Office Of ReseaRch and educatiOn accOuntability

hOw Much tennessee Public schOOls

sPend PeR student

MaRch 2021

JasOn e. MuMPOweR

Comptroller of the Treasury

taRa beRgfeld

Principal Legislative Research Analyst

KiM POtts

Principal Legislative Research Analyst

2

Overview

In late June 2020, the Tennessee Department of Education (TDOE or the department) published data

showing per-pupil expenditures for every public school in the state for school year 2018-19. To provide

some context to the amount of per-pupil spending shown for each school, OREA has released an interactive

dashboard of per-pupil spending and demographic data for all K-12 public schools and districts.

is report describes the department’s methodology

in calculating the per-pupil gures at both the school

and district level. It also explains briey how school

districts are funded in Tennessee and how, in turn,

school districts allocate funds to their schools. e report

examines Tennessee’s data and discusses factors that are

important for the General Assembly and other education

stakeholders to consider regarding the per-pupil gures,

particularly when comparing schools.

Federal education law requires states to report

per-pupil spending by school

Under a provision in the federal education law, the Every Student Succeeds Act (ESSA),

A

passed into law

in 2015, the annual State Report Card for public schools must include:

e per-pupil expenditures of Federal, State, and local funds, including actual personnel expenditures

and actual non-personnel expenditures of Federal, State, and local funds, disaggregated by source of

funds, for each local educational agency and each school in the State for the preceding scal year.

1

ough states had long reported per-pupil

expenditures by district, reporting these gures by

school was a new requirement. Because most school

districts’ accounting systems had not been designed

to report spending at the school level, states needed

time to develop the ability to comply with this

requirement. e U.S. Department of Education

granted states additional time to reach compliance

also because the 2016 federal ESSA regulations,

which addressed the per-pupil expenditure reporting

requirement for state report cards and detailed

the expenditures to include and exclude from the

calculations, were disapproved by Congress in a 2017

resolution also signed by the President. Because of

this, states were limited to using only the statutory

language to determine how to proceed.

2

Following the disapproval of the regulations, in 2017, the U.S. Department of Education directed states to its

contracted education support agencies for assistance.

3

States could collaborate with other states through the

Edunomics Lab at Georgetown University “on operationalizing the broad ESSA provision and making

A

e federal Every Student Succeeds Act (ESSA), signed into law December 2015, is the most recent version of the Elementary and Secondary Education Act of

1965. ESSA replaces the No Child Left Behind Act of 2001 (NCLB), the previous version of the 1965 education law.

OREA interactive dashboard with all Tennessee

schools’ per-pupil expenditure information

OREA’s dashboard allows users to view the 2018-

19 school year per-pupil expenditure gures for all

Tennessee school districts and K-12 public schools.

An interactive map allows users to view a breakdown of

2018-19 average district level per-pupil expenditures.

Report card calculations: the data used for

calculating per-pupil expenditures makes a dierence

States have long reported and published district level

per-pupil expenditure gures but because these included

such items as state level program and administrative

costs, among others, the resulting gures did not

represent actual district level expenditures.

The previous formula took total district operating

expenditures (excluding student body education and

adult education), USDA commodity values (school

nutrition), and state level program and administrative

costs, and divided that gure by average daily

attendance (ADA).

The updated per-pupil gure required by ESSA no

longer includes state level administrative costs. It also

uses enrollment on October 1 as the denominator in the

calculation instead of ADA.

3

the school-level nancial data meaningful across states.”

4

Tennessee is a member of a network of states and

school districts facilitated by Edunomics called the Financial Transparency Working Group (FiTWiG).

B

is collective network developed Interstate Financial Reporting, “a set of voluntary, minimal reporting

criteria that states could voluntarily use to make valid, apples-to-apples comparisons of school-level per-pupil

expenditures across states.”

5

Tennessee developed a formula for calculating

school-level per-pupil expenditures

To establish a per-pupil expenditure at the school level, in basic terms, each school’s expenditures would be

added together along with any district-wide (or shared expenditures), and the resulting total would then be

divided by the number of students enrolled in the school as of October 1. According to ESSA, the calculation

must include funds from federal, state, and local sources, and these must be disaggregated by source in the

gures reported. (See “A short explanation of how K-12 public schools in Tennessee are funded” on page 5.)

To develop its formula, Tennessee had to decide the details of which standard expenditures to include (for

example, how to divide and assign central or shared expenditures, such as transportation, to schools,), as

well as what to exclude to make the gures comparable and useful across the state. Tennessee followed the

voluntary Interstate Financial Reporting criteria, as did most participating states, according to Edunomics.

6

In 2018, TDOE created the Tennessee Financial Transparency Working Group, modeled after the national

Financial Transparency Working Group (FiTWiG), of which the state is a member, to compile input from

stakeholders (i.e., districts) on what expenditures to include at the school level versus district level and how to

collect and present data.

7

TDOE gathered input through a pilot project that included the participation of 13

Tennessee school districts using FY2017 expenditures to help create a draft formula for determining school-

versus district-level expenditures.

8,C

Tennessee’s nal formula designates certain expenditures that can be distinguished at the school level, such as

salaries and benets for those working at least 50 percent of their time in a school, instructional supplies and

materials, utilities, and school nutrition.

