” 2015. Climate Change in the United

States: Benefits of Global Action.

19

World Health Organization (WHO). “Fact Sheet No. 313: Ambient (outdoor) air quality and health.” 2014.

18

the savings in reducing the maximum corporate tax rate from 35 percent to 28 percent and eliminating

the corporate alternative minimum tax. This combination of a broader base and a lower corporate rate

would alleviate the significant economic distortions identified above that cause businesses to base

investment decisions on tax rules rather than economic returns, and it would lead to greater parity

between large corporations and their large non-corporate counterparts. Furthermore, in conjunction with

the Framework’s proposal to modernize the international tax system and implement a minimum tax on

foreign earnings, the lower U.S. corporate rate would encourage greater investment here at home and

reduce incentives for U.S. companies to move their operations abroad or to shift profits to lower-tax

jurisdictions. Where appropriate, the changes could allow adequate transition periods to permit affected

parties to adjust to the new permanent tax rules.

The Framework would pay for cutting the corporate tax rate to 28 percent and for the business tax cuts

that were recently enacted by reforming U.S. international system and by broadening the tax base in three

major ways, including:

• Addressing depreciation schedules. Current depreciation schedules generally overstate the true

economic depreciation of assets. Although this provides an incentive to invest, it comes at the

cost of higher tax rates to raise a given amount of revenue. In an increasingly global economy,

accelerated depreciation may be a less effective way to increase investment and job creation

than reinvesting the savings from moving towards economic depreciation into reducing tax rates.

Several prominent tax reform proposals have proposed to scale back accelerated depreciation to

offset rate reductions, including the tax reform proposals put forward by Chairmen Camp and

Baucus. Other large countries have taken a similar approach: paying for rate-lowering corporate

tax reform at least in part by scaling back depreciation allowances.

20

Tax reform also is an

opportunity to rationalize the relative lengths of depreciation schedules so that they better align

with the economic lives of assets; in so doing, tax reform would reduce tax distortions that lead

to misallocation of capital across assets and industries.

• Reducing the bias toward debt financing. A lower corporate tax rate by itself would reduce but

not eliminate the bias toward debt financing. Reform should take additional steps to reduce the

tax preference for debt-financed investment, such as by “haircutting” corporate interest

deductions by a certain percentage. A tax system that is more neutral towards debt and equity

will reduce incentives to overleverage and produce more stable corporate finances, making the

economy more resilient in times of stress. In addition, limiting interest deductibility would finance

lower tax rates and do more to encourage investment in the United States than many other ways

to pay for rate reductions.

• Eliminating dozens of business tax loopholes and tax expenditures. The Framework starts from

a presumption that we should eliminate all tax expenditures for specific industries, with a few

exceptions that are critical to broader growth or address certain externalities. In particular, the

Framework would:

o Eliminate “last in first out” accounting. Under the “last-in, first-out” (LIFO) method of

accounting for inventories, it is assumed that the cost of the items of inventory that are

20

Alan J. Auerbach, Michael P. Devereaux, and Helen Simpson. “Taxing Corporate Income.” 2008. The Mirrlees

Review: Reforming the Tax System for the 21

st

Century.

http://eml.berkeley.edu/~auerbach/taxing_corporate_income_march_II.pdf

19

sold is equal to the cost of the items of inventory that were most recently purchased or

produced. This assumption overstates the cost of goods sold and understates the value

of inventories. The Framework would end LIFO, bringing us in line with international

standards and simplifying the tax system.

o Eliminate oil and gas tax preferences. The tax code currently subsidizes oil and gas

production through tax expenditures that provide preferences for these industries over

others. The Framework would repeal more than a dozen tax preferences available for

fossil fuels.

o Reform treatment of insurance industry and products. The Framework would reform the

treatment of insurance companies and products to improve information reporting,

simplify tax treatment, and close loopholes, including one in which corporations shelter

income using life insurance contracts on their officers, directors, or employees.

o Reform the measurement and character of gains. The Framework would reform the

treatment of capital gains, including modifying rules for like-kind exchanges, which allow

investors in certain assets to avoid realizing a capital gain—and thus to defer payment of

tax—through a transaction structured as an exchange rather than a sale.

