1

Presentation of measures in

energy audits

- Example

EFFECT4buildings Toolbox:

Financial calculations; Annex 3

2

EFFECT4buildings project is implemented with the support from the EU funding Programme Interreg Baltic Sea

Region (European Regional Development Fund) and Norwegian national funding. The aim of the project is to

improve the capacity of public building managers in the Baltic Sea Region by providing them a comprehensive

decision-making support toolbox with a set of financial instruments to unlock the investments and lower the risks

of implementing energy efficiency measures in buildings owned by public stakeholders. More information:

http://www.effect4buildings.se/

Partners

The project “Effective Financing Tools for implementing Energy Efficiency in Buildings” (EFFECT4buildings)

develops in collaboration with public building managers a comprehensive decision-making support toolbox

with a set of financial instruments: Financial calculation tools; Bundling; Funding; Convincing decision

makers; Energy Performance Contract; Multi Service Contract; Green Lease Contract; Prosumerism. The

tools and instruments chosen by the project has the biggest potential to help building managers to

overcome financial barriers, based on nearly 40 interviews with the target group. The project improves

these tools through different real cases.

To make sure building managers invest in the best available solutions, more knowledge on different

possibilities is needed as well as confirmation from colleagues that the solutions performs well.

EFFECT4buildings mapped technological solutions for energy efficiency in buildings with the aim to share

knowledge and experiences of energy efficiency solutions among building managers in the Baltic Sea Region.

This document includes a new standard template for presenting proposal of measures based on conducted

energy audit. The template can be introduced and connect as a part of Total Concept Method process by

presenting the package of proposed measures with the TotalTool. Furthermore, the template can be utilized

in a comprehensive way as a separate excel sheet by including provided results to any calculation method

published in this toolbox. Optionally template will also provide advantage to any other appropriate energy

audit report and increase the implementation of energy efficiency measures.

3

Example of presentation of measures in

energy audits

Summary

The following report contains the result of an energy audit and proposals regarding how the

energy use and the energy costs can be decreased for XXXX.

XXXX is producing cement enclosures for fireplaces and stoves. The production plant, in this

report is located in XXXXX. XXXX also has another site, west of XXXXX. This site is treated in a

separate report.

At XXXX, elements of light versions of concrete is produced. The elements are used in fireplaces

and stoves to store heat. Another product is Marble which is cut into smaller pieces.

XXXX production site XXXX use electricity, natural gas and diesel as types of energy. During the

twelve months’ period from 2015-08-01 to 2016-07-31 the total energy use was 2 799 922

kWh and the total costs associated with energy use was € 138 306.