9

All other expenditures are considered district level. To obtain a per-

pupil gure, the total school-level and district-level expenditures are each divided by the student membership

gure as of October 1 of the school year.

10

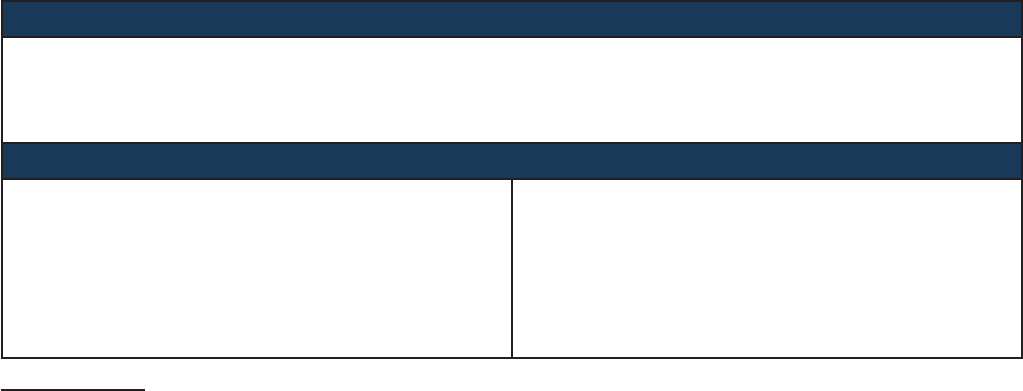

Exhibit 1: School-level expenditures

Source: Tennessee Department of Education.

B

At the time of the 2018 IFR report, FiTWiG comprised 39 states and more than 20 school districts throughout the U.S.

C

Anderson County, Bartlett City, Clinton City, Greeneville City, Hardin County, Johnson City, Madison County, Manchester City, Millington City, Rutherford

County, Sevier County, Shelby County, and Williamson County school districts participated in the pilot program with TDOE.

Expenditure categories

• Salaries

• Benets and retirement

• Instructional supplies and materials

• Utilities

Accounts

• Regular instruction program

• Alternative instruction program

• Special education program

• Vocational education program

• Attendance

• Health services

• Other student support

• Support services/regular instruction program

• Support Services/Alternative Instruction Program

• Support Services/Special Education Program

• Support Services/Vocational Education Program

• Oce of the Principal

• Food Service

4

Exhibit 2: Tennessee’s per-pupil expenditure formula

e per-pupil gures do not include the following types of expenditures:

• student body education – learning experiences including school sponsored co-curricular activities such as

band, choir, speech, etc., student-nanced and managed activities (e.g., class of 20xx) and club accounts,

and school sponsored athletic activities;

• instruction and support services for adult education – programs include activities that prepare adult

students for a job or postsecondary education (e.g., community college or certicate program), upgrade

occupational competence, etc.;

• noninstructional expenditures for early childhood and community service (e.g., expenditures for system

sta participating in community organizations such as leadership, family resource centers, Families First,

Pre-K programs, extended school programs, and community-sponsored activities);

• regular capital outlay – site acquisition services, site improvement services, architecture and engineering

services, etc.;

• debt service – expenditures for servicing long-term debt (obligations exceeding one year);

• transfers – transfers to other funds such as debt service or indirect cost payments;

• capital projects – expenditures related to constructing, remodeling, and equipping buildings where long-

term debt is usually involved in nancing the activity; and

• private purpose trust – funds dedicated for a specic purpose. In some cases, districts may use only the

interest earned on the principal investment.

11

In addition, private funds from organizations aliated with schools (e.g., parent-teacher associations, booster

clubs) are not included in either the school- or district-level gures.

OREA created two tools to view the per-pupil

expenditure data

OREA developed two tools for public analysis of the 2018-19 school-level per-pupil gures.

First, an interactive dashboard allows a user to select a school district and view both district- and school-level

nancial and demographic information. Users can choose to view all schools within a district or select one or

more for comparison. Second, a searchable map of Tennessee displays the average school and district per-pupil

amounts as well as district-level demographic data.

e department plans to add more visualization tools with the per-pupil expenditure data to the State Report

Card. In September 2020, the U.S. Department of Education released an interactive map of the U.S.,

allowing access to each state’s per-pupil spending by school. Some states’ data is not yet viewable on the site,

including Tennessee’s.

School level per pupil

+

District level per pupil

Federal

State and

Local

School

nutrition

Federal

State and

Local

School

nutrition

=

Total school expenditures

÷

Student enrollment

=

Per-pupil expenditure by school

5

A short explanation of how K-12 public schools

in Tennessee are funded

To understand how TDOE and the state’s school districts determined per-pupil expenditures for each school in the state,

a general knowledge of school funding is helpful. Each public school in Tennessee is part of a school district. School

districts receive revenues (or funds) from state, local, and federal sources. This section summarizes how each one of

these three sources aect the funds that each school in the state receives.

State funds are appropriated through the Basic Education Program (BEP), Tennessee’s education funding formula for

K-12 education. In scal year 2018-19, Tennessee’s school districts overall received 48 percent of their public revenues

from state funds, primarily through the BEP.

12

The state’s BEP funding comes from various state taxes dedicated for

education, including portions of the sales tax and cigarette tax, and is supplemented by other state taxes from the

general fund.