Ultimately, achieving a lower corporate tax rate and reducing special-interest provisions will require

eliminating a wide variety of business tax exclusions, subsidies, and deductions. The proposals above,

described in detail in the President’s Budget, represent the first step in that process.

21

21

Additional details for specified proposals can be found in: Department of the Treasury. “General Explanations of

the Administration’s Fiscal Year 2017 Revenue Proposals.” 2016.

https://www.treasury.gov/resource-center/tax-

policy/Documents/General-Explanations-FY2017.pdf

20

W

ALL

S

TREET

R

EFORM AND

T

AXATION OF THE

F

INANCIAL

S

ECTOR

In response to the 2008 financial crisis, the worst since the Great Depression, the Administration

achieved landmark reform of the Nation’s financial system in 2010 with enactment of the Dodd-Frank

Wall Street Reform and Consumer Protection Act. In the years since enactment, Federal agencies have

helped make home, auto, and short-term consumer loan terms fairer and easier to understand for

average consumers, improved transparency for investors in financial markets, and increased financial

firms’ planning for and resilience to future financial downturns. These actions are already curbing

excessive risk-taking, closing regulatory gaps, and making our financial system safer and more

resilient.

However, more work remains to be done as there is evidence that the financial sector represents a

large and growing share of the economy in a manner that may create obstacles to shared growth.*

Business tax reform can help address the downsides of an excessive financialization of the economy,

including through some of the specific measures proposed in the President’s Budget:

• Impose a financial fee: Excessive leverage undertaken by major financial firms was a significant

cause of the recent financial crisis and is an ongoing potential risk to macroeconomic stability.

The financial fee—a tax on large financial institutions based on the amount of their liabilities—

can help remedy this by reducing the incentive for large financial institutions to use excessive

leverage. The structure of this fee would be broadly consistent with the principles agreed to

by the G-20 leaders. The President’s proposal would take a direct action to combat the risk in

the financial sector and its implications on broader market volatility.

• Pay for doubling the budgets of key market regulators through increased transaction fees:

Expanding the budgets of the CFTC and SEC would allow them to improve monitoring of new

developments in the markets and to continue to fulfill their missions in increasingly complex

financial sectors. Fee funding the CFTC would shift the costs of regulatory services it provides

from the general taxpayer to the primary beneficiaries of the CFTC’s oversight, and fee rates

would be designed in a way that supports market access, liquidity, and the efficiency of the

Nation’s futures, options, and swaps markets. Additionally, increasing the transaction fees

that currently fund the SEC and imposing a similar fee to finance the CFTC would particularly

affect high-frequency traders, which could help reduce certain risks in the market.

• Close the carried interest loophole: Taxing “carried interest” as ordinary income rather than

tax-preferred capital gain would close a loophole for private equity and hedge fund managers.

In addition, increasing the tax rate on capital gains would reduce the tax benefit of the carried

interest loophole and any other strategy that involves converting income that would be taxed

at regular rates to income taxed at the lower rates on capital gains.

• Modernize taxation of certain financial products to prevent tax arbitrage: Modernizing the

taxation of financial products by taxing derivatives on a “mark-to-market” basis with gain or

loss treated as ordinary income would reduce the ability of financial institutions and

sophisticated taxpayers to craft financial products to arbitrage the disparate tax rules for

financial products.

* See, e.g., Robin Greenwood and David Scharfstein. "The Growth of Finance." 2013. 27 J. Econ. Perspect. 3; Luigi Zingales.

"Does Finance Benefit Society?" 2015. 70. J. Fin. 1327.

21

Strengthen American Innovation, Clean Energy, and Manufacturing

As noted above, a well-designed tax system can help address positive and negative spillovers of business

behavior by encouraging those activities that provide broader benefits and discouraging activities that

cause harm. The President’s Framework identifies three areas where targeted incentives are appropriate:

research and development, clean energy, and manufacturing.