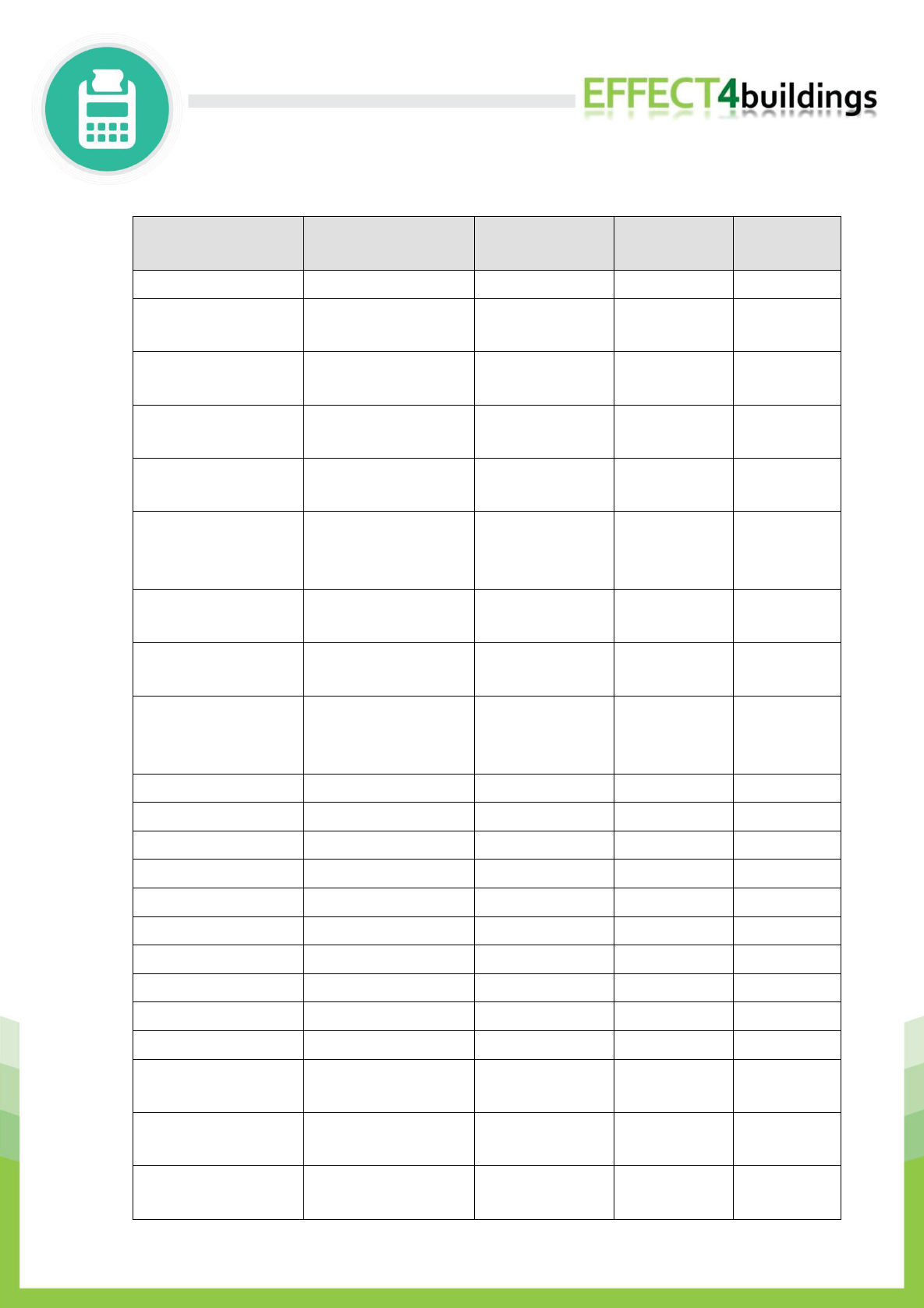

Table 1 shows a summary of the quantified measures in this report.

4

Process

Measure

Savings

Investment

cost [€]

Payback

time

[year]

Net

present

value

[€]

Internal

rate of

return

[kWh/year]

[€/year]

Building

Building 6: Apply an extra

insulated glass unit on

specified windows and

decrease the transmission

losses.

14 800

n.gas

550

4 000

7,3

1 000

11 %

Building

Building 7: Construct a well-

insulated wall that replaces

specified windows and

decrease the transmission

losses.

26 800

n.gas

990

7 200

7,3

3 000

12 %

Building

Building 7: Repair broken

window and decrease the

transmission losses.

3 500

n.gas

130

260

2,0

1 000

50 %

Building

Seal industrial doors in Building

2 and 7.

42 000

n.gas

1 550

500

0,3

10 000

310 %

Lighting

Converting from T8

fluorescent tubes to T5 in

production areas, building 3

and 12.

51 400

el

4 900

14 410

2,9

18 000

32 %

Lighting

Converting from T8

fluorescent tubes to LED tubes

and ECO/ES in specified

premises.

42 200

el

4 250

15 560

3,7

13 000

24 %

Ventilation

Sand blasting: equip fan motor

with a variable frequency

drive, VFD.

25 000

el

2 200

5 000

2,3

10 000

43 %

Compressed

air

Invest and install a compressor

with variable speed and use

this as the main compressor.

60 000

el

5 300

8 900

1,7

27 000

59 %

Compressed

air

Kaeser ASD 37 T: recover heat

to building 3 and fix current air

transportation.

1 500

el

70 000

n.gas

2 700

3 000

1,1

15 000

90 %

5

Compressed

air

Kaeser Airtower 19: recover

heat to building 12 and replace

filter more regularly.

14 000

n.gas

550

2 000

3,6

2 000

24 %

Production

Furnaces, building 12: Keep

gas-fired furnaces instead of

switching to electricity.

Recover heat from the

furnaces through a heat

exchanger, without

transferring CO

2

to premises

where people work.

Not quant.

----

Not quant.

----

----

----

Table 1: Shows a summary of the quantified measures in this report.

Table 22: Total concept method, by BELOK. Summary of the quantified measures in this report

presented with a graph to show return of investment. Y-axis showing yearly savings in SEK/year

and X-axel showing cost of energy investment in SEK.

6

Table of Contents

Summary 3

1 Introduction 7

1.1 Aim 7

1.2 Method 7

1.3 Boundaries 9

1.4 Assumptions 9

2 Description of the company 10

2.1 Contact details 10

2.2 Buildings 11

3 Energy statistics 15

3.1 Electricity 15

3.2 Natural gas 15

3.3 Diesel 17

4 Situation analysis and proposals 18

4.1 Lighting 20

4.2 Ventilation 23

4.3 Compressed air 24

4.4 Space heating and domestic hot water 28

4.5 Production 29

Appendices 30

Overview of site 30

Lighting survey 31

Calculations 34

Measurements 39

7

Introduction

Costs, related to energy are a major part of most manufacturing companies’ total costs. Due

to the fast growth of some large countries and the fact that it is becoming more difficult to

increase the oil production and also the extraction of other natural resources, the price of

many different types of energy has increased. It is therefore important for companies to start

working with questions regarding energy consumption and to manufacture in a way that is

energy efficient.

Another reason for reducing the energy consumption is the environmental problems that the

world is facing. Reduced energy consumption usually means a reduced environmental impact.

Aim

The aim is to perform an energy audit of the company’s energy use and to identify any

proposals for actions to reduce the energy costs. The audit is essential in order to find any

proposals for action and it also has an intrinsic value as it shows how the energy is distributed

among the various support- and production processes.

Method

The total energy consumption of the company has been studied. The energy statistics shows

how much electricity and thermal energy the company is using during a year and how the

energy use is distributed over time. Thereafter measurements have been performed and

different data have been collected in order to understand how the power and energy use is

distributed among different processes. The operation times have been obtained both by

measurements and by discussions with operating personnel.

Measuring instruments with data logging function, shown in Figure 1, measures the current

over time and then by using numerical integration the electrical power and the energy use can

be determined. The time duration of the measurements has been about a week so that both

the weekdays and the weekend are represented. Finally, the measurements have been

analysed in order to find proposals for action regarding possibilities to reduce the energy costs.

8

Figure 1: The picture to the left shows two installed measuring instruments with logging

function. The picture to the right shows the result of the measurement as a graph where the

power use is plotted against the time.

