Net Zero

by 2050

A Roadmap for the

Global Energy

Sector

Net Zero

by 2050

A Roadmap for the

Global Energy Sector

Net Zero by 2050 Interactive

iea.li/nzeroadmap

Net Zero by 2050 Data

iea.li/nzedata

IEA member

countries:

Australia

Austria

Belgium

Canada

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Japan

Korea

Luxembourg

Mexico

Netherlands

New Zealand

Norway

Poland

Portugal

Slovak Republic

Spain

Sweden

Switzerland

Turkey

United Kingdom

United States

The European

Commission also

participates in the

work of the IEA

IEA association

countries:

Brazil

China

India

Indonesia

Morocco

Singapore

South Africa

Thailand

INTERNATIONAL ENERGY

AGENCY

The IEA examines the

full spectrum

of energy issues

including oil, gas and

coal supply and

demand, renewable

energy technologies,

electricity markets,

energy efficiency,

access to energy,

demand side

management and

much more. Through

its work, the IEA

advocates policies

that will enhance the

reliability, affordability

and sustainability of

energy in its

30 member

countries,

8 association

countries and

beyond.

Please note that this

publication is subject to

specific restrictions that limit

its use and distribution. The

terms and conditions are

available online at

www.iea.org/t&c/

This publication and any

map included herein are

without prejudice to the

status of or sovereignty over

any territory, to the

delimitation of international

frontiers and boundaries and

to the name of any territory,

city or area.

Source: IEA. All rights

reserved.

International Energy Agency

Website: www.iea.org

Revised version,

October 2021 (4

th

revision)

Information notice

found at: www.iea.org/

corrections

Foreword 3

Foreword

Weareapproachingadecisivemomentforinternationaleffortstotackletheclimatecrisis–

agreatchallengeofourtimes.Thenumberofcountriesthathavepledgedtoreachnet‐zero

emissionsbymid‐centuryorsoonaftercontinuestogrow,butsodoglobalgreenhousegas

emissions.Thisgapbetweenrhetoricandactionneedstocloseifwearetohaveafighting

chanceofreachingnetzeroby2050andlimitingtheriseinglobaltemperaturesto1.5°C.

Doingsorequiresnothingshortofatotaltransformationoftheenergysystemsthatunderpin

oureconomies.Weareinacriticalyearatthestartofacriticaldecadefortheseefforts.The

26thConferenceoftheParties(COP26)oftheUnitedNationsFrameworkConventionon

ClimateChangeinNovemberisthefocalpointforstrengtheningglobalambitionsandaction

onclimatebybuildingonthefoundationsofthe2015ParisAgreement.TheInternational

Energy Agency (IEA) has been working hard to support the UK government’s COP26

Presidencytohelpmakeitthesuccesstheworldneeds.Iwasdelightedtoco‐hosttheIEA‐

COP26NetZeroSummitwithCOP26PresidentAlokSharmainMarch,wheretopenergyand

climateleadersfrommorethan40countrieshighlightedtheglobalmomentumbehindclean

energytransitions.

Thediscussions atthat event fed intothis special report, notablythroughtheSevenKey

PrinciplesforImplementingNetZerothattheIEApresentedattheSummit,whichhavebeen

backedby22ofourmembergovernmentstodate.Thisreportmapsout howtheglobal

energysectorcanreachnetzeroby2050.Ibelievethereport–NetZeroby2050:Aroadmap

fortheglobalenergysystem–isoneofthemostimportantandchallengingundertakingsin

theIEA’shistory.TheRoadmapistheculminationoftheIEA’spioneeringworkonenergy

datamodelling,combiningforthefirsttimethecomplexmodelsofourtwoflagshipseries,

theWorldEnergyOutlookandEnergyTechnologyPerspectives.ItwillguidetheIEA’swork

andwillbeanintegralpartofboththoseseriesgoingforward.

Despitethecurrentgapbetweenrhetoricandrealityonemissions,ourRoadmapshowsthat

therearestillpathwaystoreachnetzeroby2050.Theoneonwhichwefocusis–inour

analysis–themosttechnicallyfeasible,cost‐effectiveandsociallyacceptable.Evenso,that

pathway remains narrow and extremely challenging, requiring allstakeholders–

governments,businesses,investorsandcitizens–totakeactionthisyearandeveryyear

aftersothatthegoaldoesnotslipoutofreach.

This report sets out clear milestones – more than 400 in total, spanning all sectors and

technologies–forwhatneedstohappen,andwhen,totransformtheglobaleconomyfrom

onedominatedbyfossilfuelsintoonepoweredpredominantlyby renewableenergylike

solarandwind.Ourpathwayrequiresvastamountsofinvestment,innovation,skilfulpolicy

designandimplementation,technologydeployment,infrastructurebuilding,international

co‐operationandeffortsacrossmanyotherareas.

SincetheIEA’sfoundingin1974,oneofitscoremissionshasbeentopromotesecureand

affordableenergysuppliestofostereconomicgrowth.Thishasremainedakeyconcernof

ourRoadmap,drawingonspecialanalysiscarriedoutwiththeInternationalMonetaryFund

and the International Institute for Applied Systems Analysis. It shows that the enormous

IEA. All rights reserved.

4 International Energy Agency | Special Report

challengeoftransformingourenergysystemsisalsoahugeopportunityforoureconomies,

withthepotentialtocreatemillionsofnewjobsandboosteconomicgrowth.

AnotherguidingprincipleoftheRoadmapisthatcleanenergytransitionsmustbefairand

inclusive,leavingnobodybehind.Wehavetoensurethatdevelopingeconomiesreceivethe

financingandtechnologicalknow‐howtheyneedtocontinuebuildingtheirenergysystems

tomeettheneedsoftheirexpandingpopulationsandeconomiesinasustainableway.Itis

amoralimperativetobringelectricitytothehundredsofmillionsofpeoplewhocurrently

aredeprivedofaccesstoit,themajorityinoftheminAfrica.

Thetransitiontonetzeroisforandaboutpeople.Itisparamounttoremainawarethatnot

everyworkerinthefossilfuelindustrycaneaseintoacleanenergyjob,sogovernments

needtopromotetraininganddevoteresources tofacilitatingnewopportunities.Citizens

mustbeactiveparticipantsintheentireprocess,makingthemfeelpartofthetransitionand

notsimplysubjecttoit.Thesethemesareamongthosebeingexplored by the Global

CommissiononPeople‐CentredCleanEnergyTransitions,whichIconvenedatthestartof

2021 to examine how to enable citizens to benefit from the opportunities and navigate

the disruptions of the shift to a clean energy economy. Headed byPrimeMinister

MetteFrederiksen of Denmark and composed of government leaders, ministers and

prominentthinkers,theGlobalCommissionwillmakepublicitskeyrecommendationsahead

ofCOP26inNovember.

ThepathwaylaidoutinourRoadmapisglobalinscope,buteachcountrywillneedtodesign

itsownstrategy,takingintoaccountitsspecificcircumstances.Thereisnoone‐size‐fits‐all

approach to clean energy transitions. Plans need to reflect countries’ differing stages of

economicdevelopment:inourpathway,advancedeconomiesreachnet zero before

developingeconomiesdo.Astheworld’sleadingenergyauthority,theIEAstandsreadyto

provide governments with support and advice as they design and implement their own

roadmaps,andtoencouragetheinternationalco‐operationacrosssectorsthatissoessential

toreachingnetzeroby2050.

Thislandmarkreportwouldnothavebeenpossiblewithouttheextraordinarydedicationof

theIEAcolleagueswhohaveworkedsotirelesslyandrigorouslyonit.Iwouldliketothank

the entire team under the outstanding leadership of my colleagues LauraCozzi and

TimurGül.

The world has a huge challenge ahead of it to move net zero by 2050 from a narrow

possibility to a practical reality. Global carbon dioxide emissions are already rebounding

sharplyaseconomiesrecoverfromlastyear’spandemic‐inducedshock.Itispasttimefor

governmentstoact,andactdecisivelytoacceleratethecleanenergytransformation.

Asthisreportshows,weattheIEAarefullycommittedtoleadingthoseefforts.

DrFatihBirol

ExecutiveDirector

InternationalEnergyAgency

Acknowledgements 5

Acknowledgements

Thisstudy,across‐agencyeffort,waspreparedbytheWorldEnergyOutlookteamandthe

EnergyTechnologyPerspectivesteam.ThestudywasdesignedanddirectedbyLauraCozzi,

ChiefEnergyModellerandHeadofDivisionforEnergyDemandOutlook, and TimurGül,

HeadofDivisionforEnergyTechnologyPolicy.

The lead authors and co‐ordinators were: StéphanieBouckaert, AraceliFernandezPales,

ChristopheMcGlade, UweRemme and BrentWanner. LaszloVarro, Chief Economist,

DavideD’AmbrosioandThomasSpencerwerealsopartofthecoreteam.

The other main authors were: ThibautAbergel (buildings), YasmineArsalane (economic

outlook,electricity),PraveenBains(biofuels),JoseMiguelBermudezMenendez(hydrogen),

ElizabethConnelly (transport), DanielCrow (behaviour), AmritaDasgupta (innovation),

ChiaraDelmastro (buildings), TimothyGoodson (buildings, bioenergy), AlexandreGouy

(industry), PaulHugues (industry), LillyLee (transport), PeterLevi (industry),

HanaMandova (industry), ArianeMillot (buildings), PawełOlejarnik (fossil fuel supply),

LeonardoPaoli (innovation, transport), FaidonPapadimoulis(datamanagement),

SebastianPapapanagiotou (electricity networks), FrancescoPavan (hydrogen),

ApostolosPetropoulos (transport), RyszardPośpiech(datamanagement),LeonieStaas

(behaviour, industry), JacopoTattini (transport), JacobTeter (transport), GianlucaTonolo

(energyaccess),TiffanyVass(industry)andDanielWetzel(jobs).

Other contributors were: Lucila Arboleya Sarazola, Simon Bennett, Cyril Cassisa, Arthur

Contejean, Musa Erdogan, Enrique Gutierrez Tavarez, Taku Hasegawa,ShaiHassid,Zoe

Hungerford, Tae‐Yoon Kim, Vanessa Koh, Luca Lo Re, Christopher Lowans, Raimund

Malischek,MariachiaraPolisenaandPerAndersWidell.