To encourage greater innovation, make sustainable investments in clean energy and promote

manufacturing, the President’s Framework would:

• Expand and simplify the R&E credit. While the recent permanent extension of the R&E credit

provides certainty for businesses investing in innovation and appropriately recognizes the

positive spillovers research activity generates, further reforms should be made to make the credit

even more effective. Currently, businesses must choose between two different credit formulas,

including one so outdated that it takes into account the amount of a business’s research expenses

from 1984 to 1988. The President’s Framework would simplify the credit by repealing the

outdated formula, increase the credit rate from 14 to 18 percent, and enhance the credit for

pass-through businesses.

• Consolidate, enhance, and permanently extend key tax incentives to encourage investment

in clean energy while repealing fossil fuel subsidies. The President’s Framework would make

permanent the tax credits for the production of renewable electricity and investment in

renewable energy technologies. These reforms would provide a strong, consistent incentive to

encourage investments in renewable energy sources, like wind and solar. The production tax

credit and investment tax credit for renewable electricity generation were recently extended

for five years, but permanent tax incentives for clean energy investment are needed to meet

the challenge of climate change and address the harmful consequences of pollution. In

addition, the structure of the renewable production tax credit has required many firms to invest

in inefficient tax planning through tax equity structures so that they can benefit even when

they do not have tax liability in a given year because of a lack of taxable income. The President’s

Framework would eliminate the need for these strategies by making the production tax credit

refundable. In addition to these reforms to support clean energy, the President’s Framework

would eliminate tax subsidies for oil and gas as described above.

• Effectively cut the top corporate tax rate on manufacturing income to 25 percent by reforming

the domestic production activities deduction. The manufacturing sector plays an outsized role

in the U.S. economy and is particularly important for future job creation, innovation, and

economic growth.

22

For this reason, the President’s Framework would reform the current

domestic production activities deduction. It would focus the deduction more on manufacturing

activity and expand the deduction to 10.7 percent, effectively cutting the top corporate tax rate

for manufacturing income to 25 percent.

22

For a review of the U.S. manufacturing sector, see generally: Department of Commerce. “The Competitiveness

and Innovation Capacity of the United States.” 2012.; President’s Council of Advisors on Science and Technology.

“Ensuring American Leadership in Advanced Manufacturing.” 2011.; P. Gary Pisano and Willy C. Shih. “Restoring

American Competitiveness.” 2009. Harvard Business Review.; Erica Fuchs and Randolph Kirchain. “Design for

Location? The Impact of Manufacturing Off-Shore on Technology Competitiveness in the Optoelectronics

Industry.” 2010. 56 Mgmt. Science 2323.; Michael Greenstone et al. “Identifying Agglomeration Spillovers:

Evidence from Winners and Losers of Large Plant Openings.” 2010. 118 J. Pol. Econ. 536.

22

I

NNOVATION

B

OXES

An innovation box is a special tax preference that applies a separate, lower, tax rate to income derived

from patents and other types of intangible business property, such as copyrights, trademarks, trade

secrets, and other forms of intellectual property (IP). Innovation boxes and related regimes in other

countries vary in their tax rate, in the types of eligible IP, in the scope of qualifying income, and the

treatment of IP-related expenses.

Advocates of an innovation box in the United States argue that applying a low tax rate to income

associated with intellectual property provides an incentive for investments in research and innovation,

can improve the international competitiveness of businesses that rely on IP by reducing their taxes,

and can address concerns about the erosion of the U.S. tax base to lower-tax jurisdictions by

encouraging firms to locate their IP in the U.S. for tax purposes.

Measured by the criteria of economic efficiency, the innovation box comes up short as a desirable tax

policy tool. Compared to the R&E credit, an innovation box is less effective in encouraging innovation.

The R&E credit provides benefits to firms undertaking new research which results in spillovers that

enhance the productivity of businesses and workers economy-wide (including research that is difficult

to commercially exploit). The evidence of the R&E credit’s success is why the Administration

supported permanent extension and continues to propose further enhancements.