The BEP funds school districts – not individual schools – and is often referred to as a funding formula, not a spending

plan. In other words, the BEP formula is used to calculate the state funds that districts receive, based on several

components described below. Almost all of Tennessee’s school districts budget at the district level and report per-pupil

expenditure gures after expenditures are made.

The BEP generates funding through 46 components, which address the dierent costs of operating a school district. The

components are divided among four main categories. All components are driven, in some form, by student enrollment –

generally, the more students in a district, the more BEP money the district receives. Each component is based on a unit

cost (e.g., $48,330 for each teacher’s salary, or $77.50 per textbook).

13

Because the BEP is a funding formula and not a spending plan, there is no requirement that funds be used for or

reported as expenditures for particular students.

Local funds made up about 41 percent of school district’s public revenues in scal year 2018-19.

14

These funds come

primarily from local property taxes or payments in lieu of taxes,

D

local option sales taxes, and – for municipal districts –

appropriations from city general funds.

15

Local funding for education is based largely on two obligations in Tennessee state law: required local match and

maintenance of eort.

The local funding body for the school district must meet its required local match, which obligates local governments

to appropriate a sucient amount of money to fund the local share of the BEP after accounting for the county’s scal

capacity.

16

Many funding bodies for school districts in Tennessee appropriate funds in an amount that is “above and

beyond” the local match requirement: in 2018-19, all but ve districts exceeded the local required match amount.

And the local funding body must annually continue its maintenance of eort, which requires county commissions, city

councils, and special districts to budget at least the same total dollars for schools that they did in the previous year.

17

Federal funds account for a much smaller percentage of districts’ overall budgets than state or local

funds – only 11 percent of Tennessee school districts’ public revenues came from federal funding in FY 2018-19.

18

The amount of federal funding a district receives is often based on the enrollment of certain types of students, such as

students with disabilities and those classied as economically disadvantaged.

Because school districts must report to the U.S. Department of Education how they spend federal funds, it is possible to

isolate federal revenues and expenditures. Additionally, federal education funding is tied to specic students or schools

based on level and type of need, but districts have some discretion in how federal funds are distributed to the schools in

their district. For example, Title I allocates funds to districts with greater numbers and higher concentrations of students in

poverty. As of the 2019-20 school year, all Tennessee school districts receive some Title I funds.

E

Schools identied as Title I may operate either as targeted assistance or schoolwide programs. Targeted assistance

schools identify students who are at risk of not meeting the state’s content and performance standards and provide

individualized instructional programs only to the students identied as needing this assistance to meet the state’s

standards. Schoolwide programs use their funds to improve the entire program of the school, which aects all students.

19

D

In a payment in lieu of taxes (PILOT) agreement, a local government authority takes ownership of a business property, thereby exempting the business property

from property taxes, and leases the property to a business. e business makes payments to the local government in lieu of the property taxes that would have

otherwise been paid absent the PILOT agreement. Businesses benet from PILOT agreements because they pay a percentage of the full amount in property taxes that

would have been owed without the agreement. See https://comptroller.tn.gov/content/dam/cot/orea/advanced-search/2018/2018_OREA_BusIncentReport.pdf.

E

Tennessee Department of Education, 2019 Annual Statistical Report, Table 14, p. 79-81. Carroll County is an exception because it is used only for special education

services for less than a dozen students.

6

School districts use different methods to allocate

education funds to each individual school

Districts in Tennessee have various methods of determining how to allocate funds to their individual schools. One

recurring theme OREA heard in talking to districts about this process was that each school has unique circumstances

that aect its funding needs. One director of schools told OREA that no single factor would ever be the driving force for

his district’s decisions to allocate more or less funding per school. Allocating funds to schools, the director explained, is

not a matter of simply ranking schools by certain student demographic characteristics and using that to determine how to

distribute funding.

One of the most common methods of allocating the combined state and local funds to schools is for the school district’s

central oce to manage and assign sta and resources to individual schools.

20

Some districts that use this centralized

approach to funding schools have developed guides that are similar in approach to the BEP, i.e., a certain number of

teaching assistants, specialists, or other types of sta are funded based on the number of students enrolled in each

school.

21

These guidelines, however, are not rules, and districts generally take each school’s dierences into account

when allocating funding.

Shelby County and Metro Nashville determine each school’s allocation from the district’s state and local funds using

a method called “school-based budgeting,” sometimes referred to as student-based budgeting. Under this allocation

method, the district allocates funding to schools based on a formula, developed by district leaders and school principals,

assigning each school a certain amount of funding based on the needs for certain student populations, such as

students with disabilities, those classied as economically disadvantaged, and/or students who have limited prociency

in English.

22

The school district continues to manage certain budget activities that aect the district as a whole, such

as building construction and maintenance, employee benets, transportation, food services, and many administrative

functions.

Metro Nashville estimates that more than half of the district’s operating budget is sent directly to schools to fund the

school-level budgets created by each school’s leadership team. The remainder of the operating budget is used for district-

wide services like transportation, security, textbooks, building maintenance, and technology services.

23

Shelby County

Schools began the transition to a student-based budgeting model in 2018-19 for some of its schools, and plans to expand

the model to all the district’s schools over time.