CarolineAbettan,TeresaCoon,MarinaDosSantos,MarieFournier‐S’niehotta,RekaKoczka

andDianaLouis

providedessentialsupport.

EdmundHoskercarriededitorialresponsibilityandDebraJustuswasthecopy‐editor.

The International Monetary Fund (IMF), in particular BenjaminHunt, FlorenceJaumotte,

JaredThomasBebee and SusannaMursula, partnered with the IEA toprovidethe

macroeconomicanalysis.TheInternationalInstituteforAppliedSystemsAnalysis(IIASA),in

particularPeterRafaj,GregorKiesewetter,WolfgangSchöpp,ChrisHeyes,ZbigniewKlimont,

PallavPurohit,LauraWarnecke,BinhNguyen,NicklasForsell,StefanFrank,PetrHavlikand

MykolaGusti, partnered with the IEA to provide analysis and related indicators on air

pollutionandgreenhousegasemissionsfromlanduse.

Valuable comments and feedback were provided by other senior management and

numerous other colleagues within the International Energy Agency. In particular

KeisukeSadamori, MechthildWörsdörfer, AmosBromhead, DanDorner, NickJohnstone,

PascalLaffont, TorilBosoni, PeterFraser, PaoloFrankl, TimGould, TomHowes,

BrianMotherway, Aad van Bohemen, César Alejandro Hernández, Samantha McCulloch,

SaraMoarif, HeymiBahar, AdamBaylin‐Stern, NielsBerghout, SaraBudinis,

Jean‐BaptisteDubreuil, Carlos Fernández Alvarez,Ilkka Hannula , Jeremy Moorhouse and

StefanLorenczik.

IEA. All rights reserved.

6 International Energy Agency | Special Report

Valuableinputtotheanalysiswasprovidedby:TrevorMorgan(independentconsultant)and

DavidWilkinson(independentconsultant).

ThanksgototheIEACommunicationsandDigitalOffice(CDO),particularlytoJadMouawad,

HeadofCDO,andtoAstridDumond,JonCuster,TanyaDyhin,MerveErdil,GraceGordon,

ChristopherGully,JethroMullen,JuliePuech,RobStone,GregoryViscusi,ThereseWalshand

WonjikYangfortheirhelpinproducingandpromotingthereportandwebsitematerials.

Finally,thankstoIvoLetraoftheIEAInformationSystemsUnitforhisessentialsupportin

theproductionprocess,andtotheIEA’sOfficeofLegalCounsel,OfficeofManagementand

Administration, and EnergyData Centre forthe assistance eachprovided throughoutthe

preparationofthisreport.

Peerreviewers

Manysenior government officialsand international experts providedinput and reviewed

preliminarydraftsofthereport.Theircommentsandsuggestionswereofgreatvalue.They

include:

AimeeAguilarJaber OrganisationforEconomicCo‐operationandDevelopment(OECD)

KeigoAkimoto ResearchInstituteofInnovativeTechnologyfortheEarth,Japan

DougArent NationalRenewableEnergyLaboratory(NREL),UnitedStates

DanielBalog PermanentDelegationofHungarytotheOECD

GeorgBäuml Volkswagen

HarmeetBawa HitachiABBPowerGrids

PeteBetts GranthamResearchInstituteonClimateChangeandthe

Environment,UnitedKingdom

SamaBilbaoyLeon WorldNuclearAssociation

DianeCameron NuclearEnergyAgency

RebeccaCollyer EuropeanClimateFoundation

RussellConklin USDepartmentofEnergy

FrançoisDassa EDF

JeltedeJong MinistryofEconomicAffairsandClimatePolicy,TheNetherlands

CarldeMaré ArcelorMittal

GuillaumeDeSmedt AirLiquide

AgustinDelgado Iberdrola

JohannaFiksdahl PermanentDelegationofNorwaytotheOECD

AlanFinkel SpecialAdvisortotheAustralianGovernmentonLowEmissions

Technology

NiklasForsell InternationalInstituteforAppliedSystemsAnalysis(IIASA)

JamesFoster UKDepartmentforBusiness,EnergyandIndustrialStrategy

HiroyukiFukui Toyota

RosannaFusco Eni

LiGao MinistryofEcologyandEnvironmentofthePeople’sRepublicof

China

Acknowledgements 7

FrançoisGautier PermanentDelegationofFrancetotheOECD

OliverGeden GermanInstituteforInternationalandSecurityAffairs

DolfGielen InternationalRenewableEnergyAgency(IRENA)

FrancescaGostinelli Enel

JaeH.Jung MinistryofForeignAffairs,RepublicofKorea

MichaelHackethal MinistryforEconomicAffairsandIndustry,Germany

PeterWood Shell

SelwinHart UnitedNations

DavidHawkings NaturalResourcesDefenseCouncil

JacobHerbers USDepartmentofEnergy

TakashiHongo Mitsui&Co.GlobalStrategicStudiesInstitute,Japan

ChristinaHood CompassClimate,NewZealand

MichaelKelly WorldLPGAssociation

SirDavidKing CambridgeUniversity

KenKoyama TheInstituteofEnergyEconomics,Japan

FabienKreuzer DGEnergy,EuropeanCommission

JoyceLee GlobalWindEnergyCouncil(GWEC)

ChenLinhao MinistryofScienceandTechnologyofthePeople’sRepublicof

China

ToddLitman VictoriaTransportPolicyInstitute,Canada

ClaudeLorea GlobalCementandConcreteAssociation

RituMathur TheEnergyandResourcesInstitute(TERI)

VincentMinier SchneiderElectric

SteveNadel AmericanCouncilforanEnergy‐EfficientEconomy

StefanNowak TechnologyCollaborationProgrammeonPhotovoltaicPower

Systems(PVPSTCP)

BrianÓGallachóir MaREI,SFIResearchCentreforEnergy,ClimateandMarine,

UniversityCollegeCork

HenriPaillère InternationalAtomicEnergyAgency(IAEA)

YongdukPak KoreaEnergyEconomicsInstitute(KEEI)

AlessandraPastorelli PermanentDelegationofItalytotheOECD

JonathanPershing USStateDepartment

GlenPeters CentreforInternationalClimateandEnvironmentalResearch

(CICERO)

StephaniePfeifer InstitutionalInvestorsGrouponClimateChange(IIGCC)

CédricPhilibert Independentconsultant

LynnPrice LawrenceBerkeleyNationalLaboratory,UnitedStates

AndrewPurvis WorldSteel

JuliaReinaud BreakthroughEnergy

YaminaSaheb OpenEXP

IgnacioSantelices SustainableEnergyAgency,Chile

AndreasSchäfer UniversityCollegeLondon

VivianScott TheUniversityofEdinburgh

8 International Energy Agency | Special Report

SimonSharpe CabinetOffice,UnitedKingdom

AdnanShihabEldin FormerlyKuwaitFoundationfortheAdvancementofSciences

ToshiyukiShirai MinistryofEconomy,TradeandIndustry,Japan

AdamSieminski KAPSARC

StephanSinger ClimateActionNetwork

VarunSivaram USStateDepartment

JimSkea ImperialCollegeLondon

JeffStehm TaskForceonClimate‐RelatedFinancialDisclosures

JonathanStern OxfordInstituteforEnergyStudies

WimThomas Independentconsultant

DavidTurk USDepartmentofEnergy

FritjofUnander ResearchCouncilofNorway

RobvanderMeer TheEuropeanCementAssociation(CEMBUREAU)

NoévanHulst InternationalPartnershipforHydrogenandFuelCellsinthe

Economy

TomvanIerland DGforClimateAction,EuropeanCommission

DavidVictor UniversityofCalifornia,SanDiego

AmandaWilson NaturalResourcesCanada

HaraldWinkler UniversityofCapeTown

MarkusWolf ElectricPowerResearchInstitute(EPRI),UnitedStates

MarkusWråke SwedishEnergyResearchCentre

WilliamZimmern BP

Theindividualsandorganisationsthatcontributedtothisstudyarenotresponsibleforany

opinionsorjudgmentsitcontains.Allerrorsandomissionsaresolelytheresponsibilityofthe

IEA.

This document and any map included herein are without prejudicetothestatusofor

sovereigntyoveranyterritory,tothedelimitationofinternationalfrontiersandboundaries

andtothenameofanyterritory,cityorarea.

Commentsandquestionsarewelcomeandshouldbeaddressedto:

LauraCozziandTimurGül

DirectorateofSustainability,TechnologyandOutlooks

InternationalEnergyAgency

9,ruedelaFédération

75739ParisCedex15

France

E‐mail:IEAN[email protected]

Web:www.iea.org

Table of Contents 9

TableofContents

Foreword...........................................................................................................................3

Acknowledgements...........................................................................................................5

Executivesummary.........................................................................................................13

Announcednetzeropledgesandtheenergysector 29

1.1 Introduction...................................................................................................30

1.2 Emissionsreductiontargetsandnetzeropledges........................................31

1.2.1 NationallyDeterminedContributions...............................................31

1.2.2 Net‐zeroemissionspledges...............................................................32

1.3 OutlookforemissionsandenergyintheSTEPS............................................36

1.3.1 CO

2

emissions....................................................................................36

1.3.2 Totalenergysupply,totalfinalconsumptionandelectricity

generation.........................................................................................37

1.3.3 Emissionsfromexistingassets..........................................................39

1.4 AnnouncedPledgesCase...............................................................................40

1.4.1 CO

2

emissions....................................................................................41

1.4.2 Totalenergysupply...........................................................................43

1.4.3 Totalfinalconsumption.....................................................................44

1.4.4 Electricitygeneration.........................................................................45

Aglobalpathwaytonet‐zeroCO₂emissionsin2050 47

2.1 Introduction...................................................................................................48

2.2 Scenariodesign..............................................................................................48

2.2.1 PopulationandGDP...........................................................................50

2.2.2 EnergyandCO

2

prices........................................................................51

2.3 CO

2

emissions................................................................................................53

2.4 Totalenergysupplyandtotalfinalconsumption..........................................56

2.4.1 Totalenergysupply...........................................................................56

2.4.2 Totalfinalconsumption.....................................................................60

2.5 Keypillarsofdecarbonisation.......................................................................64

2.5.1 Energyefficiency................................................................................65

2.5.2 Behaviouralchange...........................................................................67

2.5.3 Electrification.....................................................................................70

1

2

IEA. All rights reserved.