By contrast, a U.S. innovation box would be costly and offer little potential to improve the overall

domestic economy. Unlike the R&E credit, an innovation box has much less “bang for the buck”

because it would provide windfall tax benefits for IP already in existence. In the United Kingdom, the

introduction of a low-tax patent box reduced corporate tax revenues, even when companies reported

more innovation-related income.* In the United States, the revenue costs of a similar tax incentive

are likely to be especially large because of the disproportionately large share of innovation-related

income U.S. multinationals earn from currently-taxed foreign royalty payments and the much larger

domestic market. In essence, an innovation box is just another variation on a “race to the bottom” in

the taxation of multinational firms, where countries compete to have the lowest tax rate on certain

corporate activities, without concern for the funding of necessary public goods and services.

Innovation boxes also work against the broadly shared goal of simplifying the tax system. New tax

rules and compliance checks would be needed to determine precisely how much income was

associated with particular innovations. For instance, it would be difficult to determine how much of a

drug company’s income is due to investment in developing a patented drug versus investment in the

manufacturing plant itself or in advertising and marketing activities. Corporations would have strong

incentives to attribute as much income as possible to the tax-favored innovation to take advantage of

preferential tax rates. These difficulties would lead to disputes between the IRS and taxpayers,

resulting in increased hiring of lawyers and accountants instead of increased innovative activity.

The President’s Framework, which provides support for innovation more efficiently through the R&E

credit and which tackles the problems within our international tax system with a reform centered on

the minimum tax, provides a better approach to addressing these challenges.

* Rachel Griffith, Helen Miller, and Martin O'Connell. “Ownership of intellectual property and corporate taxation.” 2014. 112

J. Pub. Econ. 12.

23

Strengthen the International Tax System to Encourage Domestic Investment

International reform should improve on the current broken and inefficient system under which firms must

pay tax at the full U.S. tax rate but only when profits are repatriated. There is considerable debate as to

how to reform the international tax code. One approach is to switch to a pure territorial system under

which all active foreign income would be subject to zero or nominal U.S. tax. However, a pure territorial

system could aggravate, rather than ameliorate, many of the problems in the current tax code. If foreign

earnings of U.S. multinational corporations are not taxed at all, firms would have even greater incentive

to locate operations abroad. Furthermore, corporations would have greater incentive to use accounting

mechanisms to shift profits out of the United States. And the incentives for corporations to invert to low-

tax jurisdictions in order to reduce their U.S. tax burdens through earnings stripping would remain.

Alternative reform proposals to address the problem of profit shifting by providing a costly tax preference

through an “innovation box,” as described above, would only exacerbate the race to the bottom in

international tax rates.

Tax reform must balance the need to reduce tax incentives to locate overseas with the need for U.S.

companies to be able to compete overseas for the investments and operations absolutely necessary to

serve and expand into foreign markets in ways that benefit U.S. jobs and economic growth. This will be a

difficult and complex undertaking but one that should be guided by the criteria of what system best

promotes the jobs, growth, and standard of living of American workers and their families.

In 2015, as part of the Budget, the President released a detailed international tax plan built on the reform

principles expressed in the Framework for Business Tax Reform. The President’s plan, which is centered

around a new per-country minimum tax on foreign earnings, would improve on the current system in

three broad ways:

• Reducing firms’ ability to avoid the U.S. tax system by shifting profits overseas. The minimum

tax on foreign earnings would ensure that no matter what tax planning techniques a U.S. firm

engages in, and no matter where it reports its profits, it would still face a tax rate of at least 19

percent. Unlike the current system, there would be no “deferral” of tax—the minimum tax would

apply to profits in the year they are earned. The minimum tax would stop our tax system from

generously rewarding companies for moving profits offshore. In addition, other elements of the

plan would make it harder to shift profits overseas by limiting interest stripping, transfer pricing

abuses, and inversions.

• Reducing the incentive to shift production overseas. The current system encourages firms to

shift production overseas to take advantage of indefinite tax deferral on the resulting earnings—

and to establish a legal toehold in a foreign country to enable even more earnings to be shifted

there on paper. The minimum tax would also reduce these incentives by ensuring that the

earnings of U.S. multinationals’ foreign subsidiaries are taxed on a current basis at a rate of at

least 19 percent.