9

Boundaries

• For this energy audit, the production site XXXX premises and associated activities, are

used as boundaries. XXXX also has a production site on the other side of XXXX. This site

is treated in a separate report.

• To make the energy audits easier to read and understand all transports between the

production sites in XXXX and other external transports is included in this energy audit,

of the production site XXXX.

• This energy audit has been performed during the period XXXX.

• This report and the work performed in this energy audit, following these standards:

o EN 16247-1, General requirements

o EN 16247-3, Processes

o EN 16247-5, Competence of energy auditors

• In order to include all support and production processes, the measures are demarcated

to provide a good base for investment. The proposals should not be interpreted to be

anywhere close to technical design. In case that the calculations for the proposed

technical measures include design parameters, such as number of light fixtures in case

of alternative lighting or installed capacity for alternative heating sources, the used

numbers shall be considered as approximate numbers and the proposals be considered

as a part of a pre-design study. The reason that we show our calculations, in appendices,

are to clarify how the base for the proposed investment has been developed and also

as a tool for the company to check the credibility of the proposals. The calculations can

also be used in final evaluation of the proposals. We recommend the technical design

of the proposed measures to be made by an authorised design firm.

Assumptions

• In normal cases the measurements, although performed during normally just one week,

are assumed to be representative for the full year.

• The savings calculated for the proposed measures are not related to each other. It

means that the savings is presented as if just the single, current proposal was

implemented. This could be changed if many proposals, which interact with each other,

were implemented.

• The presented investment costs for the proposed measures are based upon

experiences from previous implementation at other industrial sites. In situations where

e.g. large pipe systems are proposed to be installed it may be difficult to correctly

predict the investment costs since the final design will determine quantities etc. In

order to make the final evaluation of the proposed measures the company is

recommended to request sharp offers from a number of potential suppliers.

• LCC calculations are based on a nominal interest rate of 10 % and a nominal annual

energy cost increase of 2 %.

10

Description of the company

XXXX is producing cement enclosures for fireplaces and stoves. The production plant, in this

report called XXXX, is located in XXXX. XXXX also has another site, west of XXXX. This site is

treated in a separate report.

At XXXX, elements of light versions of concrete is produced. The elements are used in fireplaces

and stoves to store heat. Another product is Marble which is cut into smaller pieces.

The support processes which consumes most energy is space heating, lighting and compressed

air. In the production the largest energy consumer is thermal treatment.

The number of employees at XXXX is 170. The normal working hours in production is 1 shift

between 06.00 am and 02.00 pm. Two of seven divisions are also working 2 and 3 shifts.

Sometimes there is production on Saturdays, which was the case during the week of

measurements.

The working hours at the office is between 08.00 am and 04.00 pm. The production is normally

closed for holidays during four weeks per year, of which two weeks are during the summer.

XXXX is certified in both ISO 9001 and ISO 14001 and is working with questions regarding

energy consumption. This report should be used as guideline of how the energy is used today

and how it could be used more effectively.

Contact details

Company:

Address:

Phone:

Contact person:

Phone:

Email:

Energy analyst: Peter Karlsson

Phone: +46 708281151

Energy analyst: Mattias Jonsson

Phone: +46 738406038

Energy analyst: Curt Björk

Phone: +46 737096008

11

Buildings

The site consists of several buildings as shown in Figure 4 in appendices. The total area of all

buildings is 13 400 m

2

of which the heated area is 11 100 m

2

.

Most buildings are used for production but there is also an office building and a building for

staff where dressing rooms and canteen is located. There are also several unheated tents.

The building envelopes vary but most of them have walls which are plastered and consists of

20 cm concrete with an insulating layer of 10 cm foam. The average U-values for ceilings and

walls of these buildings have been calculated to 0,34 W/m

2

K.

Some building envelopes have obvious defects and these building are the reason why the need

of heating is higher on XXXX compared to XXXX (see separate report). The key-value for heating

is 113 kWh/m

2

(based on period for energy statistics, see chapter 0) compared to 99 kWh/m

2

for XXXX. Measures for these buildings are given in the text below.

Roof, Building 6

During our visit we noticed that a crew of construction workers were in operation on the roof

of building 6, replacing/repairing the tar roof layer.

Unfortunately, nothing more was done; Building 6 has a building envelope that is in miserable

condition and annual heating costs must be soaring. It would therefore have been a golden

opportunity to add at least 10 cm of insulation on the existing roof at the time that the crew

worked on the roof. There would of course be an additional investment cost associated to the

insulation but it would be a marginal cost, adding some value in terms of energy savings instead

of only keeping the roof waterproof.

Our recommendation to the management is to evaluate this marginal investment the next time

that a bad roof will be repaired and the work crew is already in place. We can help you in

calculating the energy savings when such an evaluation will be done.

Measure, apply an extra insulated glass unit on the windows in Building 6.

Saving

Natural gas:

14 800

kWh/year

Cost reduction

550 €/year

Costs

Investment cost:

€ 4 000

Financial calculations

Payback:

7,3 years

LCC (cost saving 15 years):

€ 710

12

Apply an extra insulated glass unit on the windows in Building 6 and thereby reduce heat losses

through the windows.

A place built insulated glass unit means only about a quarter of the cost compared to the cost

of replacing the entire window. The unit is applied from the inside and therefore does not

affect the building’s appearance. The windows U-values are considered to be reduced from 6

W/m²K to 1,3 W/m²K.

In addition to energy savings the measure also reduces cold drafts in the winter and therefore

contributes to a better working environment.