10 International Energy Agency | Special Report

2.5.4 Renewables.......................................................................................73

2.5.5 Hydrogenandhydrogen‐basedfuels.................................................75

2.5.6 Bioenergy...........................................................................................77

2.5.7 Carboncapture,utilisationandstorage............................................79

2.6 Investment....................................................................................................81

2.7 Keyuncertainties...........................................................................................83

2.7.1 Behaviouralchange...........................................................................84

2.7.2 Bioenergyandland‐usechange.........................................................90

2.7.3 CCUSappliedtoemissionsfromfossilfuels......................................94

Sectoralpathwaystonet‐zeroemissionsby2050 99

3.1 Introduction.................................................................................................100

3.2 Fossilfuelsupply.........................................................................................100

3.2.1 EnergytrendsintheNet‐ZeroEmissionsScenario..........................100

3.2.2 Investmentinoilandgas.................................................................103

3.2.3 Emissionsfromfossilfuelproduction..............................................104

3.3 Low‐emissionsfuelsupply...........................................................................105

3.3.1 EnergytrendsintheNet‐ZeroEmissionsScenario..........................105

3.3.2 Biofuels............................................................................................106

3.3.3 Hydrogenandhydrogen‐basedfuels...............................................108

3.3.4 Keymilestonesanddecisionpoints.................................................111

3.4 Electricitysector..........................................................................................113

3.4.1 EnergyandemissionstrendsintheNet‐ZeroEmissionsScenario..113

3.4.2 Keymilestonesanddecisionpoints.................................................117

3.5 Industry.......................................................................................................121

3.5.1 EnergyandemissiontrendsintheNet‐ZeroEmissionsScenario....121

3.5.2 Keymilestonesanddecisionpoints.................................................129

3.6 Transport.....................................................................................................131

3.6.1 EnergyandemissiontrendsintheNet‐ZeroEmissionsScenario....131

3.6.2 Keymilestonesanddecisionpoints.................................................138

3.7 Buildings......................................................................................................141

3.7.1 EnergyandemissiontrendsintheNet‐ZeroEmissionsScenario....141

3.7.2 Keymilestonesanddecisionpoints.................................................147

3

Table of Contents 11

Widerimplicationsofachievingnet‐zeroemissions 151

4.1 Introduction.................................................................................................152

4.2 Economy......................................................................................................153

4.2.1 Investmentandfinancing................................................................153

4.2.2 Economicactivity.............................................................................155

4.2.3 Employment....................................................................................157

4.3 Energyindustry............................................................................................160

4.3.1 Oilandgas.......................................................................................160

4.3.2 Coal..................................................................................................162

4.3.3 Electricity.........................................................................................163

4.3.4 Energy‐consumingindustries..........................................................165

4.4 Citizens........................................................................................................167

4.4.1 Energy‐relatedSustainableDevelopmentGoals.............................167

4.4.2 Affordability.....................................................................................170

4.4.3 Behaviouralchanges........................................................................173

4.5 Governments...............................................................................................175

4.5.1 Energysecurity................................................................................175

4.5.2 Infrastructure...................................................................................180

4.5.3 Taxrevenuesfromretailenergysales.............................................183

4.5.4 Innovation........................................................................................184

4.5.5 Internationalco‐operation..............................................................187

Annexes 191

AnnexA.Tablesforscenarioprojections.......................................................................193

AnnexB.Technologycosts............................................................................................201

AnnexC.Definitions......................................................................................................203

AnnexD.References.....................................................................................................217

4

IEA. All rights reserved.

Summary for policy makers 13

Summaryforpolicymakers

The energy sector is the source of around three‐quarters of greenhouse gas emissions

today and holds the key to averting the worst effects of climate change, perhaps the

greatestchallengehumankindhasfaced.Reducingglobalcarbondioxide(CO

2

)emissionsto

netzeroby2050isconsistentwitheffortstolimitthelong‐termincreaseinaverageglobal

temperaturesto1.5°C.Thiscallsfornothinglessthanacompletetransformationofhowwe

produce,transportandconsumeenergy.Thegrowingpoliticalconsensusonreachingnet

zeroiscausefor considerableoptimismabout theprogressthe world canmake,butthe

changesrequiredtoreachnet‐zeroemissionsgloballyby2050arepoorlyunderstood.Ahuge

amountofworkisneededtoturntoday’simpressiveambitionsintoreality,especiallygiven

therangeofdifferentsituationsamongcountriesandtheirdifferingcapacitiestomakethe

necessarychanges.ThisspecialIEAreportsetsoutapathwayforachievingthisgoal,resulting

inacleanandresilientenergysystemthatwouldbringmajorbenefitsforhumanprosperity

andwell‐being.

The global pathway to net‐zero emissions by 2050 detailed in this report requires all

governmentstosignificantlystrengthenandthensuccessfullyimplementtheirenergyand

climate policies.Commitmentsmadetodatefallfarshortofwhatisrequiredbythat

pathway. The number of countries that have pledged to achieve net‐zero emissions has

grownrapidlyoverthelastyearandnowcoversaround70%ofglobalemissionsofCO

2

.This

isahugestepforward.However,mostpledgesarenotyetunderpinnedbynear‐termpolicies

andmeasures.Moreover,evenifsuccessfullyfulfilled,thepledgestodatewouldstillleave

around22billiontonnesofCO

2

emissionsworldwidein2050.Thecontinuationofthattrend

wouldbeconsistentwithatemperaturerisein2100ofaround2.1°C.Globalemissionsfell

in2020becauseof the Covid‐19 crisisbutarealready reboundingstronglyaseconomies

recover.Furtherdelayinactingtoreversethattrendwillputnetzeroby2050outofreach.

InthisSummaryforPolicyMakers,weoutlinetheessentialconditionsfortheglobalenergy

sector to reach net‐zero CO

2

emissions by 2050.The pathway described indepthinthis

reportachievesthisobjectivewithnooffsetsfromoutsidetheenergysector,andwithlow

relianceonnegativeemissionstechnologies.Itisdesignedtomaximisetechnicalfeasibility,

cost‐effectiveness and social acceptance while ensuring continued economic growth and

secureenergysupplies.Wehighlightthepriorityactionsthatareneededtodaytoensurethe

opportunityofnetzeroby2050–narrowbutstillachievable–isnotlost.Thereportprovides

a global view, but countries do not start in the same place or finish at the same time:

advanced economies have to reachnetzerobeforeemergingmarkets and developing

economies,andassistothersingettingthere.Wealsorecognisethattheroutemappedout

hereisapath,notnecessarilythepath,andsoweexaminesomekeyuncertainties,notably

concerningtherolesplayedbybioenergy,carboncaptureandbehaviouralchanges.Getting

tonetzerowillinvolvecountlessdecisionsbypeopleacrosstheworld,butourprimaryaim

istoinformthedecisionsmadebypolicymakers,whohavethegreatestscopetomovethe

worldclosertoitsclimategoals.

IEA. All rights reserved.

14 International Energy Agency | Special Report

Netzeroby2050hingesonanunprecedentedcleantechnologypushto2030

Thepathtonet‐zeroemissionsisnarrow:stayingonitrequiresimmediateandmassive

deployment of all available clean and efficient energy technologies. In the net‐zero

emissionspathwaypresentedinthisreport,theworldeconomyin2030issome40%larger

thantodaybutuses7%lessenergy.Amajorworldwidepushtoincreaseenergyefficiencyis

an essential part of these efforts, resulting in the annual rate of energy intensity

improvementsaveraging4%to2030–aboutthree‐timestheaveragerateachievedoverthe

lasttwodecades.EmissionsreductionsfromtheenergysectorarenotlimitedtoCO

2

:inour

pathway,methaneemissionsfromfossilfuelsupplyfallby75%overthenexttenyearsasa

result of a global, concerted effort to deploy all available abatement measures and

technologies.

Ever‐cheaperrenewableenergytechnologiesgiveelectricitytheedgeintheracetozero.

Ourpathwaycallsforscalingupsolarandwindrapidlythisdecade,reachingannualadditions

of630gigawatts(GW)ofsolarphotovoltaics(PV)and390GWofwindby2030,four‐times

therecordlevelssetin2020.ForsolarPV,thisisequivalenttoinstallingtheworld’scurrent

largestsolarparkroughlyeveryday.Hydropowerandnuclear,thetwolargestsourcesof

low‐carbon electricity today, provide an essential foundation for transitions. As the

electricitysectorbecomescleaner,electrificationemergesasacrucialeconomy‐widetool

forreducingemissions.Electricvehicles(EVs)gofromaround5%ofglobalcarsalestomore

than60%by2030.

Make the 2020s the decade of massive clean energy expansion

Allthetechnologiesneededtoachievethenecessarydeepcutsinglobalemissionsby

2030alreadyexist,andthepoliciesthatcandrivetheirdeploymentarealreadyproven.

AstheworldcontinuestograpplewiththeimpactsoftheCovid‐19 pandemic, it is

essential that the resulting wave of investment and spending to support economic

recoveryisalignedwiththenetzeropathway.Policiesshouldbestrengthenedtospeed

thedeploymentofcleanandefficientenergytechnologies.Mandatesandstandardsare

vital to drive consumer spending and industry investment into the most efficient

technologies.Targetsandcompetitiveauctionscanenablewindandsolartoaccelerate

theelectricitysectortransition.Fossilfuelsubsidyphase‐outs,carbonpricingandother

market reforms can ensure appropriate price signals. Policies should limit or provide

disincentivesfortheuseofcertainfuelsandtechnologies,suchasunabatedcoal‐fired

power stations, gas boilers and conventional internal combustion engine vehicles.

Governments must lead the planning and incentivising of the massive infrastructure

investment,includinginsmarttransmissionanddistributiongrids.