• Increasing the global competitiveness of U.S. corporations. American multinationals often have

legitimate non-tax reasons to locate production overseas, either to serve local markets or

because of specific competitive advantages to overseas production. Other countries with

territorial systems effectively do not tax firms on their overseas production, and so those firms

incur no taxes when earnings are distributed to the parent company in its home country (that is,

upon “repatriation”). In addition, foreign resident companies that produce locally face only that

24

country’s corporate tax rate. In contrast, U.S. companies face relative high explicit or implicit

repatriation taxes, and therefore may operate at a tax disadvantage. In order to balance the two

goals above with the desire not to disadvantage American multinationals vis-à-vis their

competitors, the plan sets the global minimum tax rate lower than the full 28 percent rate

proposed for reform—and offers a deduction for income from active business investment.

Specifically, to achieve these objectives, the President’s plan would:

Institute a 19 percent minimum tax on foreign earnings

Foreign earnings would be subject to current U.S. taxation at a rate of 19 percent less a foreign tax credit

equal to 85 percent of the per-country average foreign effective tax rate. The minimum tax would be

imposed on foreign earnings regardless of whether they are repatriated to the United States, and all

foreign earnings could be repatriated without further U.S. tax. Thus, under the proposal, all active earnings

of foreign subsidiaries of U.S. firms (controlled foreign corporations, or CFCs) would be subject to U.S. tax

either immediately or not at all. Passive or highly mobile income such as dividends, interest, rents, and

royalties would continue to be subject to full U.S. tax on a current basis under the existing “Subpart F”

rules.

To help maintain international competitiveness, the minimum tax base would be reduced by an allowance

for corporate equity (ACE). The ACE allowance would provide a risk-free return on equity of the CFC

invested in active assets. In effect, this would allow U.S. based firms to exclude from tax all costs

associated with foreign investments—including the cost of equity financing—providing an even playing

field for U.S. firms operating abroad relative to their foreign competitors. At the same time, however, it

would ensure that companies cannot avoid U.S. tax on excess profits, such as those shifted abroad.

Foreign source royalty and interest payments received by U.S. persons would continue to be taxed at the

full U.S. statutory rate but, in contrast with current law, could not be shielded by excess foreign tax credits

associated with dividends. Foreign branches would be treated like CFCs. Interest expense incurred by a

U.S. person that is allocated and apportioned to foreign earnings on which the minimum tax is paid would

be deductible at the applicable minimum tax rate on those earnings. No deduction would be permitted

for interest expense allocated and apportioned to foreign earnings for which no U.S. income tax is paid.

Impose a one-time tax on unrepatriated earnings

Because the global minimum tax eliminates taxes on the repatriation of earnings, some adjustment must

be made to account for the large stock of unrepatriated earnings on which no U.S. tax has been paid. One

approach would separately track that stock of earnings, and tax it upon repatriation. That approach,

however, would be administratively burdensome, inequitable by treating firms differently depending on

their repatriation history, and overly generous by allowing continued deferral plus a lower corporate tax

rate.

Consequently, the President’s plan would impose a mandatory one-time tax on CFCs’ previously untaxed

earnings at a reduced rate of 14 percent. A proportional credit would be allowed for the amount of foreign

taxes associated with such earnings. The accumulated income subject to the one-time tax could then be

repatriated without any further U.S. tax. The revenue from the one-time tax is dedicated primarily to

funding transportation infrastructure investment.

25

Restricting deductions for excessive interest to curb “earnings stripping”

Claiming deductions for interest is a common technique used by multinational firms to erode the U.S. tax

base. Under current law, foreign multinational groups are able to load up their U.S. operations with

related-party debt and use the interest deductions to shift up to half of their U.S. earnings to low-tax

jurisdictions. This ability gives foreign multinationals a competitive advantage over purely domestic firms,

which have to pay U.S. tax on all of their earnings from U.S. operations. The proposal would address over-

leveraging of a foreign-parented group’s U.S. operations relative to the rest of the group’s operations by

limiting U.S. interest expense deductions to the U.S. subgroup’s interest income plus the U.S. subgroup’s

proportionate share of the group’s net interest expense.