Measure, construct a well-insulated wall that replaces the windows in Building 7.

One long side of Building 7 consists of two rows of windows

where the windows on the bottom row are insulated glazing (IG)

windows with an estimated U-value of 1,5 W/m

2

K. One of these

windows is broken and should be repaired immediately (see

measure below)

The windows on the upper row are old windows with only one

glass. These windows have an estimated U-value of 5 W/m

2

K and

are considered to be the part of the building which contributes

most to transmission losses, relative to size.

Construct a well-insulated wall that replaces

the one glass windows in Building 7 and

decrease the transmission losses.

The working environment is not expected to

get worse by replacing the windows,

because the IG windows will let daylight in.

It is considered possible to decrease the U-

value from 5 W/m²K to 0,3 W/m²K.

Measure, repair window in Building 7.

Saving

Natural gas:

26 800

kWh/year

Cost reduction

990 €/year

Costs

Investment cost:

€ 7 200

Financial calculations

Payback:

7,3 years

LCC (cost saving 20 years):

€ 2 520

Saving

Natural gas:

3 500 kWh/year

Cost reduction

130 €/year

Costs

Figure 2: Windows on building 7.

14

Measure, seal industrial doors in Buildings 2 and 7.

The industrial doors in Buildings 2 and 7 are

leaking in outside air and should be sealed.

In building 2, three doors are in bad shape

and can be seen in Figure 3

The savings is difficult to calculate but have

been estimated with standard value based

on the size of the area that is leaking.

Saving

Natural gas:

42 000

kWh/year

Cost reduction

1 550 €/year

Costs

Investment cost:

€ 500

Financial calculations

Payback:

0,3 years

LCC (cost saving 10 years):

€ 9 900

Figure 3: Shows industrial doors in Buildings 2 and 7

15

Energy statistics

This chapter presents all purchased energy and the costs associated with energy use broken

down by individual types of energy. All costs are excluding VAT.

XXXX’s production site XXXX use electricity, natural gas and diesel as types of energy. During

the twelve months’ period from 2015-08-01 to 2016-07-31 the total energy use was 2 799 922

kWh and the total costs associated with energy use was € 138 306.

Electricity

The total electricity use during the twelve months’ period from 2015-08-01 to 2016-07-31 was

686 710 kWh

1

according to Chart 1. The cost for electricity during the same period was €

58 522

2

.

The variable cost of electricity, i.e. the cost that depends on the electricity use, amounts to

0,088 €/kWh

3

. The cost depending on the electricity demand amounts to 28,9 €/kW and year

4

.

These are the costs that are used when the savings regarding energy use are calculated to

reduced energy costs, for proposed measures.

Chart 1: Shows the load curve for electricity during the twelve months’ period from 2015-08-01

to 2016-07-31.

Unit

Name

Avr

Min

Max

Energy [kWh]

kW

Power

78,18

0,00

247,60

686 710

Natural gas

16

1

XXXX.

2

XXXX.

3

XXXX.

4

XXXX.

17

The total consumption of natural gas during the twelve months’ period from 2015-08-01 to

2016-07-31 was 1 952 786 kWh

5

according to Chart 2. The cost for natural gas during the

same period was € 66 469

6

.

The variable cost of natural gas, i.e. the cost that depends on the use of gas, amounts to 0,037

€/kWh

7

. This is the costs that is used when the savings regarding energy use are calculated to

reduced energy costs, for proposed measures.

Chart 2: Shows the consumption of natural gas for each month during the twelve months’

period from 2015-08-01 to 2016-07-31.

Diesel

The total consumption of diesel during the twelve months’ period from 2015-08-01 to 2016-

07-31 was 160 426 kWh

8

. The cost for diesel during the same period was € 13 315

9

.

The variable cost of diesel, i.e. the cost that depends on the use of diesel, amounts to 0,083

€/kWh

10

. This is the cost that is used when the savings regarding energy use are calculated to

reduced energy costs, for proposed measures.

5

XXXX

6

XXXX

7

XXXX

8

XXXX

9

XXXX

10

XXXX

33508

52085

175517

230875

232916

339316

267761

274398

169715

84272

58851

33572

0

50000

100000

150000

200000

250000

300000

350000

400000

kWh

Natural Gas 2015/2016

18

Situation analysis and proposals

The following chapter describes how the energy is used at present and also presents proposals

on how energy can be used more efficiently. Chart 3 shows how electricity, natural gas and

diesel consumption is distributed among the various support and production processes, which

are described in more detail under the headings below.

Calculations on how the energy is used are based on:

- The performed measurements, shown in the appendices.

- The energy statistics during the twelve months’ period from 2015-08-01 to 2016-07-

31, described in chapter 0.

- The inventory of installed power and capacities.

- Observed operating patterns.

- Identified energy recovery.

19

Chart 3: Energy balance, shows how the energy use is distributed among the various support

and production processes.

20

Lighting

The lighting annually uses approximately 284 600 kWh

el

according to the lighting survey that

can be found in the appendices. The total installed power for the lighting is 96,7 kW.

The majority of all lighting consists of T8 fluorescent tubes 58W and 36W. In building 12 and 6

a few new LED fixtures that replaces the T8 fixtures can be find.

The general lighting is considered to provide a good working environment. The lux value varies

between 150 to 400 lx and is lowest in warehouses and highest in premises with work that

requires better lighting such as mounting.

As a KPI value (Key performance indicator) for lighting, installed power per square meter is

used. The key value does not include how strong the lighting is. I high KPI value can be

explained by great need of lighting. The lux value has therefore been measured.