24

Under Tennessee law, the director of schools in each school district is responsible for preparing and submitting an annual

budget, in itemized form, to the appropriate funding body for adoption prior to the upcoming school year.

25

Depending on

the type of school district, this would be, for example, the county legislative body or city council.

F

Important to know: The state’s education funding formula, the BEP, funds school districts and not individual

schools. Local funding bodies associated with school districts are required to provide matching local education

funds, which vary according to the scal capacity of the county or municipality. State and local funds for education

are then commingled in the budgeting process and cannot be distinguished from each other when determining

per-pupil spending. Federal funds are also part of the education funding school districts receive – these can be

distinguished from state and local funds because school districts must conrm to the U.S. Department of Education

that they were used for the purposes intended.

26

School districts have exibility when determining how to use BEP funds at the local level. The BEP allocates funding

by category (e.g., Instructional Salaries and Wages, Classroom, etc.) but state law does not require local funding to be

budgeted by BEP category. When districts prepare their budgets, BEP funding from the state and local matching dollars

are commingled and the dollars “lose their identity” in terms of revenue source. District budgets do not identify what

portion of expenditures are paid for with state funds versus local funds. Districts must satisfy some general parameters

for spending state funding by category, and they must budget at least the same amount of overall state and local funds

as they did in the previous year. Except in some select districts that use a school-based budgeting method (e.g., Metro

Nashville and Shelby County), local budgets do not generally include school-level budget breakdowns. Once these

requirements are met, a district’s priorities and spending commitments determine how local and state funds will be spent.

27

Important to know: A school district’s priorities may include a focus on literacy, for example, and so the district may

choose to budget additional positions for reading coaches in certain schools. Another district may prioritize hiring

additional school nurses or new afterschool or enrichment programming.

F

Funding bodies for county school districts are county commissions and for city school districts are city councils. Special school districts are considered their own

funding bodies because they can set a special tax rate with the approval of the General Assembly, giving them more direct responsibility for maintaining local funding

levels than city and county school districts. City and special school districts receive local county funding, but the apportionments of county funds to these districts

are made by the county trustee according to statute and not by county commissions.

7

Spending requirements by category in the Basic

Education Program (BEP) formula

Instructional salaries generate funding for classroom teachers

and other licensed positions, such as principals and librarians.

Funding must be spent on teacher salaries though districts do not

have to spend the money on specic types of teachers. Districts

with an average weighted salary below the state average must

spend all BEP funds generated in the Instructional Salaries and

Wages category on salaries for licensed instructional positions.

Instructional benets cover retirement and health insurance

for classroom teachers and other licensed personnel. Districts

with an average weighted salary above the state average may

use BEP Instructional Salaries and Wages funding on either

salaries or benets.

Classroom includes textbooks, classroom supplies, technology,

and some positions such as nurses and instructional assistants;

State law requires that Classroom category funding only be

spent on Instructional or Classroom items.

Non-classroom includes superintendents, school buses,

maintenance and operations, and capital outlay. Funding

generated in the Non-classroom category may be spent in any

of the BEP’s four categories.

Types of school districts in Tennessee

Local school districts in Tennessee are one of three types: county, municipal, or special.

There are 141 local school districts in the state. Districts vary widely in the number of schools

administered and the number of students served. Unlike school districts in most other states,

most school districts in Tennessee are nancially dependent on another government body,

either a county or a city. (Tennessee’s special school districts are an exception. Unlike county

and municipal districts, special school districts are established by private acts of the state

legislature and must have the legislature’s approval for any tax levy to support operations).

Municipal school districts have additional funding sources that may result in more revenues

for education overall than county school districts. On average, municipal school districts

spent about $600 more per pupil in 2018-19 than county districts. Municipal school districts

typically receive a designated portion of city tax revenues, in addition to their share of county

tax revenues and their state Basic Education Program (BEP) funds. Municipal districts are

also, on average, smaller than county districts, meaning that funding for education is divided

by fewer students, which tends to result in a higher per-pupil expenditure gure.

Type of

school district

Average total per-

pupil expenditures

Average number

of schools

Average

enrollment

County $9,467 16 8,963

Municipal $10,085 5 3,187

Special $9,618 4 1,586

8

Context is key when analyzing Tennessee’s

school-level per-pupil expenditure data, and data

limitations should be considered

As states begin publishing expenditures at the school level, one major challenge exists in presenting such

information: schools that appear similar in some respects – grade levels, number of students, for example – may

dier in the amount of spending per student, and it will be important to consider possible explanations for

such dierences. Because districts must account for a variety of factors when allocating funds to schools, it is

not advisable to isolate a single factor as the reason certain schools in a district spent more per pupil than others.

is section discusses several elements that should be considered when reviewing school per-pupil expenditures.

Data considerations

ESSA requires only the reporting of the total per-pupil expenditure at the district and school levels. e

reporting requirement was not designed to provide an in-depth view of how each school spends money.

28

e method TDOE used to collect school per-pupil expenditure data from districts in this rst year (2018-

19) limits data analysis. TDOE asked each district to provide information in the form of an Excel spreadsheet

with totals of specic expenditures (i.e., salaries and benets, instructional supplies and materials, utilities, and

school nutrition) that could be attributed to each school, and to provide a breakdown between federal and

state/local expenditures.