PRIORITYACTION

Summary for policy makers 15

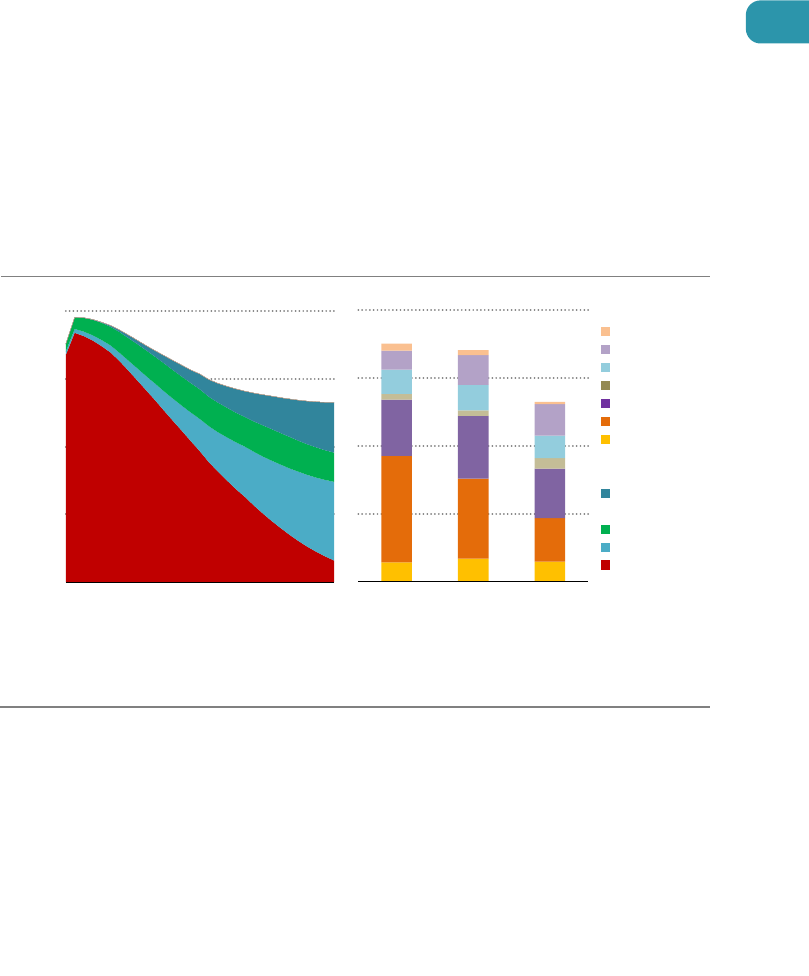

Key clean technologies ramp up by 2030 in the net zero pathway

Note:MJ=megajoules;GDP=grossdomesticproductinpurchasingpowerparity.

Netzeroby2050requireshugeleapsincleanenergyinnovation

Reachingnetzeroby2050requiresfurtherrapiddeploymentofavailabletechnologiesas

wellaswidespreaduseoftechnologiesthatarenotonthemarketyet.Majorinnovation

effortsmustoccuroverthisdecadeinordertobringthesenewtechnologiestomarketin

time.MostoftheglobalreductionsinCO

2

emissionsthrough2030inourpathwaycomefrom

technologies readily available today. But in 2050, almost half the reductions come from

technologiesthatarecurrentlyatthedemonstrationorprototypephase.Inheavyindustry

andlong‐distancetransport,theshareofemissionsreductionsfromtechnologiesthatare

stillunderdevelopmenttodayisevenhigher.

Thebiggestinnovationopportunitiesconcernadvancedbatteries,hydrogenelectrolysers,

and direct air capture and storage.Together,thesethreetechnologyareasmakevital

contributions the reductions in CO

2

emissions between 2030 and 2050 in our pathway.

Innovationoverthenexttenyears–notonlythroughresearchanddevelopment(R&D)and

demonstrationbutalsothroughdeployment–needstobeaccompaniedbythelarge‐scale

constructionoftheinfrastructurethetechnologieswillneed.Thisincludesnewpipelinesto

transportcapturedCO

2

emissionsandsystemstomovehydrogenaroundandbetweenports

andindustrialzones.

10

20

30

40

50

60

2020 2030

x18

200

400

600

800

1000

1200

2020 2030

x4

SolarPV

Wind

Capacity additions

(GW)

Electriccarsales

(millions)

Energy intensityofGD

P

(MJperUSDppp)

1

2

3

4

5

2020 2030

4% per

year

IEA. All rights reserved.

16 International Energy Agency | Special Report

Prepare for the next phase of the transition by boosting innovation

Clean energy innovation must accelerate rapidly, with governments putting R&D,

demonstrationanddeploymentatthecoreofenergyandclimatepolicy.

GovernmentR&Dspendingneedstobeincreasedandreprioritised.Criticalareassuchas

electrification,hydrogen,bioenergyandcarboncapture,utilisationandstorage(CCUS)

today receive only around one‐third of the level of public R&D funding of the more

established low‐carbon electricity generation and energy efficiency technologies.

Supportisalsoneededtoacceleratetheroll‐outofdemonstrationprojects,toleverage

privateinvestmentinR&D,andtoboostoveralldeploymentlevelstohelpreducecosts.

AroundUSD90billionofpublicmoneyneedstobemobilisedgloballyassoonaspossible

tocompleteaportfolioofdemonstrationprojectsbefore2030.Currently,onlyroughly

USD25billionisbudgetedforthatperiod.Developinganddeployingthesetechnologies

would create major new industries, as well as commercial and employment

opportunities.

Annual CO

2

emissions savings in the net zero pathway, relative to 2020

20% 40% 60% 80% 100%

2030

2050

Behaviourchanges Technologiesinthemarket Technologiesunderdevelopment

PRIORITYACTION

Summary for policy makers 17

Thetransitiontonetzeroisforandaboutpeople

Atransitionofthescaleandspeeddescribedbythenetzeropathwaycannotbeachieved

withoutsustainedsupportandparticipationfromcitizens.Thechangeswillaffectmultiple

aspectsofpeople’slives–fromtransport,heatingandcookingtourbanplanningandjobs.

Weestimatethataround55%ofthecumulativeemissionsreductionsinthepathwayare

linked to consumer choices such as purchasing an EV, retrofittingahousewithenergy‐

efficient technologies or installing a heat pump. Behavioural changes, particularly in

advancedeconomies–suchasreplacingcartripswithwalking,cyclingorpublictransport,

or foregoing a long‐haul flight – also provide around 4% of the cumulative emissions

reductions.

Providingelectricitytoaround785millionpeoplethathavenoaccessandcleancooking

solutionsto2.6billionpeoplethatlackthoseoptionsisanintegralpartofourpathway.

Emissionsreductionshavetogohand‐in‐handwitheffortstoensureenergyaccessforallby

2030.ThiscostsaroundUSD40billionayear,equaltoaround1%ofaverageannualenergy

sectorinvestment,whilealsobringingmajorco‐benefitsfromreducedindoorairpollution.

Someofthechangesbroughtbythecleanenergytransformationmaybechallengingto

implement,sodecisionsmustbetransparent,justandcost‐effective.Governmentsneed

toensurethatcleanenergytransitionsarepeople‐centredandinclusive.Householdenergy

expenditureasashareofdisposableincome–includingpurchasesofefficientappliances

andfuelbills–risesmodestlyinemergingmarketanddevelopingeconomiesinournetzero

pathway as more people gain access to energy and demand for modern energy services

increases rapidly. Ensuring the affordability of energy for households demands close

attention:policytoolsthatcandirectsupporttothepoorestincludetaxcredits,loansand

targetedsubsidies.

Clean energy jobs will grow strongly but must be spread widely

Energy transitions have to take account of the social and economic impacts on

individualsandcommunities,andtreatpeopleasactiveparticipants.

Thetransitionto net zerobringssubstantial new opportunitiesforemployment,with

14millionjobscreatedby2030inourpathwaythankstonewactivitiesandinvestment

incleanenergy.Spendingonmoreefficientappliances,electricandfuelcellvehicles,and

building retrofits and energy‐efficient construction wouldrequire a further 16 million

workers.Buttheseopportunitiesareoftenindifferentlocations,skillsetsandsectors

thanthejobsthatwillbelostasfossilfuelsdecline.Inourpathway,around5millionjobs

arelost.Mostofthosejobsarelocatedclosetofossilfuelresources,andmanyarewell

paid,meaningstructuralchangescancauseshocksforcommunitieswithimpactsthat

persist over time. This requires careful policy attention to address the employment

PRIORITYACTION

IEA. All rights reserved.

18 International Energy Agency | Special Report

losses.Itwillbevitaltominimisehardshipsassociatedwiththesedisruptions,suchasby

retrainingworkers,locatingnewcleanenergyfacilitiesinheavilyaffectedareaswherever

possible,andprovidingregionalaid.

Global employment in energy supply in the net zero pathway, 2019-2030

Anenergysectordominatedbyrenewables

Inthenetzeropathway,globalenergydemandin2050isaround8%smallerthantoday,

but it serves an economy more than twice as big and a population with 2 billion more

people.Moreefficientuseofenergy,resourceefficiencyandbehaviouralchangescombine

tooffsetincreasesindemandforenergyservicesastheworldeconomygrowsandaccessto

energyisextendedtoall.

Insteadoffossilfuels,theenergysectorisbasedlargelyonrenewableenergy.Two‐thirds

oftotalenergysupplyin2050isfromwind,solar,bioenergy,geothermalandhydroenergy.

Solar becomes the largest source, accounting for one‐fifth of energy supplies. Solar PV

capacityincreases20‐foldbetweennowand2050,andwindpower11‐fold.

Netzeromeansahugedeclineintheuseoffossilfuels.Theyfallfromalmostfour‐fifthsof

totalenergysupplytodaytoslightlyoverone‐fifthby2050.Fossilfuelsthatremainin2050

areusedingoodswherethecarbonisembodiedintheproductsuchasplastics,infacilities

fittedwithCCUS,andinsectorswherelow‐emissionstechnologyoptionsarescarce.

Electricityaccountsforalmost50%oftotalenergyconsumptionin2050.Itplaysakeyrole

acrossallsectors–fromtransportandbuildingstoindustry–andisessentialtoproducelow‐

emissionsfuelssuchashydrogen.Toachievethis,totalelectricitygenerationincreasesover

20

40

60

2019 2030

Millionjobs

Bioenergy

Electricity

Coal

Oilandgas

Losses

Growth

Summary for policy makers 19

two‐and‐a‐half‐timesbetweentodayand2050.Atthesametime,noadditionalnewfinal

investmentdecisionsshouldbetakenfornewunabatedcoalplants,theleastefficientcoal

plants are phased out by 2030, and the remaining coal plants still in use by 2040 are

retrofitted.By2050,almost90%ofelectricitygenerationcomesfromrenewablesources,

withwindandsolarPVtogetheraccountingfornearly70%.Mostoftheremaindercomes

fromnuclear.