In Table 3 the KPI and lux value is shown for chosen premises. All of these premises have T8

fluorescent as general lighting and the different in KPI-value is explained by difference in lux-

value and parameters specific for the premises such as ceiling height and colours of walls,

ceiling and floor.

Premises

Installed power [kW]

KPI-value [W/m

2

]

Lux [lx]

Building 2 - Marble

5,4

9,3

250

Building 3 - Fireplaces

22,2

7,9

160

Building 3 - Fireplaces

warehouse

6,8

5

200

Building 7

10,1

13,3

400

Building 10 - Slate 1

4,4

8,9

400

Building 10 - Slate 2

3,1

6,4

350

Building 11 - Warehouse

SL. TH

3,1

3,6

150

Building 12 - Thermotte

12,2

8,3

350

Table 3: Shows KPI value for chosen premises. An overview of buildings and premises are shown

in appendices in Figure 4. Lux values are an average value that represents the entire premises.

Higher and lower Lux value can appear in specific parts of the premises.

Measure, Converting from T8 fluorescent tubes to T5.

Saving

Electricity:

51 400

kWh/year

Cost reduction

4 900 €/year

Costs

Investment cost:

€ 14 410

Financial calculations

21

The premises with highest electricity use

during one year are the production area in

building 3 (fireplaces) and building 12

(Thermotte).

In these premises it is profitable to change from T8 fluorescent tubes. The lighting technology

that is considered to be most suitable is T5 fluorescent tubes with a higher light output per

Watt and a more efficient drive than T8 fluorescent tubes.

The reason that LED is not suggested in these premises is that it would be too high investment

compared to savings. LED tubes are not suggested because most existring fixtures are old and

need to be changed.

Measure, Converting from T8 fluorescent tubes to LED tubes.

Payback:

2,9 years

LCC (cost saving 10 years):

€ 18 470

Saving

Electricity:

42 200

kWh/year

Cost reduction

4 250 €/year

Costs

Investment cost:

€ 15 560

Financial calculations

Payback:

3,7 years

LCC (cost saving 10 years):

€ 12 960

22

In the other premises a combination between changing from T8 fluorescent tubes to LED-tubes

and ECO/ES tubes would be the best alternative. T5 tubes are not profitable here because of

too low run time and too low installed power for current lighting.

Current fixtures are old but are expected to last a few more years. LED technology is moving

forward fast and new fixtures for industrial premises will be cheaper and better in a few years

and therefore keeping current fixtures but changing light source is suggested.

For fixtures with least wear, LED tubes is the best alternative and for the other fixtures ECO/ES

tubes should be applied. Both of these lighting technologies are explained under headings

below. The calculations for these measures have been made with the assumption that half of

the current T8 fluorescent tubes are changed for LED tubes and the half for ECO/ES tubes.

In building 10 personnel are worried that changing light source would mean a cooler light. Both

LED tubes and ECO/ES are available as warmer light down to 3000 K, why this is not an

argument.

LED tubes

Converting from T8 fluorescent tubes to LED tubes which can be applied in existing fixtures

and therefore means a lower investment cost than most other alternatives.

The T8 58W (including drive means 68W) are exchanged for LED 25W (including drive means

30 W) and T8 36W (including drive means 43W) for LED 21W (including drive means 24W). The

power varies slightly between different providers.

LED tubes produce less light than T8 fluorescent tubes but directs all the lights downwards.

Therefore, LED tubes are suitable with existing fittings with poor reflectors that can´t take

advantage of the higher light output of the T8 fluorescent tubes. Before converting all the light

sources, a smaller number of LED tubes should be purchased to ensure that the lighting still

provide a good working environment.

The LED tubes have a higher life expectancy than T8 fluorescent tubes which means that the

tubes don’t have to be replaced so often. The maintenance cost is thereby reduced.

It is important to have a guarantee of at least 5 years because there are LED tubes of poor

quality on the market.

ECO tubes

The conventional T8 tubes used today, can be exchanged for the equivalent ECO/ES tubes that

use 10 % less energy. These tubes are called ECO by Philips and ES by Osram and can be applied

in existing fixtures (also other manufactures have the same type of fluorescent tubes).

ECO/ES tubes provide basically the same light output and last as long as current fluorescent

tubes. The investment cost is an additional cost compared with the conventional T8 tubes and

amounts to approximately € 3 each.

Because the payback time is shorter than the expected technical lifetime of the conventional

T8 tubes, and the LCC calculation gives a positive result, the measure is profitable.

23

Ventilation

Ventilation is using approximately 59 600 kWh

el

/year. Most of the buildings are not ventilated

and the majority of the energy consumption is used by the filter for sand blasting and polishing

(see measure below).

There is also a ventilation unit for building 7a with heat recovery that runs 1-shift.

Sand blasting

Our logging of the electricity use for sand blasting filter (ventilation fan, 18 kW) show that this

fan is in operation between 06.00 and 21.30 weekdays, with a 30 minute break in the morning

(09.30 – 10.00) when the fan is switched off. The base level for the fan is at 14,5 kW and when

actual operations are done the power demand increases to 17,6 kW. It seems that the main

part of the electric energy use here is for keeping the fan running, not necessarily transporting

anything out from sand blasting or/and polishing to the filter.