29

(Tennessee’s formula combines state and local funds into one expenditure category

because, when districts prepare their budgets, BEP funding from the state and local matching dollars are

commingled and the dollars “lose their identity” in terms of revenue source. District budgets do not identify

what portion of expenditures are paid for with state funds versus local funds.

30

)

e spreadsheets that districts provided contain totals for the expenditures in each category by school but

do not contain all the data – i.e., individual expenditures and accounts – that districts used to aggregate

the expenditure totals. As expenditure reporting requirements do not include a provision for districts to

distinguish between state and local sources, the per-pupil expenditure formula cannot capture this split.

TDOE ocials indicated a high level of condence in the data that districts provided, but OREA did not

verify districts’ data.

31

e department provided OREA with some select districts’ spreadsheets for review. Salaries and benets made

up the bulk of school expenditures across the board, but data for these was not collected in a way that would

allow an analysis, for example, of whether the school employs a larger proportion of newer teachers with lower

salaries or more experienced teachers with higher salaries.

G

Private donations that schools receive are not included in the data. For some schools, private funds are a

signicant source of funding that may be used to fund items such as building renovations, teacher supplies,

and technology needs.

32

e inclusion of these funds into the per-pupil spending data could help identify

dierences among schools that are unrelated to the funds derived from federal, state, and local sources of

funds. Few states have elected to include private funds in their reporting of per-pupil school spending,

however – OREA identied only one: Massachusetts. In the federal regulations concerning the reporting of

per-pupil school-level expenditures that were ultimately revoked, private funds specically were not to be

included in state and local expenditures used for reporting.

33

G

Tennessee educator information, such as salary and licensure data, is available through TN Compass. Aggregated data must be requested from TDOE and is not

readily available for public download.

9

Interpreting per-pupil expenditure data

As of the 2018-19 school year, only the two largest districts in the state, Metro Nashville and Shelby County,

are using school-based budgeting. Almost all of Tennessee’s school districts budget at the district level and,

after expenditures are made, then report per-pupil expenditure gures. (See “A short explanation of how K-12

public schools in Tennessee are funded” starting on page 5 for more information on how districts budget and

distribute funds for education.)

It is important to keep in mind that this data is best used to compare schools within one district, not to

compare schools from dierent districts to one another. Tennessee’s school districts are quite varied in terms

of size and student demographics. Seven of the state’s 141 districts have only one school while Shelby County

served over 100,000 students in 202 schools in 2018-19. e ve largest urban districts in the state are dierent

from most of the other districts not only in the number of students enrolled but in the student populations

they serve and the resources they have available. e revenue sources available to school districts and the way

they distribute funds to schools can also vary – urban school districts can raise more local revenue for education

than smaller rural districts. e total amount of funds spent at an urban school with a large population of poor

students is not an even comparison to a small rural school with a less diverse student population.

Additionally, it is not advisable to isolate a single factor – such as the grade level, or the percent of

economically disadvantaged students or English learners at a school – as the reason a school spent more per

pupil compared to other schools. Further statistical analyses may reveal the inuence that these variables have

on spending, but one director of schools told OREA that no single factor would ever be the driving force for

his district’s decisions to allocate more or less funding to a particular school. Allocating funds to schools, this

director explained, is not a matter of simply ranking schools by certain student demographic characteristics

and using that to determine how to distribute funding.

34

See “School districts use dierent methods to allocate

education funds to each individual school” on page 6.

OREA analyzed total school-level expenditures per pupil in several districts to illustrate dierent factors that

could inuence school-level per-pupil gures. Some examples are described below.

Special population schools

Some districts have schools that specialize in serving certain populations, such as students with disabilities.

ese schools often have low enrollments but the highest per-pupil expenditures in their districts.

For example, in Metro Nashville, the six schools with the highest school-level per-pupil expenditures all serve

special populations of students. ese schools spend fewer total dollars than the district average, but, due to

the small number of students they serve, the total per-pupil expenditures range from over $34,000 to almost

$70,000 per pupil compared to the district average of $12,757. In addition to high per-pupil expenditures of

state and local funds, the district’s three special education schools – Murrell at Glenn School, Harris Hillman

Special Education School, and Cora Howe School – spend the most federal dollars out of all the schools in

MNPS, likely due to higher federal IDEA funding.

H

Another example of low enrollment schools that serve special populations is the New Directions Academy in

Dickson County, which serves as the district’s alternative program for students in grades K-12. In 2018-19,

the school reported school-level expenditures of about $38,000 per student, compared to a district average

of about $9,250. e school’s total expenditures – about $1.3 million – were the lowest of all the district’s

schools, but its low enrollment (33 students) means that the total expenditures are divided by far fewer

students than other schools, where enrollments range from about 200 to 1,500 students.

H

IDEA funding is allocated by the state to districts, not to individual schools. Districts determine how IDEA funding will be allocated based in part on an

assessment of student needs.

10

Enrollment and grade span

In addition to a school’s enrollment, the grade levels served may inuence spending. Elementary schools often

enroll fewer students than high schools, but state law requires elementary schools to have smaller class sizes

than high schools which may result in more teachers – thus, potentially higher expenditures – per grade.