Emissionsfromindustry,transportandbuildingstakelongertoreduce.Cuttingindustry

emissionsby95%by2050involvesmajoreffortstobuildnewinfrastructure.Afterrapid

innovationprogressthroughR&D,demonstrationandinitialdeploymentbetweennowand

2030tobringnewcleantechnologiestomarket,theworldthenhastoputthemintoaction.

Everymonthfrom2030onwards,tenheavyindustrialplantsareequippedwithCCUS,three

newhydrogen‐basedindustrialplantsarebuilt,and2GWofelectrolysercapacityareadded

atindustrialsites.Policiesthatendsalesofnewinternalcombustionenginecarsby2035and

boostelectrificationunderpinthemassivereductionintransportemissions.In2050,carson

theroadworldwiderunonelectricityorfuelcells.Low‐emissionsfuelsareessentialwhere

energyneedscannoteasilyoreconomicallybemetbyelectricity.Forexample,aviationrelies

largelyonbiofuelsandsyntheticfuels,andammoniaisvitalforshipping.Inbuildings,bans

onnewfossilfuelboilersneedtostartbeingintroducedgloballyin2025,drivingupsalesof

electricheatpumps.Mostoldbuildingsandallnewonescomplywithzero‐carbon‐ready

buildingenergycodes.

1

Set near-term milestones to get on track for long-term targets

Governmentsneedtoprovidecrediblestep‐by‐stepplanstoreachtheirnetzerogoals,

buildingconfidenceamonginvestors,industry,citizensandothercountries.

Governments must put inplacelong‐term policyframeworks to allow all branchesof

governmentandstakeholderstoplanforchangeandfacilitatean orderly transition.

Long‐termnationallow‐emissionsstrategies,calledforbytheParisAgreement,canset

outavisionfornationaltransitions,asthisreporthasdoneonagloballevel.Theselong‐

termobjectivesneedtobelinkedtomeasurableshort‐termtargetsand policies.Our

pathwaydetailsmorethan400sectoralandtechnologymilestonestoguidetheglobal

journeytonetzeroby2050.

1

Azero‐carbon‐readybuildingishighlyenergyefficientandeitherusesrenewableenergydirectlyorusesan

energysupplythatwillbefullydecarbonisedby2050,suchaselectricityordistrictheat.

PRIORITYACTION

IEA. All rights reserved.

20 International Energy Agency | Special Report

Key milestones in the pathway to net zero

‐5

0

5

10

15

20

25

30

35

40

2020 2025 2030 2035 2040 2045 2050

GtCO₂

Buildings Transport Industry Electricityandheat Other

2045

150 Mtlow‐carbonhydrogen

850GWelectrolysers

435Mtlow‐carbonhydrogen

3000GWelectrolysers

4GtCO

2

captured

Phase‐outof

unabatedcoalin

advancedeconomies

2030

Universalenergyaccess

60%ofglobalcar

salesareelectric

1020GWannualsolar

andwindadditions

Allnewbuildingsare

zero‐carbon‐ready

Mostnewclean

technologiesin

heavyindustry

demonstrated

atscale

Allindustrial

electricmotorsales

arebestinclass

NonewICEcarsales

2035

Overallnet‐zero

emissionselectricity

inadvanced

economies

Mostappliancesand

coolingsystemssold

arebestinclass

50%ofheavytruck

salesareelectric

7.6GtCO

2

captured

Nonewunabated

coalplantsapproved

fordevelopment

2021

2025

Nonewsalesof

fossilfuelboilers

2040

Morethan90%of

heavyindustrial

productionis

low‐emissions

2050

Almost70%of

electricitygeneration

globallyfromsolarPV

andwind

Morethan85%

ofbuildingsare

zero‐carbon‐ready

50%ofheatingdemand

metbyheatpumps

Phase‐outofall

unabatedcoalandoil

powerplants

Net‐zeroemissions

electricityglobally

50%offuelsused

inaviationare

low‐emissions

Around90%of

existingcapacityin

heavyindustries

reachesendof

investmentcycle

50%ofexisting

buildingsretrofitted

tozero‐carbon‐ready

levels

Nonewoilandgas

fieldsapprovedfor

development;no

newcoalminesor

mineextensions

Summary for policy makers 21

Thereisnoneedforinvestmentinnewfossilfuelsupplyinournetzero

pathway

Beyond projects already committed as of 2021, there are no new oil and gas fields

approvedfordevelopmentinourpathway,andnonewcoalminesormineextensionsare

required.Theunwaveringpolicyfocusonclimatechangeinthenetzeropathwayresultsin

a sharp decline in fossil fuel demand, meaning that the focus for oil and gas producers

switches entirely to output – and emissions reductions – from the operation of existing

assets.Unabatedcoaldemanddeclinesby98%tojustless than 1%oftotalenergy

usein2050.Gasdemanddeclinesby55%to1750billioncubicmetresandoildeclinesby

75%to24millionbarrelsperday(mb/d),fromaround90mb/din2020.

Cleanelectricitygeneration,networkinfrastructureandend‐usesectorsarekeyareasfor

increasedinvestment.Enablinginfrastructureandtechnologiesarevitalfortransforming

theenergysystem.Annualinvestmentintransmissionanddistributiongridsexpandsfrom

USD260billiontodaytoUSD820billionin2030.Thenumberofpublicchargingpointsfor

EVsrisesfromaround1milliontodayto40millionin2030,requiringannualinvestmentof

almostUSD90billionin2030.AnnualbatteryproductionforEVsleapsfrom160gigawatt‐

hours(GWh)todayto6600GWhin2030–theequivalentofaddingalmost20gigafactories

2

eachyearforthenexttenyears.Andtherequiredroll‐outofhydrogenandCCUSafter2030

means laying the groundwork now: annual investment in CO

2

pipelines and hydrogen‐

enablinginfrastructureincreasesfromUSD1billiontodaytoaroundUSD40billionin2030.

Drive a historic surge in clean energy investment

Policiesneedtobedesignedtosendmarketsignalsthatunlocknewbusinessmodels

andmobiliseprivatespending,especiallyinemergingeconomies.

Accelerateddeliveryofinternationalpublicfinancewillbecriticaltoenergytransitions,

especiallyindevelopingeconomies,butultimatelytheprivatesectorwillneedtofinance

most of the extra investment required. Mobilising the capital for large‐scale

infrastructurecallsforcloserco‐operation between developers, investors, public

financialinstitutionsandgovernments.Reducingrisksforinvestorswillbeessentialto

ensuresuccessfulandaffordablecleanenergytransitions.Manyemergingmarketand

developingeconomies,whichrelymainlyonpublicfundingfornewenergyprojectsand

industrialfacilities,willneedtoreformtheirpolicyandregulatoryframeworkstoattract

moreprivatefinance.Internationalflowsoflong‐termcapitaltotheseeconomieswillbe

needed to support the development of both existing and emergingcleanenergy

technologies.

2

Batterygigafactorycapacityassumption=35gigawatt‐hoursperyear.

PRIORITYACTION

IEA. All rights reserved.

22 International Energy Agency | Special Report

Clean energy investment in the net zero pathway

Anunparalleledcleanenergyinvestmentboomliftsglobaleconomicgrowth

Total annual energy investment surges to USD 5 trillion by 2030, adding an extra

0.4percentagepointayeartoannualglobalGDPgrowth,basedonourjointanalysiswith

the International Monetary Fund. This unparalleled increase – with investment in clean

energy and energy infrastructure morethantriplingalreadyby2030 – brings significant

economicbenefitsastheworldemergesfromtheCovid‐19crisis.Thejumpinprivateand

governmentspendingcreatesmillionsofjobsincleanenergy,includingenergyefficiency,as

wellasintheengineering,manufacturingandconstructionindustries.Allofthisputsglobal

GDP4%higherin2030thanitwouldbebasedoncurrenttrends.

Governments have a key role in enabling investment‐led growth and ensuring that the

benefitsaresharedbyall.Therearelargedifferencesinmacroeconomicimpactsbetween

regions. But government investment and public policies are essential to attract large

amountsofprivatecapitalandtohelpoffsetthedeclinesinfossilfuelincomethatmany

countrieswillexperience.Themajorinnovationeffortsneededtobringnewcleanenergy

technologies to market could boost productivity and create entirely new industries,

providingopportunitiestolocatetheminareasthatseejoblossesinincumbentindustries.

Improvementsinairqualityprovidemajorhealthbenefits,with2millionfewerpremature

deathsglobally fromairpollution in2030 than todayinour netzeropathway.Achieving

universalenergyaccessby2030wouldprovideamajorboosttowell‐beingandproductivity

indevelopingeconomies.

1

2

3

4

5

2016‐20 2030 2050

TrillionUSD(2019)

End‐use

Energyinfrastructure

Electricitygeneration

Low‐emissionsfuels

Summary for policy makers 23

Newenergysecurityconcernsemerge,andoldonesremain

Thecontractionofoilandnaturalgasproductionwillhavefar‐reachingimplicationsforall

thecountriesandcompaniesthatproducethesefuels.Nonewoilandnaturalgasfieldsare

neededinourpathway,andoilandnaturalgassuppliesbecomeincreasinglyconcentrated

inasmallnumberoflow‐costproducers.Foroil,theOPECshareofamuch‐reducedglobal

oilsupplyincreasesfromaround37%inrecentyearsto52%in2050,alevelhigherthanat

anypointinthehistoryofoilmarkets.Yetannualpercapitaincomefromoilandnaturalgas

inproducereconomiesfallsbyabout75%,fromUSD1800inrecentyearstoUSD450bythe

2030s,whichcouldhaveknock‐onsocietaleffects.Structuralreformsandnewsourcesof

revenueareneeded,eventhoughtheseareunlikelytocompensatefullyforthedropinoil

andgasincome.Whiletraditionalsupplyactivitiesdecline,theexpertiseoftheoilandnatural

gasindustryfitswellwithtechnologiessuchashydrogen,CCUSandoffshorewindthatare

neededtotackleemissionsinsectorswherereductionsarelikelytobemostchallenging.