Measure, fan with variable frequency drive

We propose that the fan motor be equipped

with a variable frequency drive, VFD; that

can reduce the fan speed (motor frequency)

to 20 Hz when there are no operations going

on. In addition to this there should be

automatic dampers installed for every work

station/exhaust point so that there is no

suction when no work is being done (except

a small flow in order to keep the motor

running at 20 Hz). As one or more dampers

open there will be a change in duct pressure

and the fan can increase its speed via the VFD.

Calculating annual electric energy use for this fan gives us a number of 50,000 kWh/year. The

proposed modification/investment can easily reduce the annual electric energy use by 50 %,

or 25,000 kWh of electric energy per year, worth 2,200 Euros per year.

The investment cost is estimated to be approximately 5,000 Euros, giving a pay-off time of 2.3

years.

Saving

Electricity:

25 000

kWh/year

Cost reduction

2 200 €/year

Costs

Investment cost:

€ 5 000

Financial calculations

Payback:

2,3 years

LCC (cost saving 10 years):

€ 9 760

24

Compressed air

The compressed air system is using 134 000 kWh/year and is served by three compressors,

model Kaeser ASD 37 with rated power of 22 kW, Kaeser Airtower19 with rated power of 11

kW and Speiarke Lialter with rated power of 5,5 kW. Speiarke Lialter is only used if pressure is

too low in building 2a.

The average power use during one day of production is 20,5 kW. The air pressure in the system

is around 7.5 bar.

Because some divisions are working 2 and 3 shifts there is a need for compressed air from

Monday morning to Friday afternoon.

Measure, compressor with variable frequency drive

Invest and install a compressor with variable

speed and use this as the main compressor.

Keep Kaeser ASD 37 T as a reserve

compressor only used during stop for main

compressor.

The need for compressed air varies widely

during a production day. According to

measurements made by Kaeser, spring

2016, the airflow during peaks around 7 am

and 1 pm is above 5 m

3

/min. During the

third shift the airflow is only 0.6 m

3

/min.

The power consumption for compressors does not vary as much. The average power for

compressors during first shift (with peak loads) is 20,5 kW and during third shift 15,6 kW.

A compressor with variable frequency drive would much better adapt the production to the

need for compressed air and reduce the power consumption when the need is low.

Measure, Kaeser ASD 37 T, air transportation and heat recovery

Saving

Electricity:

60 000

kWh/year

Cost reduction

5 300 €/year

Costs

Investment cost:

€ 8 900

Financial calculations

Payback:

1,7 years

LCC (cost saving 10 years):

€ 26 660

Saving

Electricity:

1 500 kWh/year

Natural gas:

70 000

kWh/year

Cost reduction

2 700 €/year

Costs

Investment cost:

€ 3 000

Financial calculations

Payback:

1,1 years

LCC (cost saving 10 years):

€ 15 120

25

The air compressor located in the compressor room between buildings 2 and 3 at XXXX XXXX

site has a non-functioning heat recovery/cooling system that can be fixed so that two main

significant goals can be achieved:

The system, with a ventilation duct leading from outside into the compressor room, does not

have sufficient cooling capacity. Therefore, a split cooling unit, with 800 W electricity use and

2.2 kW cooling capacity is placed in the compressor room to help during warm days.

The system does not have appropriate exhaust capacity either. A hood on top of the

compressor is located too close to the top of the compressor and the exhaust air duct is

broken/separated up at ceiling level before the duct leaves the room and continues to the

environment (outdoors) or into the marble

grinding/polishing room. See photos:

This system must be re-constructed so that cooling air can be drawn from outside during the

summer and from the marble department (or from the cleaner part of Kominki, building 3) in

the winter and so that the exhaust can be evacuated to the outside during the summer and

back to where the air was taken from, during the winter. By fixing this the compressor can get

sufficient supply of fresh air and the warm air that is exhausted from the compressor can be

used to replace the use of natural gas for heating during the cold season. Parts of the existing

air distribution system can be used also in the future:

26

By fixing the system it is calculated that the extra

cooling unit does not have to be used anymore,

saving 1,500 kWh of electricity during the summer.

The energy recovered from the compressor during

the heating season can be used instead of natural

gas, saving a total of 60,000 kWh of natural gas

every winter, net savings. With an expected annual

efficiency of the gas boilers at 85 % the gross

natural gas savings amount to over 70,000 kWh per

year. Total savings, 1,500 kWh of electricity and

70,000 kWh of natural gas, are worth 2,700 Euros per year.

The investment cost is estimated to be around 3,000 Euros, making the pay-back time as short

as 1.1 years.

Measure, Kaeser Airtower 19, heat recovery and filter change

Saving

Natural gas:

14 000

kWh/year

Cost reduction

550 €/year

Costs

Investment cost:

€ 2 000

Financial calculations

Payback:

3,6 years

LCC (cost saving 10 years):

€ 1 690

27

This compressor is located in a small building located close to warehouse 11 and not far from

building no. 12. Measured data for this compressor shows that it annually uses approximately

22,500 kWh, every week approximately 430 kWh of electricity.

When visiting the compressor room, we noticed that the compressor’s air filters were very

dirty, see photo. This makes the compressor run very inefficiently since it cannot easily get the

air that it needs to generate the compressed air. It is like breathing through a straw, like having

asthma.

Our recommendation is that the air intake filters should be

replaced more regularly, maybe as often as once every month

if needed. This will increase the compressor efficiency

significantly although it is not easy to calculate the savings.

Also the heat that this compressor generates could be used to

heat buildings instead of only using natural gas for heating.