I

For the 2018-19 school year, on average, elementary schools had the highest school-level per-pupil

expenditures, about $760 higher than high schools and over $1,200 more than middle schools, as shown in

Exhibit 3.

Exhibit 3: Average school-level per-pupil expenditures by grade span, statewide

Source: Tennessee Department of Education.

Demographics

e demographic makeup of Tennessee’s public schools varies signicantly and may play a greater or lesser role

in a district’s decisions about allocating funds to schools.

J

A school with higher numbers of certain student

demographics (e.g., students with disabilities, or students classied as economically disadvantaged or English

learners) may have higher – or lower – per-pupil expenditures than another school with a similar number of

students enrolled and a similar grade span. Although the BEP generates funding based on numbers of at-risk

students, because the BEP is a funding formula and not a spending plan, there is no requirement that these

funds be used for or reported as expenditures for at-risk or economically disadvantaged students. is is also

the case for other student demographics, such as English learners and special education students.

Student demographics are often categorized into three subgroups: economically disadvantaged (ED), English

learners (EL), and students with disabilities, which were discussed above. Statewide, approximately 35 percent

of Tennessee’s K-12 students are classied as ED, but the number of ED students in each district ranges from

about 3 percent in Williamson County to 64 percent in Lake County.

K

About 45,000 students statewide

(5 percent) are classied as English learners (EL). During the 2018-19 school year, Metro Nashville served

almost 14,000 EL students while 12 districts did not have any students classied as EL. Students in both these

categories are more likely to need services to support them academically, which may mean higher expenditures

for some schools.

Although federal money is a signicant source of funding for schools with certain types of students, such as

low-income students and students with disabilities, overall federal funds account for a much smaller percent of

districts’ budgets. Only 11 percent of Tennessee school districts’ revenues came from federal funding in 2018-

19.

35,L

In an analysis of the per-pupil expenditure data, OREA found that federal funds are linked with student

demographics to a greater degree than are state and local funds. (See box on page 11).

All Tennessee school districts receive federal education funds.

36

Districts with high numbers of students who

are economically disadvantaged, have disabilities, or are English learners receive (and thus, spend) more in

federal funds than districts with lower numbers of those subgroups of students.

I

Tennessee Code Annotated 49-1-104(a). State law sets the average class size at 20 students for grades K-3, 25 students for grades 4-6, and 30 students for grades 7-12.

J

Almost all of Tennessee’s school districts budget at the district level and then report per-pupil expenditure gures after expenditures are made.

K

Approximately 74 percent of the Achievement School District’s student population is classied as economically disadvantaged.

L

is gure includes federal funding from all sources, including school nutrition.

Grade span School level per-pupil expenditures Average enrollment

Elementary

$7,886 465

Middle

$6,669 596

High

$7,122 859

11

e federal laws that require the distribution of these funds to states are Title I, Title III, and the Individuals

with Disabilities Education Act (IDEA). (See “Federal funds received by Tennessee school districts.”)

States distribute the funds to districts, which then allocate the funds to schools. e funds can be used to

supplement state and local funds for districts but cannot be used to supplant them.

M

English learners

During the 2018-19 school year, six school districts

accounted for about 69 percent of all students classied

as English learners.

N

Two of these districts (Davidson

and Shelby) served almost half (or 48 percent) of

all EL students in Tennessee.

O

For example, within

Metro Nashville, which serves the largest number

(13,701) of EL students in the state, EL students are

not evenly distributed among the schools. In 2018-

19, one elementary school, Tusculum Elementary,

served more EL students (451 students) than 47 other

schools combined, which served a collective total of 417

students. Five schools reported serving no EL students.

Shelby County served approximately 8,000 EL

students, the second highest total number in the state

after Metro Nashville. During the 2018-19 school year,

29 schools in Shelby County reported no EL students

while six schools served almost 20 percent (1,560) of

the district’s 7,950 EL students. Of the 10 schools with the highest percentage of EL students, the per-pupil

amounts range from $10,925 to $14,100.

Economically disadvantaged students

e BEP’s at-risk component provides a specied amount of state funding for each student identied as “at

risk.”

P

e term is also synonymous with another descriptor for students: “economically disadvantaged or ED.”

Q

As explained previously, it is important not to use one single variable to explain why a school spends more or

less than similar schools in the same district. In larger districts with a diverse student population, however,

students’ economic status is an important consideration that may factor into school decisions about spending.

Schools with large populations of poor students may not have access to private sources of fundraising through

M

In general, schools and districts can use Title I funds in ways they deem best to achieve the goals of Title I: to supplement instructional support for students at risk

of educational failure, within certain scal parameters. Districts must be able to verify that each Title I school receives the same amount of state and local funds it

would have received if it did not participate in the Title I program – in other words, districts can supplement but cannot supplant state and local education funds

with federal Title I funds. 20 U.S. Code 6321 (a); 20 U.S. Code 7901.

N

According to federal law, an English Learner student is one “whose diculties in speaking, reading, writing, or understanding the English language may be

sucient to deny the individual the ability to meet the challenging state academic standards, the ability to successfully achieve in classrooms where the language of

instruction is English, or the opportunity to participate fully in society.”