Theenergytransitionrequiressubstantialquantitiesofcriticalminerals,andtheirsupply

emergesasasignificantgrowtharea.Thetotalmarketsizeofcriticalmineralslikecopper,

cobalt,manganeseandvariousrareearthmetalsgrowsalmostsevenfoldbetween2020and

2030inthenetzeropathway.Revenuesfromthosemineralsarelargerthanrevenuesfrom

coalwellbefore2030.Thiscreatessubstantialnewopportunitiesforminingcompanies.It

alsocreatesnewenergysecurityconcerns,includingpricevolatilityandadditionalcostsfor

transitions,ifsupplycannotkeepupwithburgeoningdemand.

The rapid electrification of all sectors makes electricity even more central to energy

securityaroundtheworldthanitistoday.Electricitysystemflexibility–neededtobalance

windandsolarwithevolvingdemandpatterns–quadruplesby2050evenasretirementsof

fossilfuelcapacityreduceconventionalsourcesofflexibility.Thetransitioncallsformajor

increases in all sources of flexibility: batteries, demand response and low‐carbonflexible

powerplants,supportedbysmarterandmoredigitalelectricitynetworks.Theresilienceof

electricitysystemstocyberattacksandotheremergingthreatsneedstobeenhanced.

Address emerging energy security risks now

Ensuring uninterrupted and reliable supplies of energy and critical energy‐related

commoditiesataffordablepriceswillonlyriseinimportanceonthewaytonetzero.

Thefocusofenergysecuritywillevolveasrelianceonrenewableelectricitygrowsand

the role of oil and gas diminishes. Potential vulnerabilities from the increasing

importance of electricity include the variability of supply andcybersecurityrisks.

Governmentsneedtocreatemarketsforinvestmentinbatteries,digitalsolutionsand

electricity grids that reward flexibility and enable adequate and reliable supplies of

electricity.Thegrowingdependenceoncriticalmineralsrequiredforkeycleanenergy

technologies calls for new international mechanisms to ensure both the timely

PRIORITYACTION

IEA. All rights reserved.

24 International Energy Agency | Special Report

availabilityofsuppliesandsustainableproduction.Atthesametime,traditionalenergy

securityconcernswillnotdisappear,asoilproductionwillbecomemoreconcentrated.

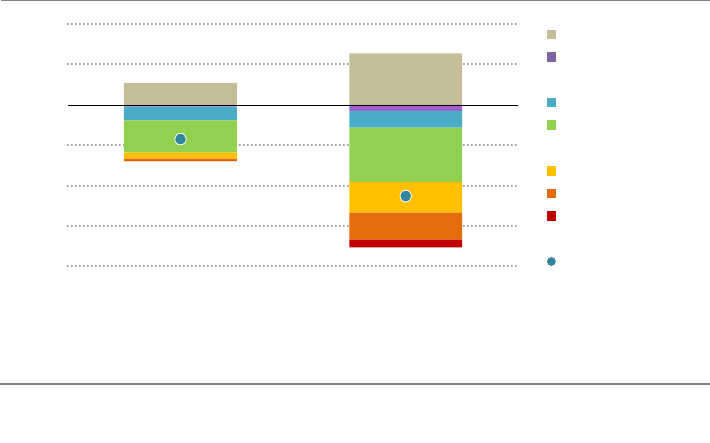

Global energy security indicators in the net zero pathway

Note:mb/d=millionbarrelsperday;Mt=milliontonnes.

Internationalco‐operationispivotalforachievingnet‐zeroemissionsby2050

Making net‐zero emissions a reality hinges on a singular, unwavering focus from all

governments – working togetherwith one another, and with businesses, investors and

citizens.Allstakeholdersneedtoplaytheirpart.Thewide‐rangingmeasures adopted by

governmentsatalllevelsinthenetzeropathwayhelptoframe,influenceandincentivise

the purchase by consumers and investment by businesses. This includes how energy

companiesinvestinnewwaysofproducingandsupplyingenergyservices,howbusinesses

investinequipment,andhowconsumerscoolandheattheirhomes,powertheirdevicesand

travel.

Underpinningallthesechangesarepolicydecisionsmadebygovernments.Devisingcost‐

effectivenationalandregionalnetzeroroadmapsdemandsco‐operationamongallpartsof

governmentthatbreaksdownsilosandintegratesenergyintoeverycountry’spolicymaking

onfinance,labour,taxation,transportandindustry.Energyorenvironmentministriesalone

cannotcarryoutthepolicyactionsneededtoreachnetzeroby2050.

Changesinenergyconsumptionresultinasignificantdeclineinfossilfueltaxrevenues.In

manycountriestoday, taxes ondiesel,gasolineand other fossilfuelconsumptionarean

importantsourceofpublicrevenues,providingasmuchas10%insomecases.Inthenetzero

pathway,taxrevenuefromoilandgasretailsalesfallsbyabout40%between2020and2030.

Managingthisdeclinewillrequirelong‐termfiscalplanningandbudgetreforms.

10

20

30

40

50

2020 2050

20%

40%

60%

80%

100%

2020 2050

20

40

60

80

100

2020 2050

Oilsupply

(mb/d)

Shareofsolar PVandwind

inelectricitygeneration

Criticalmineralsdemand

(Mt)

52%

OPECshare

34%

Summary for policy makers 25

The net zero pathway relies on unprecedented international co‐operation among

governments,especiallyon innovationandinvestment.TheIEAstandsreadyto support

governmentsinpreparingnationalandregionalnetzeroroadmaps,toprovideguidanceand

assistanceinimplementingthem,andtopromoteinternationalco‐operationtoaccelerate

theenergytransitionworldwide.

Take international co-operation to new heights

Thisisnotsimplyamatterofallgovernmentsseekingtobringtheirnationalemissions

tonetzero–itmeanstacklingglobalchallengesthroughco‐ordinatedactions.

Governmentsmustworktogetherinaneffectiveandmutuallybeneficial manner to

implement coherent measures that cross borders. This includes carefully managing

domesticjobcreationandlocalcommercialadvantageswiththecollectiveglobalneed

for clean energy technology deployment. Accelerating innovation, developing

international standards and co‐ordinating to scale up clean technologies needs to be

doneinawaythatlinksnationalmarkets.Co‐operationmustrecognisedifferencesinthe

stagesofdevelopmentofdifferentcountriesandthevaryingsituationsofdifferentparts

ofsociety.Formanyrichcountries,achievingnet‐zeroemissionswillbemoredifficult

and costly without international co‐operation. For many developing countries, the

pathwaytonetzerowithoutinternationalassistanceisnotclear.Technicalandfinancial

supportisneededtoensuredeploymentofkeytechnologiesandinfrastructure.Without

greaterinternationalco‐operation,globalCO

2

emissionswillnotfalltonetzeroby2050.

Global energy-related CO

2

emissions in the net zero pathway and

Low International Co-operation Case

Note:Gt=gigatonnes.

10

20

30

40

2010 2030 2050 2070 2090

GtCO

2

NZE

LowInternationalCooperation Case

PRIORITYACTION

IEA. All rights reserved.

Net Zero Emissions by 2050 Interactive iea.li/nzeroadmap

2035

2020

2030

Industry

Other

Power

Transport

Unabated coal, natural gas

and oil account for over 60%

of total electricity generation

Solar PV and wind

accounts for almost

10% of total electricity

generation

Retroit rates below

1% globally

Fossil fuels account for

almost 80% of TES

40 Mt CO

2

captured

5% of global car

sales are electric

33.9

Total CO

2

emissions (Gt)

Buildings

2.9Gt

8.5Gt

1.9Gt

13.5Gt

7.2Gt

From 2021:

No new oil and gas

ields approved for

development;

no new coal mines

or mine extensions

From 2021:

No new unabated

coal plants approved

for development

Most new clean

technologies in heavy

industry demonstrated

at scale

60% of global car

sales are electric

150 Mt low-carbon

hydrogen; 850 GW

electrolysers

All new buildings are

zero-carbon-ready

Universal

energy access

1 020 GW annual

solar and wind

additions

Phase-out of unabated coal

in advanced economies

Industry

Other

Power

Transport

Buildings

1.8Gt

6.9Gt

0.9Gt

5.8Gt

5.7Gt

21.1

Total CO

2

emissions (Gt)

All industrial electric

motor sales are

best in class

Virtually all heavy industry

capacity additions are

innovative low-emissions

routes

No new internal

combustion

engine car sales

50% of heavy truck

sales are electric

4 Gt CO

2

captured

Overall net-zero emissions

electricity in advanced

economies

Most appliances and

cooling systems sold

are best in class

Capacity itted with

CCUS or co-iring

hydrogen-based

fuels reaches 6% of

total generation

Industry

Other

Power

Transport

Buildings

1.2Gt

5.2Gt

0.1Gt

2.1Gt

4.1Gt

12.8

Total CO

2

emissions (Gt)

2040

2050

Net Zero Emissions by 2050 Interactive iea.li/nzeroadmap

50% of existing

buildings retroitted to

zero-carbon-ready levels

Around 90% of

existing capacity in

heavy industries reaches

end of investment cycle

50% of fuels used

in aviation are

low-emissions

Oil demand is 50%

of 2020 level

Net-zero emissions

electricity globally

Phase-out of all

unabated coal and

oil power plants

Electrolyser capacity

reaches 2 400 GW

Industry

Other

Power

Transport

Buildings

0.7Gt

3.5Gt

-0.5Gt

-0.1Gt

2.7Gt

6.3

Total CO

2

emissions (Gt)

33.9

Total CO

2

emissions (Gt)

More than 90% of heavy

industrial production

is low-emissions

More than 85%

of buildings are

zero-carbon-ready

7.6 Gt CO

2

captured

Renewables reach

almost 90% of total

electricity generation

Almost 70% of

electricity generation

globally from solar PV

and wind

520 Mt

low-carbon

hydrogen

Industry

Other

Power

Transport

Buildings

0.1Gt

0.5Gt

-1Gt

-0.4Gt

0.7Gt

0

Total CO

2

emissions (Gt)

IEA. All rights reserved.

Chapter 1 | Announced net zero pledges and the energy sector 29

Chapter1

Announced net zero pledges and the energy sector

Therehasbeena rapid increaseoverthelastyearin thenumber of governments

pledgingtoreducegreenhousegasemissionstonetzero.Netzeropledgestodate

coveraround70%ofglobalGDPandCO

2

emissions.However,fewerthanaquarter

of announced net zero pledges are fixed in domestic legislation and few are yet

underpinnedbyspecificmeasuresorpoliciestodelivertheminfullandontime.