Since the compressor house is closest to warehouse 11 it

should be most natural to utilise the recovered compressor

heat in this warehouse. However, the warehouse already

utilises recovered heat from the sand blasting filter, located

outside building 10, why we recommend installation of a fan,

a manual damper to choose summer or winter operation and

an insulated duct leading the recovered heat into building 12

which is also close by the compressor house for compressor ASD 19.

The energy recovered from the compressor during the heating season can be used instead of

natural gas, saving a gross total of over 14,000 kWh of natural gas every winter, worth 550

Euros per year.

The investment cost is estimated to be around 2,000 Euros, making the pay-back time become

3.6 years.

28

Space heating and domestic hot water

Natural gas is used for space heating and domestic hot water. The heat is distributed through

a hydronic heating system with radiators and aerotempers. Smaller local systems also exist, for

example building 6 has its own gas burner. The amount of natural gas used for space heating

was 1 250 000 kWh and for domestic hot water 50 000 kWh during the twelve month period

from 2015-08-01 to 2016-07-31.

The KPI value for space heating amounts to 113 kWh/m

2

and year (based on the same twelve

months’ period) which doesn´t seems to be particularly high. However, if one takes into

account that most buildings are not ventilated and therefore do not have any ventilation losses

this KPI-value is higher than for a normal building with similar production.

The high KPI-value is explained by deficiencies in the building envelopes. Measures that

decrease the need for space heating are given in chapter 0, 0, 0 and 0.

The electricity for space heating and domestic hot water shown in Chart 3 is the energy used

by the main circulation pumps which annually amounts to 9 000 kWh

el

respective 2 000 kWh

el

.

29

Production

The processes in the production annually use 140 000 kWh

el

and 655 000kWh

n.ags

. Separate

measurement has been done for the water cutting machine. Other processes have been

estimated by measuring electricity centrals for different buildings. These measurements can

be found in appendices.

There is small idle power consumption during weekends and this is not derived from

production according to measurements. The idle power is as low as 10 kW and is believed to

be from circulation pumps for heating system and from outside lighting.

Furnaces, building 12

In building 12 there are some gas-fired furnaces that are used to cure some of the finished

products. The process is now in operation during night time and the temperature in the

furnaces vary between 80 and 120

o

C. According to the personnel it is not easy to maintain the

correct temperature (or even to know which is the correct temperature) in the furnaces

because it varies so much depending on how close to the openings the products are.

Before the furnaces were installed the products cured in room temperature but it took longer

time and of course this also requires larger space for storage of products while curing.

There also used to be a heat recovery system, using excess heat from the furnaces to heat

some of the premises (a warehouse) but that system is no longer in use due to problems with

CO

2

in the air (rest product from combustion of natural gas). When heat could be used also for

heating during the heating season, then at least the usage of natural gas had a doubled value.

Now it is questioned whether to continue to use gas-fired furnaces, to switch to electric

furnaces or to go back to getting the products cured in room temperature.

After evaluating the power situation, costs of various energy sources etc. we strongly

recommend that there should not be a change to electric furnaces; costs will be too high for

the electricity and there will also be some implications on the rate structure and the potential

power interruptions that follow with exceeding a demand of 300 kW.

From an energy efficiency point of view it is best to not use any furnaces at all but we realise

that productivity goals may call for some increased curing time. In case furnaces must be used

we recommend gas-fired furnaces but that some investments are made to recover heat from

the furnaces through a heat exchanger, without transferring CO

2

to premises where people

work.

30

Appendices

Overview of site

Figure 4: Overview of site XXXX with building numbers.

31

Lighting survey

32

Premises

Type

Installed power

[kW]

Run time

[h/year]

Energy use

[kWh/year]

Building 2 - Marble

T8 58W

5,4

2 160

11 800

Building 2a - Wood

department

T8 58W

3,3

2 160

7 100

Building 2 -

Compressor room

T8 36W

0,1

2 160

200

Building 2 - Electricity

central

T8 36W

0,1

2 160

200

Building 3 -

Fireplaces

T8 58W

22,2

2 880

63 800

Building 3 -

Fireplaces

warehouse

T8 58W, Metal halide

120W

6,8

2 880

19 500

Building 3a - World

warehouse

T8 58W

4,5

2 160

9 700

Object 4a - Tent

warehouse

T8 36W

0,5

2 880

1 500

Building 5 - Wood

T8 36W, High

pressure sodium

150W

1,1

2 160

2 400

Building 6

T8 58W

1,2

2 160

2 600

Tent warehouse "C"

T8 58W

1,5

2 160

3 200

Building 7

T8 58W, T8 36W

10,1

2 160

21 800

Building 7a - Foundry

T8 36W

2,1

2 160

4 600

Building 8 - Welding

T8 58W

2

2 160

4 400

Crusher

T8 58W

1

2 160

2 100

Office

T8 36W, T8 18W

2

2 400

4 900

Building 10 - Slate 1

T8 58W

4,4

2 400

10 400

Building 10 - Slate 2

T8 58W

3,1

2 400

7 500

Building 11 - Canteen

T8 58W

1,4

2 160

2 900

Building 11 - Dressing

room

T8 58W

2,9

2 160

6 200

Building 11 -

Corridors, Staircase

T5 28W

0,1

2 160

300

Building 11 -

Warehouse SL. TH

T8 58W, LED 102W

3,1

2 400

7 300

33

Building 12 -

Thermotte

T8 58W

12,2

5 760

70 500

Building 13 -

Laboratory

T8 58W, T8 18W

1,7

2 160

3 600

Outside

Metal halide 120W,

High pressure

sodium 150W, Hg

125W

4

4 000

16 100

Total

96,7

284 600

Table 4: Performed lighting survey. An overview of buildings and premises are shown in

appendices in Figure 4.