O

Davidson, Shelby, Knox, Hamilton, Rutherford, and Hamblen had 31,174 of the state’s 45,250 EL students in 2018-19 or about 69 percent. Davidson and Shelby

alone had 21,624 EL students (most in Davidson) or about 48 percent of all EL students in the state.

P

At-risk students meet direct certication eligibility guidelines, i.e., a process that allows states and school districts to certify children who are eligible for free meals.

e term “at risk” also refers to students who are homeless, migrant, foster, and runaway students – i.e., students who experience circumstances that make them more

likely to be at risk academically. e amount of funding generated for the at-risk component includes state funds with a required local match. e amount depends

on the scal capacity of the school district.

Q

Tennessee Department of Education, Every Student Succeeds Act: Building on Success in Tennessee, ESSA State Plan, Updated Aug. 13, 2018, p. 68: “e

‘economically disadvantaged students’ subgroup includes all students who are directly certied to receive free lunch without the need to complete the household

application. Homeless, runaway, and migrant children and children from households that receive benets under the Supplemental Nutrition Assistance Program

(SNAP), Temporary Assistance for Needy Families (TANF), or the Food Distribution Program on Indian Reservations (FDPIR) are deemed “categorically eligible”

for free school meals and are directly certied.” See https://www.tn.gov/content/dam/tn/education/documents/TN_ESSA_State_Plan_Approved.pdf.

Federal funds received by Tennessee school districts

All Tennessee school districts receive federal Title I, Part

A funds. In scal year 2019, Tennessee’s grant for Title

I, Part A totaled $302,108,622. Shelby County received

the largest Title I, Part A subgrant at $61,147,324,

and Richard City received the smallest at $86,246. All

Tennessee school districts receive Title I funds.

In 2018-19, 66 districts received Title III funding to

support English learners academically.

In 2018-19, all school districts received funds under

the Individuals with Disabilities Education Act (IDEA)

to support students with disabilities academically.

Tennessee’s IDEA grant totaled $239,217,149 that

year. Shelby County had the largest subgrant at

$26,488,747, and State Board of Education had the

smallest at $53,954.

Source: Tennessee Department of Education, Annual Statistical

Report, 2018-19, Table 14.

12

groups such as booster clubs or parent-teacher organizations, for example. Conversely, larger urban districts

have more resources for local funding for education which may inuence total funds for education.

Like the EL student population, the distribution of ED students is not always evenly spread among schools

within the same district. For example, in Clarksville-Montgomery County Schools, the percent of ED students

in the district’s 39 schools ranges from 8 percent to 65 percent. In small rural districts, the opposite can be

true. For example, approximately 46 percent of the 1,515 students in Decatur County Schools were classied

as economically disadvantaged in 2018-19, ranging from 40 to 61 percent. For more detailed information on

district- and school-level nancial and demographic information, see OREA’s interactive dashboard.

Exhibit 4: Decatur County Schools per-pupil expenditures by school, 2018-19

School-level programming

Schools with special programs may warrant additional funding for specialized sta and supplies. Examples of

such programs include:

• language immersion courses for one or more grade levels;

• special skills classes for students with behavioral issues;

• STEM (science, technology, engineering, and math) focused courses or after school programs;

• magnet schools; and

• gifted education programs.

Building costs and utilities

Tennessee’s school-level per-pupil expenditure gure includes the cost of each individual school’s utilities –

electricity, fuel/oil, natural gas, and water and sewer. e costs of heating and cooling a building constructed

in 1950 will typically be higher than those for a more energy ecient building constructed in the past two

decades. For example, in Robertson County Schools, the cost of utilities ($154,316 for the 2018-19 school

year) at one elementary school built in 1952 is about double the cost of utilities ($76,469 for the 2018-19

school year) at a high school constructed in 2010.

13

Endnotes

1

20 USC 6311 (h)(1)(C )(x), https://www.law.

cornell.edu/uscode/text/20/6311.

2

Edunomics Lab, Interstate Financial Reporting:

Making the most of school-level per-student spending

data, 2018, p. 1, https://edunomicslab.org/wp-

content/uploads/2018/03/Interstate-Financial-

Reporting_FINAL.pdf (accessed Oct. 27, 2020).

3

Jason Botel, Acting Assistant Secretary, United

States Department of Education, Dear Colleague

Letter, June 28, 2017, https://oese.ed.gov/

les/2020/07/perpupilreqltr.pdf (accessed Dec. 1,

2020).

4

Edunomics Lab, Interstate Financial Reporting:

Making the most of school-level per-student spending

data, 2018, p. 1, https://edunomicslab.org/wp-

content/uploads/2018/03/Interstate-Financial-

Reporting_FINAL.pdf (accessed Oct. 27, 2020).

5

Ibid.

6

Lucy Hadley, Elizabeth Ross, and Marguerite Roza,

A Moment of (Early) Truth: Taking Stock of School-by-

School Spending Data, Edunomics Lab, 2020, https://

edunomicslab.org/wp-content/uploads/2020/07/

School-Level-Data-Brief_R5.pdf (accessed Oct. 15,

2020).

7

Tennessee Department of Education, Local Finance

Update, 2018 Spring Fiscal Workshop, p. 92, https://

eplan.tn.gov/documentlibrary/ViewDocument.

aspx?DocumentKey=1363194&inline=true (accessed

Oct. 9, 2020).