TheStatedPoliciesScenario(STEPS)takesaccountonlyofspecificpoliciesthatarein

placeorhavebeenannouncedbygovernments.Annualenergy‐relatedandindustrial

processCO

2

emissionsrisefrom34Gtin2020to36Gtin2030andremainaround

thisleveluntil2050.Ifemissionscontinueonthistrajectory,withsimilarchangesin

non‐energy‐relatedGHGemissions,thiswouldleadtoatemperatureriseofaround

2.7°Cby2100(witha50%probability). Renewablesprovide almost 55%ofglobal

electricitygenerationin2050(upfrom29%in2020),butcleanenergytransitionslag

inothersectors.Globalcoalusefallsby15%between2020and2050;oilusein2050

is15%higherthanin2020;andnaturalgasuseisalmost50%higher.

The Announced Pledges Case (APC) assumes that all announced national net zero

pledges are achieved in full and on time, whether or not they are currently

underpinned by specific policies. Global energy‐related and industrial process CO

2

emissions fall to 30Gt in 2030 and 22Gt in 2050. Extending thistrajectory,with

similaractiononnon‐energy‐relatedGHGemissions,wouldleadtoatemperaturerise

in2100ofaround2.1°C(witha50%probability).Globalelectricitygenerationnearly

doubles to exceed 50000TWh in 2050. The share of renewables in electricity

generationrisestonearly70%in2050.Oildemanddoesnotreturntoits2019peak

and falls about 10% from 2020 to 80mb/d in 2050. Coal use drops by 50% to

2600Mtcein2050,whilenaturalgasuseexpandsby10%to4350bcmin2025and

remainsaboutthatlevelto2050.

Efficiency, electrification and the replacement of coal by low‐emissions sources in

electricity generation play a central role in achieving net zerogoalsintheAPC,

especiallyovertheperiodto2030.Therelativecontributionsofnuclear,hydrogen,

bioenergyandCCUSvaryacrosscountries,dependingontheircircumstances.

ThedivergenceintrendsbetweentheAPCandtheSTEPSshowsthedifferencethat

currentnetzeropledgescouldmake,whileunderliningatthesametimetheneedfor

concretepoliciesandshort‐termplansthat areconsistentwithlong‐termnetzero

pledges.However,theAPCalsostarklyhighlightsthatexistingnetzeropledges,even

ifdeliveredinfull,fallwellshortofwhatisnecessarytoreach global net‐zero

emissionsby2050.

SUMMARY

IEA. All rights reserved.

30 International Energy Agency | Special Report

1.1 Introduction

November2021willseethemostimportantUNFrameworkConventiononClimateChange

(UNFCCC)ConferenceoftheParties(COP26)sincetheParisAgreementwassignedin2015.

AsCOP26approaches,anincreasingnumberofcountrieshaveannouncedlong‐termgoals

to achieve net‐zero greenhouse gas (GHG) emissions over the coming decades. On

31March2021, the International Energy Agency(IEA) hosted a Net Zero Summit to take

stockofthegrowinglistofcommitmentsfromcountriesandcompaniestoreachthegoals

oftheParisAgreement,andtofocusontheactionsnecessarytostartturningthosenetzero

goalsintoreality.

Achievingthosegoalswillbedemanding.TheCovid‐19pandemicdeliveredamajorshockto

theworldeconomy,resultinginanunprecedented5.8%declineinCO

2

emissionsin2020.

However,ourmonthlydatashowthatglobalenergy‐relatedCO

2

emissionsstartedtoclimb

againinDecember2020,andweestimatethattheywillreboundtoaround33gigatonnesof

carbondioxide(GtCO

2

)in2021,only1.2%belowthelevelin2019(IEA,2021).Sustainable

economicrecoverypackages

offeredauniqueopportunitytomake2019thedefinitivepeak

inglobalemissions,buttheevidencesofarpointstoareboundinemissionsinparallelwith

renewedeconomicgrowth,atleastinthenearterm(IEA,2020a).

RecentIEAanalysesexaminedthetechnologiesandpoliciesneededforcountriesand

regions to achieve net‐zero emissions energy systems. The World Energy Outlook 2020

examinedwhatwouldbeneededovertheperiodto2030toputtheworldonapathtowards

net‐zero emissions by 2050 in the context of the pandemic‐related economic recovery

(IEA,2020b).TheFasterInnovationCaseinEnergyTechnologyPerspectives2020explored

whethernet‐zeroemissionscouldbeachievedgloballyby2050throughacceleratedenergy

technologydevelopmentanddeploymentalone:itshowedthat,relativetobaselinetrends,

almost half of the emissions savings needed in 2050 to reach net‐zero emissions rely on

technologiesthatarenotyetcommerciallyavailable(IEA,2020c).

Thisspecialreport,preparedattherequestoftheUKPresidentoftheCOP26,incorporates

theinsightsandlessonslearnedfrombothreportstocreateacomprehensiveanddetailed

pathway, or roadmap, to achieve net‐zero energy‐related and industrial process CO

2

emissionsgloballyby2050.Itassessesthecostsofachievingthisgoal,thelikelyimpactson

employmentandtheeconomy,andthewiderimplicationsfortheworld.Italsohighlights

thekeymilestonesfortechnologies,infrastructure,investmentandpolicythatareneeded

alongtheroadto2050.

Thisreportissetoutinfourchapters:

Chapter 1 explores the outlook for global CO

2

emissions and energy supply and use

basedonexistingpoliciesandpledges.Itsetsoutprojectionsofglobalenergyuseand

emissionsbasedontheStatedPoliciesScenario(STEPS),whichincludesonlythefirm

policies that are in placeor havebeen announced bycountries, including Nationally

Chapter 1 | Announced net zero pledges and the energy sector 31

1

Determined Contributions. It also examines the Announced Pledges Case (APC), a

variantoftheSTEPSthatassumesthatallofthenetzerotargetsannouncedbycountries

aroundtheworldtodatearemetinfull.

Chapter2presentstheNet‐ZeroEmissionsby2050Scenario(NZE),whichdescribes

howenergydemandandtheenergymixwillneedtoevolveiftheworldistoachieve

net‐zeroemissionsby2050.Italsoassessesthecorrespondinginvestmentneedsand

exploreskeyuncertaintiessurroundingtechnologyandconsumerbehaviour.

Chapter3examinestheimplicationsoftheNZEforvarioussectors,coveringfossilfuel

supply, the supply of low‐emissions fuels (such as hydrogen, ammonia, biofuels,

syntheticfuelsandbiomethane)andtheelectricity,transport,industryandbuildings

sectors.Ithighlightsthekeychangesrequiredtoachievenet‐zeroemissionsintheNZE

andthemajormilestonesthatareneededalongtheway.

Chapter4explorestheimplicationsoftheNZEfortheeconomy,theenergyindustry,

citizensandgovernments.

1.2 Emissionsreductiontargetsandnetzeropledges

1.2.1 NationallyDeterminedContributions

Under the Paris Agreement, Parties

1

are required to submit Nationally Determined

Contributions(NDCs)totheUNFCCCandtoimplementpolicieswiththeaimofachieving

theirstatedobjectives.Theprocessisdynamic;itrequiresPartiestoupdatetheirNDCsevery

fiveyearsinaprogressivemannertoreflectthehighestpossibleambition.Thefirstroundof

NDCs, submitted by 191countries, covers more than 90% of global energy‐related and

industrial process CO

2

emissions.

2

The first NDCs included some targets that were

unconditional and others that were conditional on international support for finance,

technologyandothermeansofimplementation.

As of 23 April 2021, 80countries have submitted new or updatedNDCstotheUNFCCC,

coveringjustover40%ofglobalCO

2

emissions (Figure1.1).

3

Many of the updated NDCs

include more stringent targets than in the initial round of NDCs, or targets for a larger

number of sectors or for a broader coverage of GHGs. In addition, 27countries and the

EuropeanUnionhavecommunicatedlong‐termlowGHGemissionsdevelopmentstrategies

totheUNFCCC,asrequestedbytheParisAgreement.Someofthesestrategiesincorporate

anetzeropledge.

1

Partiesreferstothe197membersoftheUNFCCCwhichincludesallUnitedNationsmemberstates,United

NationsGeneralAssemblyObserverStateofPalestine,UNnon‐memberstatesNiueandtheCookIslandsand

theEuropeanUnion.

2

Unless otherwise stated, CO

2

emissions in this report refer to energy‐related and industrial process CO

2

emissions.

3

SeveralcountrieshaveindicatedthattheyintendtosubmitneworupdatedNDCslaterin2021orin2022.

IEA. All rights reserved.

32 International Energy Agency | Special Report

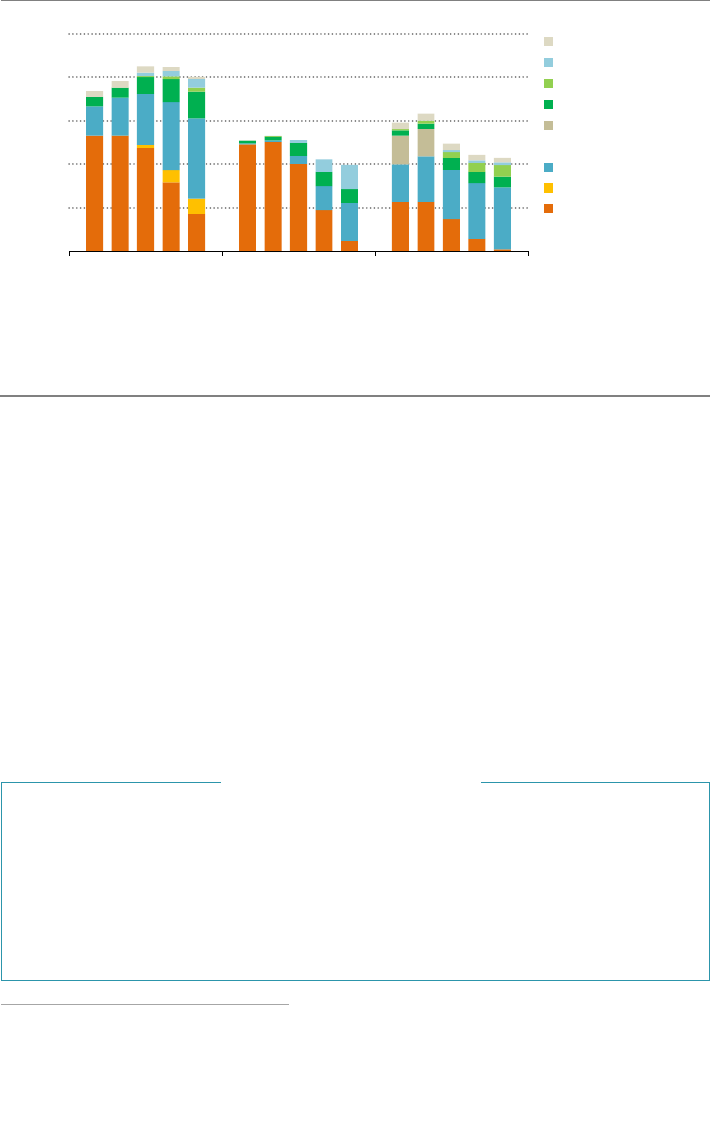

Figure 1.1 ⊳ Number of countries with NDCs, long-term strategies and net

zero pledges, and their shares of 2020 global CO

2

emissions

IEA.Allrightsreserved.