Limit inversions

The President’s plan would limit inversions by preventing firms from acquiring smaller foreign firms and

changing their tax residence as a result. In addition, the proposal would prevent firms from changing their

tax residence to any country where they do not have substantial economic activities if their operations in

the United States are more valuable than their operations in the other country and they continue to be

managed and controlled in the United States.

Close loopholes and stop strategies that facilitate base erosion and profit shifting

While the minimum tax and the reduction in the corporate rate would reduce the incentives for erosion

of the U.S. base by domestic firms, the difference in tax rates would still provide a tax advantage for firms

able to shift profits to their foreign affiliates. And more importantly, foreign-owned and inverted

corporations would still have strong incentives to strip earnings out of the United States to low-tax

jurisdictions. Hence, additional reforms are necessary to reduce incentives to shift income and assets

overseas. Therefore, the President’s plan tightens rules governing cross-border transfers of intangible

property and closes loopholes by expanding the scope of the existing “Subpart F” rules. It restricts the use

of “hybrid” arrangements that take advantage of differences in tax rules to generate so-called “stateless

income”—income that is not subject to tax in any country.

These proposed reforms to the U.S. international system are consistent with the cooperative efforts of

the United States and other countries to establish principles for addressing the shared challenge of base

erosion and profit shifting by multinational firms. At the June 2012 G-20 Summit, the leaders of the world’s

largest economies identified the actions of multinational companies to reduce their tax liabilities by

shifting income into low- and no-tax jurisdictions as a significant global concern. The leaders instructed

their governments to develop an action plan to address these issues. The resulting action plan to address

base erosion and profit shifting (BEPS) was endorsed by President Obama and other world leaders at the

2015 G-20 Summit. The BEPS project made a number of recommendations and the OECD and G20

countries have committed to minimum standards in the areas of: requiring country-by-country reporting

of income, assets, employees, and taxes paid; fighting harmful tax practices; improving dispute resolution;

and preventing “treaty shopping.” In the area of transfer pricing (where concerns about profit shifting

were prevalent), existing international standards have been updated and strengthened. With respect to

recommendations on hybrid securities (treated as debt in some jurisdictions and as equity in others) and

on rules governing interest deductibility, countries have agreed on the general tax policy direction

reflected in the Administration’s proposals, which would require Congressional action in the United

States. The BEPS project also generated guidance based on best practices that focus on the areas of

disclosure and “CFC” rules (rules for taxing mobile income of foreign subsidiaries). Finally, participants

26

agreed to draft a multilateral instrument that countries may use to implement the BEPS work on tax treaty

issues. All these steps have established principles for appropriate taxation of multinational firms and have

set the stage for the OECD and G-20 countries to implement these approaches in their own tax systems.

Simplify and Cut Taxes for America’s Small Businesses

America’s small businesses face a tax code that is unduly complex. Often, these firms, unlike large

businesses, are not engaged in complex transactions, and yet they must spend significant time and

resources trying to comply with the tax code. Small businesses are disproportionately burdened with tax

compliance, and the cost of this burden is substantial.

In 2004, small businesses devoted between 1.7 and 1.8 billion hours and spent between $15 and $16

billion on tax compliance. On average, each small business devoted about 240 hours complying with the

tax code, and spent over $2,000 in tax compliance costs. An overwhelming share of the time burden is

due to recordkeeping, while most of the money burden is spent on compensation for paid tax preparers.

23

For some small businesses, the cost of tax compliance is particularly burdensome. In 2004, 9.7 percent of

small businesses spent over $5,000 in tax compliance and 11.2 percent devoted in excess of 500 hours to

compliance. Moreover, for very small businesses, the burden of tax compliance can approach the total

amount of taxes paid. For example, for small businesses with between $10,000 and $20,000 in annual

receipts, the money burden of compliance is between 6.8 and 7.8 percent of receipts while the time

burden amounts to about half—between 51.9 and 52.9 percent—of total receipts.

24

The high compliance cost for small businesses is a drag on innovation and entrepreneurship. Outlays for