8

Ibid.

9

Tennessee Department of Education, Executive

Director, Oce of Local Finance, interview, Aug. 12,

2020.

10

Ibid.

11

Tennessee Department of Education, Oce of

Local Finance, Standardized System of Accounting

and Reporting, Issued July 1, 2001, https://

eplan.tn.gov/documentlibrary/ViewDocument.

aspx?DocumentKey=415987&inline=true (accessed

Sept. 15, 2020).

12

Tennessee Department of Education, 2019 Annual

Statistical Report, Table 19, p. 96.

13

See a complete explanation of the BEP at https://

comptroller.tn.gov/oce-functions/research-and-

education-accountability/interactive-tools/bep.html.

14

Tennessee Department of Education, 2019 Annual

Statistical Report, Table 14, p. 96.

15

See OREA Education Glossary, “Revenue Sources,”

https://comptroller.tn.gov/oce-functions/research-

and-education-accountability/collections/glossary.

html.

16

See OREA BEP Portal, https://comptroller.

tn.gov/oce-functions/research-and-education-

accountability/interactive-tools/bep.html.

17

Tennessee Code Annotated 49-3-314(c)(1-3).

18

Tennessee Department of Education, 2019 Annual

Statistical Report, Table 19, p. 96.

19

See OREA Education Glossary, “Title I,” https://

comptroller.tn.gov/oce-functions/research-and-

education-accountability/collections/glossary.html.

20

Director of Schools, Dickson County Schools,

interview, Sept. 18, 2020.

21

Ibid.

22

Rebecca R. Skinner, Congressional Research

Service, State and Local Financing of Public Schools,

Aug. 26, 2019.

23

Budgets, Metro Nashville Public Schools, https://

www.mnps.org/budgets (accessed Nov. 16, 2020).

24

Shelby County Schools, Back 2 Students,

Frequently Asked Questions, http://www.scsk12.org/

back2students/les/2018/Back2StudentsFAQs.pdf

(accessed Nov. 16, 2020).

25

Tennessee Code Annotated 49-2-203(9)(A)(i).

14

26

Tara Bergfeld and Linda Wesson, Teacher Salaries in

Tennessee, 2015-2018, Comptroller of the Treasury,

Oce of Research and Education Accountability,

April 2019, p. 7, https://comptroller.tn.gov/oce-

functions/research-and-education-accountability/

publications/k-12-education/content/teacher-salaries-

in-tennessee--2015-to-2018.html (accessed Nov. 16,

2020).

27

Ibid.

28

Lucy Hadley, Elizabeth Ross, and Marguerite Roza,

A Moment of (Early) Truth: Taking Stock of School-

by-School Spending Data, Edunomics Lab, https://

edunomicslab.org/wp-content/uploads/2020/07/

School-Level-Data-Brief_R5.pdf (accessed Oct. 27,

2020).

29

Tennessee Department of Education, Oce of

Local Finance, select LEA spreadsheets.

30

Tara Bergfeld and Linda Wesson, Teacher Salaries in

Tennessee, 2015-2018, Comptroller of the Treasury,

Oce of Research and Education Accountability,

April 2019, p. 7, https://comptroller.tn.gov/oce-

functions/research-and-education-accountability/

publications/k-12-education/content/teacher-salaries-

in-tennessee--2015-to-2018.html (accessed Nov. 16,

2020).

31

Tennessee Department of Education, Executive

Director, Oce of Local Finance, interview, Aug. 12,

2020.

32

Jason Gonzales, “How the community rallied

around one Nashville school to give its students –

and teachers – a chance to thrive,” e Tennessean,

Nov. 19, 2019, https://www.tennessean.com/

story/news/education/dismissed/2019/11/20/

how-community-rallied-around-nashville-school-

let-thrive/2562054001/ (accessed Oct. 28, 2019).

Jessica Bliss and Jason Gonzales, “Others step up

for Nashville schools in needy communities without

PTO support,” e Tennessean, Oct. 23, 2019,

https://www.tennessean.com/story/news/education/

dismissed/2019/10/24/nashville-public-schools-

pto-inequity-step-up/3943237002/ (accessed Oct.

28, 2020). Jessica Bliss and Jason Gonzales, “In a

district already facing deep divides, one Nashville

school’s PTO raised $218,000, one $150,” e

Tennessean, Oct. 23, 2019, https://www.tennessean.

com/story/news/education/dismissed/2019/10/24/

nashville-schools-pto-fundraising-parent-teacher-

support/2157624001/ (accessed Oct. 28, 2020).

33

34 CFR 200.35, 7-1-17 Edition, https://www.

govinfo.gov/content/pkg/CFR-2017-title34-vol1/

pdf/CFR-2017-title34-vol1-sec200-35.pdf (accessed

Nov. 16, 2020).

34

Director of Schools, Dickson County Schools,

interview, Sept. 18, 2020.

35

Tennessee Department of Education, 2019 Annual

Statistical Report, p. 96.

36

Tennessee Department of Education, 2019 Annual

Statistical Report, Table 14, pp. 79-81.

Oce of Research and Education Accountability

Russell Moore | Director

425 Rep. John Lewis Way N.

Nashville, Tennessee 37243

615.401.7866

www.comptroller.tn.gov/OREA/