Around 40% of countries that have ratified the Paris Agreement have updated their NDCs,

but net zero pledges cover around 70% of global CO

2

emissions

1.2.2 Net‐zeroemissionspledges

Therehasbeenarapidincreaseinthenumberofgovernmentsmakingpledgestoreduce

GHGemissionstonetzero(Figure1.2).IntheParisAgreement,countriesagreedto“achieve

abalancebetweenanthropogenicemissionsbysourcesandremovalsbysinksofgreenhouse

gasesinthesecond‐halfofthecentury”.TheIntergovernmentalPanelonClimateChange

(IPCC)SpecialReport onGlobalWarming of1.5°Chighlightedtheimportanceofreaching

net‐zero CO

2

emissions globally by mid‐century or sooner to avoid the worstimpactsof

climatechange(IPCC,2018).

Net‐zeroemissionspledgeshavebeen announced by national governments, subnational

jurisdictions, coalitions

4

and a large number of corporate entities (see Spotlight). As of

23April2021, 44countries and the European Union have pledged to meet a net‐zero

emissions target:in total they account for around 70% of global CO

2

emissions and GDP

(Figure1.3). Of these, ten countries have made meeting their net zero target a legal

obligation,eightareproposingtomakeitalegalobligation,andtheremainderhavemade

theirpledgesinofficialpolicydocuments.

4

Examplesinclude:theUN‐ledClimateAmbitionAllianceinwhichsignatoriessignaltheyareworkingtowards

achievingnet‐zeroemissionsby2050;andtheCarbonNeutralityCoalitionlaunchedattheUNClimateSummit

in2017,inwhichsignatoriescommittodeveloplong‐termlowGHGemissionsstrategiesinlinewithlimiting

temperaturerisesto1.5°C.

25%

50%

75%

100%

50

100

150

200

First

NDC

Neworupdated

NDC

NZEpledges Long‐term

strategy

NZEtargetsin

law

Numberofcountries

Shareofglobal2020CO₂emissions(rightaxis)

Chapter 1 | Announced net zero pledges and the energy sector 33

1

Figure 1.2 ⊳ Number of national net zero pledges and share of global CO

2

emissions covered

IEA.Allrightsreserved.

There has been a significant acceleration in net-zero emissions pledges

announced by governments, with an increasing number enshrined in law

Notes:Inlaw=anetzeropledgehasbeenapprovedbyparliamentandislegallybinding.Proposed=anet

zeropledgehasbeenproposedtoparliamenttobevotedintolaw.Inpolicydocument=anetzeropledgehas

beenproposedbutdoesnothavelegallybindingstatus.

Figure 1.3 ⊳ Coverage of announced national net zero pledges

IEA.Allrightsreserved.

Countries accounting for around 70% of global CO

2

emissions and GDP have set net zero

pledges in law, or proposed legislation or in an official policy document

Note:GDP=grossdomesticproductatpurchasingpowerparity.

20%

40%

60%

80%

100%

10

20

30

40

50

2015 2016 2017 2018 2019 2020 2021

Q1

ShareofCO₂emissions

Countrieswithpledges

Inlaw Proposed Inpolicydocuments GlobalCO₂covered(rightaxis)

20% 40% 60% 80% 100%

GDP

CO₂emissions

Population

Countries

Advancedeconomies Emergingmarketanddevelopingeconomies Notcovered

IEA. All rights reserved.

34 International Energy Agency | Special Report

IncontrasttosomeoftheshortertermcommitmentscontainedwithinNDCs,fewnetzero

pledges are supported by detailed policies and firm routes to implementation. Net‐zero

emissionspledgesalsovaryconsiderablyintheirtimescaleandscope.Somekeydifferences

include:

GHGcoverage.MostpledgescoverallGHGemissions,butsomeincludeexemptionsor

differentrulesforcertaintypesofemissions.Forexample,New Zealand’s net zero

pledgecoversallGHGsexceptbiogenicmethane,whichhasaseparatereductiontarget.

Sectoralboundaries.Somepledgesexcludeemissionsfromspecificsectorsoractivities.

For example, the Netherlands aims to achieve net‐zero GHG emissions only in its

electricitysector(aspartofanoverallaimtoreducetotalGHGemissionsby95%),and

somecountries,includingFrance,PortugalandSweden,excludeinternationalaviation

andshipping.

Useofcarbondioxideremoval(CDR).Pledgestakevaryingapproachestoaccountfor

CDRwithinacountry’ssovereignterritory.CDRoptionsincludenaturalCO

2

sinks,such

as forests and soils, as well as technological solutions, such as direct air capture or

bioenergy with carbon capture and storage. For example, Uruguayhasstatedthat

naturalCO

2

sinkswillbeusedtohelpitreachnet‐zeroemissions,whileSwitzerlandplans

touseCDRtechnologiestobalanceapartofitsresidualemissionsin2050.

Use of international mitigation transfers.SomepledgesallowGHGmitigationthat

occursoutsideacountry’sborderstobecountedtowardsthenetzerotarget,suchas

throughthetransferofcarboncredits,whileothersdonot.Forexample,Norwayallows

thepotentialuseofinternationaltransfers,whileFranceexplicitlyrulesthemout.Some

countries,suchasSweden,allowsuchtransfersbutspecifyanupperlimittotheiruse.

Timeframe.Themajorityofpledges,covering35%ofglobalCO

2

emissions in 2020,

targetnet‐zeroemissionsby2050,butFinlandaimstoreachthatgoalby2035,Austria

andIcelandby2040andSwedenby2045.Amongothers,thePeople’sRepublicofChina

(hereafterChina)andUkrainehavesetatargetdateafter2050.

How are businesses responding to the need

to reach net-zero emissions?

Therehasbeenarapid rise in net‐zero emissionsannouncements from companiesin

recentyears:asofFebruary2021,around110companiesthatconsumelargeamounts

of energy directly or produce energy‐consuming goods have announced net‐zero

emissionsgoalsortargets.

Around60‐70%ofglobalproductionofheatingandcoolingequipment,roadvehicles,

electricity and cement is from companies that have announced net‐zero emissions

targets (Figure1.4). Nearly 60% of gross revenue in the technology sector is also

generated by companies with net‐zeroemissiontargets.Inother sectors, net zero

SPOTLIGHT

Chapter 1 | Announced net zero pledges and the energy sector 35

1

pledgescover30‐40%ofairandshippingoperations,15%oftransportlogisticsand10%

of construction.

Allthese shares are likely to keepgrowingasmorecompaniesmake

pledges.

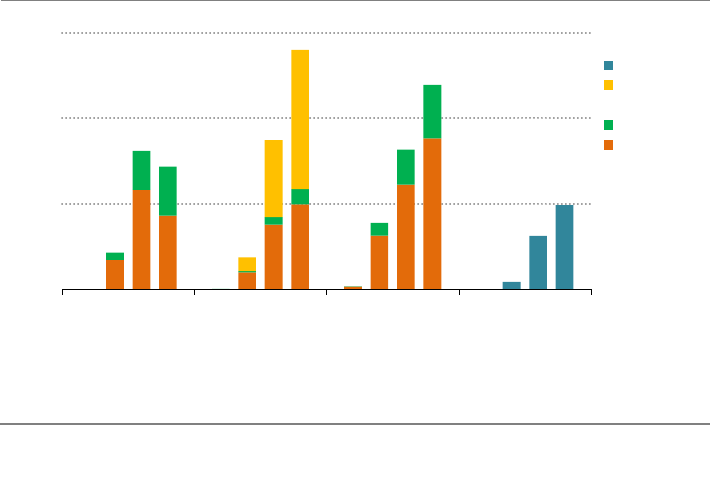

Figure 1.4 ⊳ Sectoral activity of large energy-related companies with

announced pledges to reach net-zero emissions by 2050

IEA.Allrightsreserved.

Some sectors are more advanced in terms of the extent

of net zero targets by companies active in the sector

Notes:Scope1=directemissionsfromenergyandothersourcesownedorcontrolled.Scope2=indirect

emissionsfromtheproductionofelectricityandheat,andfuelspurchasedandused.Scope3=indirect

emissionsfromsourcesnotownedordirectlycontrolledbutrelatedtotheiractivities(suchasemployee

travel, extraction, transport and production of purchased materials and fuels, and end‐use of fuels,

productsandservices).PartialvaluechainincludesScope1and2emissionsandScope3emissionsin

specificgeographiclocationsorsectionsofacompany’svaluechain.

Source:IEAanalysisbasedoncompanyreportsfromthelargest10‐25companieswithineachsector.

Companypledgesmaynotbereadilycomparable.Mostcompaniesaccountforemissions

andsetnetzeropledgesbasedontheGHGProtocol(WRI,WBCSD, 2004), but the

coverageandtimeframeofthesepledgesvarieswidely.Somecover only their own

emissions,forexamplebyshiftingtotheuseofzero‐emissionselectricityinofficesand

production facilities, and by eliminating the use of oil in transport or industrial

operations,e.g.FedEx,ArcelorMittalandMaersk.Othersalsocoverwideremissionsfrom

certain parts of their values chains, e.g. Renault in Europe, or all indirect emissions

relatedtotheiractivities,e.g.Daikin,Toyota,Shell,EniandHeidelberg.Around60%of