34

Calculations

Building

Seal the industrial door in Building 2 and 7.

Transmission losses have been estimated by standard value to 60 kWh / year and cm

2

. The

area of the field is measured to 700 cm

2

.

The investment cost used in the calculation is € 500.

The parameters for the LCC calculation is, calculation period 10 years, discount rate 10 % and

annual energy price increase 2 %.

Apply an extra insulated glass unit on the windows in Building 6.

U-value for the current window is estimated to 6 W/m²K. It is considered possible to reduce to

1,3 W/m²K with an extra insulated glass unit. The window area amounts to 36 m² and the

indoor temperature to 18°C.

The investment cost used in the calculation is € 4 000.

The parameters for the LCC calculation is, calculation period 15 years, discount rate 10 % and

annual energy price increase 2 %.

Construct a well-insulated wall that replaces the windows in Building 7.

U-value for the current window is estimated to 5 W/m

2

K. It is considered possible to reduce to

0,3 W/m

2

K. The window area amounts to 65 m

2

and the indoor temperature to 18°C.

35

The investment cost used in the calculation is € 7 200.

The parameters for the LCC calculation is, calculation period 20 years, discount rate 10 % and

annual energy price increase 2 %.

Repair broken window in Building 7.

U-value for the current window is estimated to 35 W/m²K. It is considered possible to reduce

to 1,3W/m²K. The window area amounts to 1,2 m² and the indoor temperature to 18°C.

The investment cost used in the calculation is € 260.

The parameters for the LCC calculation is, calculation period 20 years, discount rate 10 % and

annual energy price increase 2 %.

36

Lighting

Change of lighting to T5

The new lighting is calculated to provide an estimated key value. The change applies to the

room(s) Building 12 Thermotte, Building 3 Fireplaces.

The investment cost used in the calculation is € 14410.

The parameters for the LCC calculation is, calculation period 10 years, discount rate 10 % and

annual energy price increase 2 %.

Change of lighting to ECO/ES tubes

The following savings have been calculated for the measure: Electricity 42 200 kWh/year. The

reduced energy costs have been estimated at 4 250 €/year.

The investment cost used in the calculation is € 15 560.

The parameters for the LCC calculation is, calculation period 10 years, discount rate 10 % and

annual energy price increase 2 %.

Ventilation

Sand blasting, fan with variable frequency drive

The following savings have been calculated for the measure: Electricity 50 000 kWh/year. The

reduced energy costs have been estimated at 2 200 €/year.

The investment cost used in the calculation is € 5 000.

37

The parameters for the LCC calculation is, calculation period 10 years, discount rate 10 % and

annual energy price increase 2 %.

Compressed air

Compressor with variable frequency drive

The following savings have been calculated for the measure: Electricity 60 000 kWh/year. The

reduced energy costs have been estimated at 5 300 €/year.

The investment cost used in the calculation is € 8 900.

The parameters for the LCC calculation is, calculation period 10 years, discount rate 10 % and

annual energy price increase 2 %.

Kaeser ASD 37 T, air transportation and heat recovery

The following savings have been calculated for the measure: Electricity 1 500 kWh/year,

Natural gas 70 000 kWh/year. The reduced energy costs have been estimated at 2 700 €/year.

The investment cost used in the calculation is € 3 000.

The parameters for the LCC calculation is, calculation period 10 years, discount rate 10 % and

annual energy price increase 2 %.

Kaeser Airtower 19, heat recovery and filter change

The following savings have been calculated for the measure: Natural gas 14 000 kWh/year. The

reduced energy costs have been estimated at 550 €/year.

The investment cost used in the calculation is € 2 000.

The parameters for the LCC calculation is, calculation period 10 years, discount rate 10 % and

annual energy price increase 2 %.

38

39

Measurements

Measurement 1: Production, Water cutting.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

1,22

0,00

58,94

226

40

Measurement 2: Electricity central, Building 7.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

8,68

0,72

54,25

1 619

41

Measurement 3: Electricity central, Building 3.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

18,20

6,60

52,05

3 396

Measurement 4: Electricity central, Office.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

1,34

0,31

10,56

250

42

Measurement 5: Electricity central, Building 11, 3a, 12.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

31,28

1,44

89,84

5 835

43

Measurement 6: Electricity central, Building 6.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

2,78

0,00

54,63

519

44

Measurement 7: Electricity central, Building 2 (R5).

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

0,20

0,00

2,87

4

45

Measurement 8: Electricity central, Building 2 R1 R2 (1).

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

1,20

0,00

8,62

25

46

Measurement 9: Electricity central, Building 2 Polerka.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

0,00

0,00

0,00

0

47

Measurement 10: Electricity central, Building 2 R3.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

2,54

0,00

19,26

54

48

Measurement 11: Compressed air, Kaeser ASD37T.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

13,14

0,00

24,90

2 448

49

Measurement 12: Compressed air, Kaeser Airtower 19.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

2,72

0,00

13,80

506

50

Measurement 13: Electricity central, Building 2 R1 R2 (2).

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

3,50

0,00

22,74

73

51

Measurement 14: Ventilation, Building 7a.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

1,22

0,00

6,36

25

52

Measurement 15: Ventilation, Sand filter.

Unit

Name

Ave

Min

Max

Energy

(kWh)

[kW]

Power

8,23

0,00

17,68

170

Normal Text text text

Example of bullets

• Text

• Text’

• Text

•

53